UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22005

Allspring Global Dividend Opportunity Fund

(Exact name of registrant as specified in charter)

1415 Vantage

Park Drive, 3rd Floor, Charlotte, NC 28203

(Address of principal executive offices) (Zip code)

Matthew Prasse

Allspring Funds Management, LLC

1415 Vantage Park Drive, 3rd Floor, Charlotte, NC 28203

(Name and address of agent for service)

Registrant’s telephone number, including area

code: 800-222-8222

Date of fiscal year end:

October 31

Date of reporting period: October 31, 2023

ITEM 1. REPORT TO STOCKHOLDERS

Allspring Global Dividend Opportunity Fund (EOD)

Annual Report

October 31, 2023

The views expressed and any forward-looking statements are as of October 31, 2023, unless otherwise noted, and are those of the Fund’s portfolio

managers and/or Allspring Global Investments. Discussions of individual securities or the markets generally are not intended as individual recommendations.

Future events or results may vary significantly from those expressed in any forward-looking statements. The views expressed are subject to change at any time

in response to changing circumstances in the market. Allspring Global Investments disclaims any obligation to publicly update or revise any views expressed

or forward-looking statements.

Allspring Global Dividend Opportunity Fund | 1

Letter to shareholders (unaudited)

Andrew Owen

President

Allspring

Funds

Dear Shareholder:

We are pleased to offer you this annual report for the Allspring Global Dividend Opportunity Fund for the

12-month period that ended October 31, 2023. Globally, stocks and bonds experienced high levels of volatility through the period. The market was focused on persistently high inflation and the impact of ongoing aggressive central bank rate hikes. Compounding these concerns were the

global reverberations of the Russia-Ukraine war. Riskier assets rallied in 2023, as investors anticipated an end to the tight monetary policy despite concerns of a possible impending recession. After suffering deep and broad losses through 2022, bonds now benefit from

a base of higher yields that can help generate higher income. However, ongoing rate hikes continued to be a headwind during recent months.

For the 12-month period, stocks generally outperformed bonds—both domestic

U.S. and global. For the period, U.S. stocks, based on the S&P 500

Index,1 gained 10.14%. International stocks, as measured by the MSCI ACWI ex USA Index (Net),2 returned 12.07%, while the MSCI EM Index (Net) (USD)3 had more modest performance, with a gain of 10.80%. Among bond indexes, the Bloomberg U.S. Aggregate Bond Index4 returned 0.36%, the Bloomberg Global Aggregate ex-USD Index (unhedged)5 gained 2.59%, the Bloomberg

Municipal Bond Index6 gained 2.64%, and the ICE BofA U.S. High Yield Index7 returned 5.90%.

Despite

high inflation and central bank rate hikes, markets rallied.

As the

12-month period began, stocks and bonds rallied in November. Economic news was encouraging, driven by U.S. labor market strength. Although central banks kept increasing rates, hopes rose for an easing in the pace of rate hikes and a possible end to central bank monetary tightening in 2023.

While inflation remained at record highs in the eurozone, we began to see signs of a possible decline in inflationary pressures as U.S. inflation moderated. China’s economic data remained weak, reflecting its zero-COVID-19 policy.

Financial markets cooled in December, with U.S. equities declining overall in response to a weakening U.S.

dollar. Fixed income securities ended one of their worst years ever, with generally flat monthly returns as markets weighed the hopes for an end to the monetary tightening cycle with the reality that central banks had not completed their jobs yet. U.S. Consumer Price Index (CPI)8 data showed a strong consistent trend downward, which brought down the 12-month CPI to 6.5% in December from 9.1% in June. Other countries and regions reported still-high but

declining inflation rates as the year wound down.

1

The S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value-weighted index with each stock’s weight in the index

proportionate to its market value. You cannot invest directly in an index.

2

The Morgan Stanley Capital International (MSCI) All Country World Index (ACWI) ex USA

Index (Net) is a free-float-adjusted market-capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets,

excluding the U.S. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. You cannot invest directly in an index.

3

The MSCI Emerging Markets (EM) Index (Net) (USD) is a free-float-adjusted market-capitalization-weighted index that is designed to measure the equity market performance of emerging markets. You cannot invest directly in an index.

4

The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the

investment-grade, U.S.-dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities

(agency fixed-rate and hybrid adjustable-rate mortgage pass-throughs), asset-backed securities, and commercial mortgage-backed securities. You cannot invest directly in an

index.

5

The Bloomberg Global Aggregate ex-USD Index (unhedged) is an unmanaged index that provides a broad-based measure of the global investment-grade fixed income markets excluding the U.S.-dollar-denominated debt market. You cannot invest directly in an index.

6

The Bloomberg Municipal Bond Index is an unmanaged index composed of long-term

tax-exempt bonds with a minimum credit rating of Baa. You cannot invest directly in an index.

7

The ICE BofA U.S. High Yield Index is a market-capitalization-weighted index of

domestic and Yankee high yield bonds. The index tracks the performance of high yield securities traded in the U.S. bond market. You cannot invest directly in an index.

Copyright 2023. ICE Data Indices, LLC. All rights reserved.

8

The U.S. Consumer Price Index (CPI) is a measure of the average change over time in

the prices paid by urban consumers for a market basket of consumer goods and services. You cannot invest directly in an index.

2 | Allspring Global Dividend Opportunity Fund

Letter to shareholders (unaudited)

The year 2023 began with a

rally across global equities and fixed income securities. Investor optimism rose in response to data indicating declining inflation rates and the reopening of China’s economy with the abrupt end to its zero-COVID-19 policy. The U.S. reported strong job gains and

unemployment fell to 3.4%—the lowest level since 1969. Meanwhile, wage growth, seen as a potential contributor to ongoing high inflation, continued to moderate. All eyes remained on the Federal Reserve (Fed) and on how many more rate hikes remain in

this tightening cycle. The 0.25% federal funds rate hike announced in January was the Fed’s smallest rate increase since March 2022.

Markets declined in February as investors responded unfavorably to resilient economic data. The takeaway: Central banks

would likely continue their monetary tightening cycle for longer than markets had priced in. In this environment—where strong economic data is seen as bad news—the resilient U.S. labor market was taken as a negative, with inflation not falling

quickly enough for the Fed, which raised interest rates by 0.25% in February. Meanwhile, the Bank of England (BoE) and the European Central Bank (ECB) both raised rates by 0.50%.

The collapse of Silicon Valley Bank in March—the second-largest banking failure in U.S. history—led

to a bank run that spread to Europe, where Switzerland’s Credit Suisse was taken over by its rival, UBS. The banking industry turmoil created an additional challenge for central banks in balancing inflationary concerns against potential economic weakening. Meanwhile, other data in

March pointed to economic strength in the U.S., Europe, and China. China’s economy continued to rebound after the removal of its COVID-19 lockdown. Inflation rates in the U.S., the U.K., and the eurozone all remained higher than central bank

targets, leading to additional rate hikes in March.

Economic data released in April pointed

to global resilience, as Purchasing Managers Indexes1 in the U.S., U.K., and eurozone beat expectations and China reported first quarter annualized economic growth of 4.5%.

Despite banking industry stress, developed market stocks had monthly gains. The U.S. labor market remained strong,

with a 3.5% jobless rate and monthly payroll gains above 200,000. However, uncertainty and inflationary concerns

weighed on investors in the U.S. and abroad.

May was marked by a divergence between

expanding activity in services and an overall contraction in manufacturing activity in the U.S., U.K., and eurozone. Core inflation remained elevated in the U.S. and Europe, despite the ongoing efforts of the Fed and the ECB, which included rate

hikes of 0.25% by both in May. Stubborn inflation and the resilient U.S. labor market led to expectations of further interest rate hikes, overall monthly declines across bond indexes, and mixed results for stocks in May. Investor worries over a U.S. debt ceiling

impasse were modest, and market confidence was buoyed by a deal in late May to avert a potential U.S. debt default.

June featured the Fed’s first pause on interest rate hikes since March 2022, when it began its aggressive campaign to rein in inflation. However, Core CPI2, while continuing to decline, remained stubbornly high in June at 4.8%, well above the Fed’s 2.0% target rate. With the U.S. unemployment rate still at 3.6%, near a historical low, and U.S. payrolls growing in June for

the 30th consecutive month, expectations of more Fed rate hikes were reinforced. However, U.S. and global stocks had strong returns in June.

“ The collapse of Silicon

Valley Bank in March—the second-largest banking failure in U.S. history—led to a

bank run that spread to Europe, where

Switzerland’s Credit Suisse was taken over by its rival, UBS. ”

1

The Purchasing Managers Index (PMI) is an index of the prevailing direction of economic trends in the manufacturing and service sectors. You cannot invest directly in an index.

2

The Core CPI is a measure of the average change over time in the prices paid by urban

consumers for a market basket of consumer goods and services excluding energy and food prices. You cannot invest directly in an index.

Allspring Global Dividend Opportunity Fund | 3

Letter to shareholders (unaudited)

“ With strong

second-quarter gross

domestic

product (GDP)

growth—initially

estimated at 2.4%—and

U.S. annual inflation

easing steadily to 3.2%

in July, hopes for a soft

economic landing

grew. ”

July was a good month for stocks. However, bonds had more muted but positive monthly returns overall. Riskier sectors and regions tended to do well, as investors grew more optimistic regarding economic

prospects. With strong second-quarter gross domestic product (GDP) growth––initially estimated at 2.4%––and U.S. annual inflation easing steadily to 3.2% in July, hopes for a soft economic landing grew. The Fed, the ECB, and the BoE all raised their respective key

interest rates by 0.25% in July. In the Fed’s case, speculation grew that it could be very close to the end of its tightening cycle. Meanwhile, China’s economy showed signs of stagnation, renewing concerns of global fallout.

Stocks retreated in August while monthly bond returns were flat overall. Increased global market volatility

reflected unease over the Chinese property market being stressed along with weak Chinese economic data. On a more positive note, speculation grew over a possible end to the Fed’s campaign of interest rate increases or at least a pause in September. U.S. economic data

generally remained solid, with resilient job market data and inflation ticking up slightly in August, as the annual CPI rose 3.7%. However, the three-month trend for core CPI stood at a more encouraging annualized 2.4%.

Stocks and bonds both had negative overall returns in September as investors reluctantly recited the new

chorus of “higher for longer,” led by the Fed’s determination not to lower interest rates until it knows it has vanquished its pesky

opponent—higher-than-targeted inflation. As of September, the two primary gauges of U.S. inflation—the annual Core Personal Consumption Expenditures Price Index1 and the CPI—both stood at roughly 4%, twice as high as the Fed’s oft-stated 2% target. The month ended with the

prospect of yet another U.S. government shutdown, averted at least temporarily but looming later this fall.

October was a tough month for stocks and bonds. Key global and domestic indexes all

were pushed down by rising geopolitical tensions—particularly the Israel-Hamas conflict—and concerns

over the Fed’s “higher for longer” monetary policy. The U.S. 10-year Treasury yield rose above 5% for the first time since 2007. Commodity prices did well as oil

prices rallied in response to the prospect of oil supply disruptions from the Middle East. U.S. annualized third

quarter GDP was estimated at a healthier-than-anticipated 4.9%. China’s GDP indicated surprisingly strong

industrial production and retail sales, offset by ongoing weakness in its real estate sector.

Don’t let short-term uncertainty derail long-term investment goals.

Periods of investment uncertainty can present challenges, but experience has

taught us that maintaining long-term investment goals can be an effective way to plan for the future. Although

diversification cannot guarantee an investment profit or prevent losses, we believe it can be an effective way to manage investment risk and potentially smooth out overall portfolio performance. We encourage investors to know their investments and to understand that appropriate levels of

risk-taking may unlock opportunities.

Thank you for choosing to invest

with Allspring Funds. We appreciate your confidence in us and remain committed to helping you meet your financial needs.

Sincerely,

Andrew Owen

President

Allspring Funds

For further information about your fund, contact

your investment professional, visit our website at allspringglobal.com, or call us directly at 1-800-222-8222.

1

The Core Personal Consumption Expenditures Price Index (PCE) is a measure of prices

that people living in the United States, or those buying on their behalf, pay for goods and services. It is sometimes called the core PCE price index, because two categories

that can have price swings – food and energy – are left out to make underlying inflation easier to see. You cannot invest directly in an index.

4 | Allspring Global Dividend Opportunity Fund

Letter to shareholders (unaudited)

| |

• On November 15, 2023, the Fund announced a renewal of its open-market share repurchase program (the “Buyback

Program”). Under the renewed Buyback Program, the Fund may repurchase up to 5%

of its outstanding shares in open market transactions during the period

beginning on January 1, 2024 and ending on December 31, 2024. The Fund’s Board of Trustees has delegated to Allspring Funds Management, LLC, the Fund’s adviser, discretion to administer the Buyback

Program, including the determination of the amount and timing of repurchases in

accordance with the best interests of the Fund and subject to applicable

legal limitations. |

• The Fund’s managed distribution plan provides for the declaration of quarterly distributions to common shareholders of

the Fund at an annual minimum fixed rate of 9% based on the Fund’s average

monthly net asset value per share over the prior 12 months. Under the

managed distribution plan, quarterly distributions may be sourced from income, paid-in capital, and/or capital gains, if any. To the extent that sufficient investment income is not available on a quarterly basis, the

Fund may distribute long-term capital gains and/or return of capital to its

shareholders in order to maintain its managed distribution level. You

should not draw any conclusions about the Fund’s investment performance from the amount of the Fund’s distributions or from the terms of the managed distribution plan. Shareholders may elect to reinvest distributions

received pursuant to the managed distribution plan in the Fund under the existing

dividend reinvestment plan, which is described later in this

report. |

Allspring Global Dividend Opportunity Fund | 5

Performance highlights (unaudited)

Performance highlights

| |

The Fund’s primary investment objective is to seek a high level of current income. The Fund’s secondary

objective is long-term growth of capital. |

| |

The Fund allocates its assets between two separate investment strategies, or sleeves. Under normal market

conditions, the Fund allocates approximately 80% of its total assets to an equity sleeve comprised

primarily of common stocks and other equity securities that offer above-average

potential for current and/or future dividends. This sleeve invests normally in

approximately 60 to 80 securities, broadly diversified among major sectors and

regions. The sector and region weights are typically

within+/- 5 percent of weights in

the MSCI ACWI (Net)†. The remaining approximately 20%

of the Fund’s total assets is allocated to a sleeve

consisting of below investment grade (high yield) debt, loans, and preferred stocks.

The Fund also employs an option strategy in an attempt to generate gains on call

options written by the Fund. |

| |

Allspring Funds Management, LLC |

| |

Allspring Global Investments, LLC |

| |

Justin P. Carr, CFA, Harindra de Silva, Ph.D, CFA, Vince Fioramonti, CFA,

Chris Lee, CFA, Megan Miller, CFA, Michael J. Schueller, CFA

|

Average annual total returns (%) as of October 31, 20231 |

| |

|

|

|

| |

|

|

|

| |

|

|

|

Based on net asset value (NAV) |

|

|

|

Global Dividend Opportunity Blended Index2

|

|

|

|

ICE BofA U.S. High Yield Constrained Index3

|

|

|

|

| |

|

|

|

Figures quoted represent past performance, which is no

guarantee of future results, and do not reflect taxes that a shareholder may pay on an investment in a fund. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold, may be worth more or less than their original cost. Current performance

may be lower or higher than the performance data quoted, which assumes the reinvestment of dividends and capital gains. Performance figures of the Fund do

not reflect brokerage commissions that a shareholder would pay on the purchase and sale of shares. If taxes and such brokerage commissions had been

reflected, performance would have been lower. To obtain performance information current to the most recent month-end, please call

1-800-222-8222.

The Fund’s expense ratio for the year ended October 31, 2023, was 2.98% which

includes 1.65% of interest expense.

| |

| |

Total returns based on market value are calculated assuming a purchase of common stock on the first day and a sale on the last day of the period reported. Total returns

based on NAV are calculated based on the NAV at the beginning of the

period and at the end of the period. Dividends and distributions, if any, are assumed for the purposes of these calculations to be reinvested at prices obtained under the Fund’s Automatic Dividend Reinvestment Plan. |

| |

Source: Allspring Funds Management, LLC. The Global Dividend Opportunity Blended Index is composed of 80% Morgan Stanley Capital International (MSCI) All Country

World Index (ACWI) (Net) and 20% ICE BofA U.S. High Yield Constrained Index. Prior to

October 15, 2019, the Global Dividend Opportunity Blended Index was composed

65% of the MSCI ACWI (Net), 20% of the ICE BofA U.S. High Yield Constrained Index, and

15% of the ICE BofA Core Fixed Rate Preferred Securities Index. Prior to May 1, 2017, the Global Dividend Opportunity Blended Index was composed 65% of the MSCI ACWI (Net) and 35% of the ICE BofA Core Fixed Rate Preferred Securities Index. You

cannot invest directly in an index. |

| |

The ICE BofA U.S. High Yield Constrained Index is a market-value-weighted index of all domestic and Yankee high-yield bonds, including deferred interest bonds and

payment-in-kind securities. Issues included in the index have maturities

of one year or more and have a credit rating lower than BBB-/Baa3 but are not in default. The ICE BofA U.S. High Yield Constrained Index limits any individual issuer to a maximum of 2% benchmark exposure. You cannot invest directly in an index. Copyright 2023. ICE

Data Indices, LLC. All rights reserved. |

| |

The MSCI ACWI (Net) is a free-float-adjusted market-capitalization-weighted index that is designed to measure the equity market performance of developed and emerging

markets. Source: MSCI. MSCI makes no express or implied warranties

or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved,

reviewed, or produced by MSCI. You cannot invest directly in an

index. |

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute. |

6 | Allspring Global Dividend Opportunity Fund

Performance highlights (unaudited)

Growth of $10,000 investment as of October 31, 20231 |

| |

The chart compares the performance of the Fund for the most recent ten years with the Global Dividend Opportunity Blended Index, ICE BofA U.S. High Yield Constrained

Index and MSCI ACWI (Net). The chart assumes a hypothetical investment of $10,000

investment and reflects all operating expenses of the Fund. |

Comparison of NAV vs. market value1 |

| |

This chart does not reflect any brokerage commissions charged on the purchase and sale of the Fund’s common stock. Dividends and distributions paid by the Fund are

included in the Fund’s average annual total returns but have the effect of

reducing the Fund’s NAV. |

Allspring Global Dividend Opportunity Fund | 7

Performance highlights (unaudited)

Risk summary

This closed-end fund is no longer available as an initial public offering and is only offered

through broker-dealers on the secondary market. A closed-end fund is not required to buy its shares back from investors upon request. Shares of the Fund may trade at either a

premium or discount relative to the Fund’s net asset value, and there can be no assurance that any discount will decrease. The values of, and/or the income generated

by, securities held by the Fund may decline due to general market conditions or other factors, including those directly involving the issuers of such securities. Equity

securities fluctuate in value in response to factors specific to the issuer of the security. Small- and mid-cap securities may be subject to special risks associated with

narrower product lines and limited financial resources compared with their large-cap counterparts and, as a result, small- and mid-cap securities may decline significantly in market downturns and may be more volatile than those of larger companies due to their higher risk of failure. Debt securities are subject to credit risk and interest rate risk, and high-yield securities and unrated securities of similar credit quality have a much greater risk of default and their values tend to be more volatile than higher-rated securities with similar maturities. Foreign investments may contain more risk due to the inherent risks associated with changing political climates, foreign market instability, and foreign currency fluctuations. Risks of foreign investing are magnified in emerging or developing markets. Derivatives involve risks, including interest rate risk, credit risk, the risk of improper valuation, and the risk of noncorrelation to the relevant instruments they are designed to hedge or closely track. There are numerous risks associated with transactions in options on securities and/or indexes. As a writer of an index call option, the Fund forgoes the opportunity to profit from increases in the values of securities held by the Fund. However, the Fund has retained the risk of loss (net of premiums received) should the price of the Fund’s portfolio securities decline. Similar risks are involved with writing call options or secured put options on individual securities and/or indexes held in the Fund’s portfolio. This combination of potentially limited appreciation and potentially unlimited depreciation over time may lead to a decline in the net asset value of the Fund. The Fund is leveraged through a revolving credit facility and also may incur leverage by issuing preferred shares in the future. The use of leverage results in certain risks, including, among others, the likelihood of greater volatility of the net asset value and the market value of common shares.

More detailed information about the Fund’s investment objective, principal investment strategies and the principal risks associated with investing in the Fund can be found on page 12.

8 | Allspring Global Dividend Opportunity Fund

Performance highlights (unaudited)

MANAGER’S DISCUSSION

Overview

The

Fund’s return based on market value was -8.16% for the 12-month period that ended October 31, 2023. During the same period, the Fund’s return based on its net

asset value (NAV) was 9.52%. Based on both its market value and its NAV return, the Fund underperformed the Global Dividend Opportunity Blended Index for the

period.

Global equities rebounded at 2022 year-end and

through the first half of 2023.

Global equities rallied through the first half of 2023, supported by disinflationary trends, a

robust labor market, resilient consumer spending, and expectations of a slowdown in rate hikes by central banks. Global equity markets overcame persistent inflation, rising interest rates, recession fears, a regional banking crisis,

a Chinese economic downturn, stretched valuations, and narrow market leadership.

However, the MSCI ACWI (Net) finished lower during the third quarter, snapping a streak of three

consecutive quarters of positive returns for the index. Beginning in August, global equity markets came under pressure from the “higher for longer” interest rate narrative from developed central banks, a spike in energy

prices, a pullback in momentum for technology-focused stocks, escalating geopolitical tensions, and growing skepticism of a soft landing for many advanced economies. Over the 12-month period, global large caps outperformed small

caps and growth outperformed value.

Ten largest holdings (%) as of October 31, 20231 |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

Oaktree Specialty Lending Corp. |

|

| |

Figures represent the percentage of the Fund’s net assets. Holdings are subject to change and may have changed since the date specified. |

High yield and leveraged loans generated single-digit market returns overall.

U.S. high yield and leveraged loans performed well over the past 12 months as a modest uptick in

yields was more than offset by strong interest income, tighter credit spreads, and limited defaults. As a result, high yield generated mid-single-digit total returns and leveraged loans generated high-single-digit returns over

the period. Robust economic

growth and a decelerating pace of inflation helped boost corporate fundamentals as companies

remained profitable and generated strong cash flow. Credit rating migration remained positive as upgrades outpaced downgrades. Conversely, tighter monetary policy and higher base rates with the federal funds rate rising 225

basis points (bps; 100 bps equal 1.00%) to 5.5% put increasing pressure on marginal credits—particularly those with variable-rate bank funding. As a result, default rates pushed higher over the year, from 1% to about

2.3% as of October 31, 2023. Commodity-based sectors, such as energy, outperformed over the course

of the year whereas higher-rated, longer-duration sectors, such as utilities, lagged. However,

idiosyncratic dispersion across most sectors increased because of tighter financial conditions.

The option overlay* is a short-call strategy written on a portion of the Fund’s global equity allocation. The combined global equity and short option portfolio create a global

covered call portfolio. Over the long run, a covered call strategy aims to add yield and lower risk compared with a passive allocation to equity. The option overlay is expected to add value in flat-to-down global equity markets

and in above-average volatility environments.

The equity sleeve adapted to persistent inflation, central bank monetary tightening, and decelerating growth.

The strategy employs a blended approach between investing in higher-dividend-paying value stocks and low- or non-dividend-paying growth stocks. We continued to achieve a dividend that is

1.5 % to 2.0% higher than the benchmark. As inflation metrics rose, we reduced the strategy’s weighting in industries that are

more economically exposed, as growth may be peaking amid central bank tightening. The strategy currently has an overweight in health care, which is typically a less economically sensitive sector. The strategy has a slight

underweight in information technology (IT), where prospects related to cloud computing continue to

grow. We continue to search for IT stocks that pay a dividend.

Health care, energy, and communication services detracted from relative performance.

Pfizer, Inc., declined 32% as the company significantly reduced sales expectations for its COVID-19 vaccine and therapeutics. Bristol-Myers Squibb** pulled back 19% from increased generic competition to its

*

The option overlay is compared with the option-only returns of the U.S.-based covered call benchmarks, the Chicago Board Options Exchange (CBOE) S&P 500 Buy Write (BXM) Index and the CBOE S&P 500 2% OTM Buy Write (BXY) Index. The BXM is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. The BXY Index is a new index that uses the same methodology as BXM, but is calculated using out-of-the-money S&P 500 Index (SPX) call options, rather than at-the-money SPX call options. The Fund’s options returns against notional exposure (50% of the equity exposure) are compared to the options-only return of these indices, calculated as the respective index return less the return of the S&P 500. The unadjusted BXM Index and BXY Index returned 7.27% and 10.06%, respectively, from October 31, 2022 to October 31, 2023. You cannot invest directly in an index.

**This security was no longer held at the end of the reporting period.

Allspring Global Dividend Opportunity Fund | 9

Performance highlights (unaudited)

immunotherapy and

blood clot prevention franchises and a slower-than-expected launch of new cardiovascular drug treatments. Devon Energy fell 37% on disappointing earnings and management’s lower production and higher capital expenditures guidance.

Meta Platforms surged 223% during the period, which detracted from relative performance as the Fund did not

hold a position in the stock.

Sector allocation as of October 31, 20231 |

| |

Figures represent the percentage of the Fund’s long-term investments. Allocations are subject to change and may have changed since the date specified. |

The high yield sleeve trailed the benchmark for the period.

The high yield portfolio underperformed the benchmark for the 12-month period. In October 2022, the portfolio was overweight electric generation, air transportation, and gas

distribution and underweight telecom-wireline, gaming, and personal and household products. By rating, the Fund was overweight BBBs and Bs and underweight BBs and CCCs. The Fund was overweight to the less-than-five-years

segment, and against the index, it was shorter duration, lower in yield, and tighter on spread.

Financials, industrials, and materials stocks contributed to relative performance.

3i Group plc, a U.K-based private equity firm, returned over 62% during the holding period. 3i

Group’s lead investment, Action, is a European discount retailer that produced solid growth amid an environment of macroeconomic headwinds. nVent Electric plc, a global provider of electrical connection and protection

solutions, rose over 33% during the

period. nVent generated strong profit margins and earnings growth as the company’s

best-in-class products and services are benefiting from long-term trends toward electrification, digitization, and sustainability. Fortescue Metals Group, a leading global miner of iron ore, surged over 63% during the period, supported by a

rebound in iron ore prices and resilient demand from China.

The high yield sleeve received contributions from leisure, property and casualty, and transportation

services.

For the 12-month period that ended October 2023, within the high yield sleeve, leisure, property

and casualty, and transportation services were the strongest contributing sectors, while electric, brokerage/asset managers, and media/entertainment were the most detrimental sectors. Royal Caribbean Cruises, Fly Leasing, and

The GEO Group were our best performers, while Enviva and Resolute Investment Managers (American

Beacon) were the worst. Not holding Lumen Technologies was positive, while not holding Carvana hurt

relative performance as it rallied in the index. By rating, our underweight to higher-quality BBs helped performance, while our overweight to BBBs and underweight to CCCs were detrimental. Our overweight to the

less-than-three-year segment was a performance driver, while our overweight to seven years and out

hurt.

At

the end of October, the high yield sleeve remains shorter than the index—overweight only the one- to three-year segment. We favor single Bs over BBs and CCCs. By sector, the Fund is overweight electric generation, gas distribution, and recreation and

travel and underweight telecom-wireline, chemicals, and software/services. Relative to the index, the Fund is short on duration, lower in yield, and tighter on spread.

Leverage had a positive impact.

The Fund’s use

of leverage through bank borrowings had a positive impact on the NAV total return performance during this reporting period. As of October 31, 2023, the Fund had approximately 19% in leverage as a percent of total assets.

The option overlay added modest return to the Fund during a period of volatile equity performance. Global equity markets performed moderately during this period, with the MSCI ACWI

(Net) returning 10.50%. The index had a strong start but declined nearly 12% from its highs in the past three months as investors remained concerned about inflation, the possible policy response, and the likelihood of a

recession in 2024. Option-implied volatility reflected the market jitters during the period, oscillating in a large range from a low of 12.82 in September 2023 to a high of 26.52 in March 2023.

Recession risks are elevated as growth decelerates and credit conditions tighten.

As we enter the final quarter of 2023, the sharp rise in short-term rates appears to be taming

inflation, but the lagged effects of central bank tightening are increasing the risk of a hard economic landing in Europe, China, and many emerging markets. Growth in the U.S. has remained

resilient, but activity is weakening.

10 | Allspring Global Dividend Opportunity Fund

Performance highlights (unaudited)

Credit quality as of October 31, 20231 |

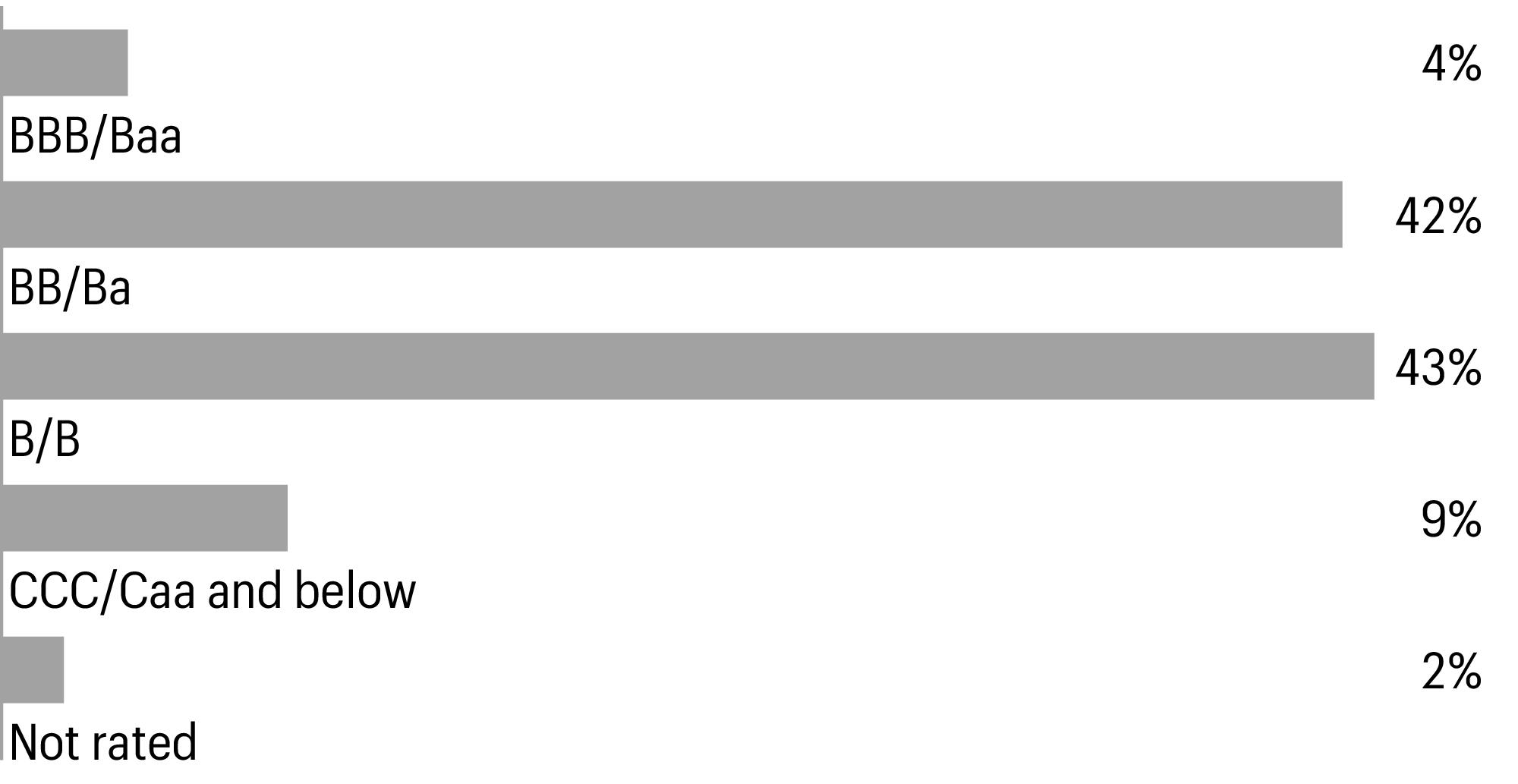

| |

The credit quality distribution of portfolio holdings reflected in the chart is based on ratings from Standard & Poor’s, Moody’s Investors Service,

and/or Fitch Ratings Ltd. Credit quality ratings apply to the underlying

holdings of the Fund and not to the Fund itself. The percentages of the

portfolio with the ratings depicted in the chart are calculated based on the

market value of fixed income securities held by the Fund. If a security

was rated by all three rating agencies, the middle rating was utilized. If

rated by two of the three rating agencies, the lower rating was utilized,

and if rated by one of the rating agencies, that rating was utilized.

Standard & Poor’s rates the creditworthiness of bonds, ranging

from AAA (highest) to D (lowest). Ratings from A to CCC may be modified by

the addition of a plus (+) or minus (-) sign to show relative standing within the rating

categories. Standard & Poor’s rates the creditworthiness of

short-term notes from SP-1 (highest) to SP-3 (lowest). Moody’s rates

the creditworthiness of bonds, ranging from Aaa (highest) to C (lowest).

Ratings Aa to B may be modified by the addition of a number 1 (highest) to

3 (lowest) to show relative standing within the ratings categories.

Moody’s rates the creditworthiness of short-term U.S. tax-exempt

municipal securities from MIG 1/VMIG 1 (highest) to SG (lowest). Fitch

rates the creditworthiness of bonds, ranging from AAA (highest) to D

(lowest). Credit quality distribution is subject to change and may have changed

since the date specified. |

Broad segments of the

global economy continue to show signs of tilting toward, or already being in, a recession. Tighter credit conditions and stubborn inflation are persistently raising the costs for businesses and prices for consumers. Consumer spending

has been resilient due to pent-up demand, but consumers are cutting back on bigger-ticket items and

trading down for discounts. Supply chains are improving, but China’s economy has faltered and international trade is in decline. Geopolitical tensions are escalating rapidly in response to Russia’s ongoing invasion of Ukraine, China’s

aggressive stance toward Taiwan, and the outbreak of war between Israel and Hamas.

For most of this rate hiking cycle, the Federal Reserve has been trying to convince the markets

that interest rates would remain “higher for longer” to ensure inflation reaches its target rate. Additionally, developed central banks are progressing with “quantitative tightening,” reversing the central bank bond purchases

undertaken to support global markets in 2020. Governments, corporations, investors, and individuals will all have to make significant adjustments in a higher interest rate environment.

While corporations in developed markets have generally been well positioned to endure higher

interest rates, their earnings have been

anemic. After three quarters in a row of falling earnings, it is likely the earnings recession

will come to an end when third quarter earnings are reported. Although earnings momentum has improved, higher real yields, a stronger U.S. dollar, and higher energy prices are headwinds to earnings growth. With valuations at

higher-than-average levels, it is difficult to expect an increase in market multiples, such as price/earnings ratios.

We currently anticipate volatile and range-bound global equity markets. While we are generally cautious, there are potential positive catalysts from decelerating inflation, a

still-tight labor market, and improving corporate earnings. As we monitor the macroeconomic environment, we will continue to diligently focus on company fundamentals and disciplined portfolio risk management.

The outlook for U.S. high yield and leveraged loans is mixed. With both segments of the market yielding close to 10%, valuations appear attractive. Current yields provide considerable

cushion for investors to weather higher price volatility and an uptick in defaults going forward. In

addition, many high yield credits have successfully transitioned to a higher inflation, higher

volatility, tighter monetary policy environment. Much success is due to well-funded balance sheets with low-cost debt. However, broad-based credit fundamentals are slowly eroding as tighter monetary

policy and higher interest costs start to bite.

Geographic allocation as of October 31, 20231 |

| |

Figures represent the percentage of the Fund’s long-term investments. Allocations are subject to change and may have changed since the date specified. |

Default rates are expected to rise toward 4% to 6% over the next 12 to 24 months as the economy

slows to below-trend growth while idiosyncratic dispersion is likely to remain high. Small to midsize borrowers heavily dependent on variable-rate bank debt are particularly vulnerable to economic shocks in this environment.

Successfully navigating the market will be heavily dependent on deft security selection and deep credit analysis.

Looking

forward, we expect investor uncertainty to continue, leading to higher implied volatility levels in the global option market. Higher levels of volatility could present a good opportunity for the option overlay strategy in the Fund.

Allspring Global Dividend Opportunity Fund | 11

Objective, strategies and risks (unaudited)

Objective, strategies and

risks

Investment objective

The Fund’s primary investment objective is to seek a high level of current income. The Fund’s secondary objective is long-term growth of capital. The Fund’s investment objectives are non-fundamental policies and may be changed by the Trustees without prior approval of the Fund’s shareholders.

Principal investment strategies

The Fund allocates its assets between two separate investment strategies, or sleeves, equity and high yield. Under normal market conditions, the Fund allocates approximately 80% of its total assets to an equity sleeve comprised primarily of a diversified portfolio of common stocks of U.S. and non-U.S. companies and other equity securities that offer above-average potential for current and/or future dividends. The remaining 20% of the Fund’s total assets is allocated to a sleeve consisting of below investment-grade (high yield) debt securities, loans, and preferred stocks. The Fund also employs an option strategy in an attempt to generate gains on call options written by the Fund.

Equity Sleeve. The Fund’s equity sleeve invests normally in approximately

60 to 80 securities, broadly diversified among major sectors and regions. The sector and region weights are typically within+/- 5 percent of weights in the MSCI ACWI Index. Region weights are managed according to

Wells Capital Management’s proprietary region classification. We target an overall portfolio dividend yield higher than that of the MSCI ACWI Index. The equity sleeve

of the Fund may hold equity securities of companies of any size, including companies with large, medium, and small market capitalizations. The equity sleeve of the Fund may hold equity securities issued by domestic or foreign issuers, including emerging market issuers. The equity sleeve of the Fund will likely include primarily common stocks, although the Fund may also invest in preferred stocks, and securities convertible into or exchangeable for common stock, such as convertible preferred stocks.

Our approach is to lever the best attributes of quantitative tools and fundamental analysis. Our quantitative model casts a wide net to identify buy and sell candidates in our investment universe. Our fundamental overlay gives us the conviction that we need to build a portfolio that both targets high levels of income while still maintaining a broad-based, well-diversified exposure.

We employ a proprietary, quantitative model to evaluate all companies in the investment universe. The model draws from a factor library containing both cross-sectional and sector-specific factors. It seeks to identify companies that provide attractive dividend yields, but also have favorable quality characteristics and growth potential. The model is comprised of three unique factor

groupings: valuation, quality and momentum. The valuation factors identify companies that are undervalued relative to their peers; the quality factors identify companies with strong management and profitability; and the momentum factors identify companies that have market support and positive investor sentiment. The factor composition of the model is reviewed and refreshed each quarter through a dynamic process called re-specification. The process enhances the predictive power of the model by considering recent changes in the underlying drives of stock price movement.

As previously mentioned, the investment approach combines the objectivity and repeatability of quantitative modeling with a qualitative review and validation of every stock that is added to the portfolio. The qualitative review helps us build conviction in the positions that we put into the portfolio by considering data that is more difficult to process and consume systematically in a timely fashion. We use additional sources of information such as news sentiment data, research reports, short interest data and a multitude of other resources to uncover nuances within companies that a traditional systematic strategy may not identify. Through this analysis we seek to verify that the financials driving the quantitative model reflect the true prospects of the business, identify non-quantifiable opportunities and the risks in companies, and avoid value traps (which are ever-present risk in dividend strategies).

Material Changes During the Fiscal Year ended October 31, 2023: There were no material changes to the equity sleeve during the fiscal year ended

October 31, 2023.

High Yield Sleeve. Under normal market conditions, the Fund allocates

approximately 20% of its total assets to an investment strategy that focuses on U.S. dollar-denominated below investment-grade bonds (including convertible bonds),

debentures, and other income obligations, including loans and preferred stocks (often called “high yield” securities or “junk bonds”). We may invest

in below investment-grade debt securities of any credit quality, however, we may not purchase securities rated CCC or below if 20% of the sleeve’s assets are already

held with such a rating. We are not required to sell securities rated CCC or below if the 20% limit is exceeded due to security downgrades.

The sleeve will not invest more than 20% of its total assets in convertible instruments

(convertible bonds and preferred stocks). The sleeve may invest up to 10% of its total assets in U.S. dollar–denominated securities of foreign issuers, excluding

emerging markets securities.

For purposes of the Fund’s credit quality

policies, if a security receives different ratings from nationally recognized securities rating organizations, the Fund will use the rating that the portfolio managers

believe is most representative of the security’s credit quality. The Fund’s high yield securities may have fixed or variable principal payments and all types of

interest rate and dividend payment and reset terms, including fixed rate, adjustable rate, contingent, deferred, payment in kind and auction rate features. The sleeve may

invest in securities with a broad range of maturities.

The Fund’s high yield

sleeve is managed following a rigorous investment process that emphasizes both quality and value. The research driven approach includes both a top-down review of

macroeconomic factors and intensive, bottom-up scrutiny of individual securities. We consider both broad economic

12 | Allspring Global Dividend Opportunity Fund

Objective, strategies and risks (unaudited)

and issuer

specific factors in selecting securities for the high yield sleeve. In assessing the appropriate maturity and duration for the Fund’s high yield sleeve and the credit

quality parameters and weighting objectives for each sector and industry in this portion of the Fund’s portfolio, we consider a variety of factors that are expected to

influence the economic environment and the dynamics of the high yield market. These factors include fundamental economic indicators, such as interest rate trends, the rates

of economic growth and inflation, the performance of equity markets, commodities prices, Federal Reserve monetary policy and the relative value of the U.S. dollar compared to

other currencies. Once we determine the preferable portfolio characteristics, we conduct further evaluation to determine capacity and inventory levels in each targeted

industry. We also identify any circumstances that may lead to improved business conditions, thus increasing the attractiveness of a particular industry. We select individual

securities based upon the terms of the securities (such as yields compared to U.S. Treasuries or comparable issues), liquidity and rating, sector and issuer diversification.

We also employ due diligence and fundamental research to assess an issuer’s credit quality, taking into account financial condition and profitability, future capital

needs, potential for change in rating, industry outlook, the competitive environment and management ability.

The analysis of issuers may include, among other things, historic and current financial

conditions, current and anticipated cash flow and borrowing requirements, value of assets in relation to historical costs, strength of management, responsiveness to business

conditions, credit standing, the company’s leverage versus industry norms and current and anticipated results of operations. While we consider as one factor in our

credit analysis the ratings assigned by the rating services, we perform our own independent credit analysis of issuers.

In making decisions for the high yield sleeve, we rely on the knowledge, experience and judgment

of our team who have access to a wide variety of research. We apply a strict sell discipline, which is as important as purchase criteria in determining the performance of

this portion of this portfolio. We routinely meet to review profitability outlooks and discuss any deteriorating business fundamentals, as well as consider changes in equity

valuations and market perceptions before selling securities.

We regularly review the investments of the portfolio and may sell a portfolio holding when it has achieved its valuation target, there is deterioration in the underlying fundamental of the business, or we have identified a more attractive investment opportunity.

Material Changes During the Fiscal Year ended October 31, 2023: There were no material changes to the high yield sleeve during the fiscal year ended

October 31, 2023.

Option Strategy. The Fund also employs an option strategy in an attempt to

generate gains from the premiums on call options written by it on selected U.S. and non-U.S.-based securities indices, on exchange-traded funds providing returns based on

certain indices, countries, or market sectors, and, to a lesser extent, on futures contracts and individual securities. The Fund may write covered call options or secured put

options on individual securities and/or indexes. The Fund may also purchase call or put options.

The Fund may write call options with an aggregate net notional amount of up to 50% of the value

of the equity sleeve’s total assets. The extent of the Fund’s use of written call options will vary over time based, in part, on our assessment of market

conditions, pricing of options, related risks, and other factors. The Fund will limit option writing to an aggregate net notional amount less than the value of the

Fund’s equity securities in order to allow the Fund potentially to benefit from capital gains on its equity sleeve. The aggregate net notional amount of the open option

positions sold by the Fund will never exceed the market value of the Fund’s equity investments. For these purposes, the Fund treats options on indices as being written

on securities having an aggregate value equal to the face or notional amount of the index subject to the option. At any time we may limit, or temporarily suspend, the option

strategy.

We will attempt to maintain for the Fund written call option positions on equity indices whose

price movements, taken in the aggregate, correlate to some degree with the price movements of some or all of the equity securities held in the Fund’s equity sleeve. The

Fund may write index call options that are “European style” options, meaning that the options may be exercised only on the expiration date of the option. The Fund

also may write index call options that are “American style” options, meaning that the options may be exercised at any point up to and including the expiration

date. The Fund expects to use primarily listed/ exchange-traded options contracts and may also use unlisted (or “over-the-counter”) options.

We will actively manage the Fund’s options positions using a proprietary quantitative and

statistical analysis in an attempt to identify option transactions for the Fund that produce attractive current income for the Fund with appropriate limitations on the

potential losses to the Fund from those transactions. We may attempt to preserve for the Fund the potential to realize a portion of any increases in the values of its

portfolio securities by writing options that are out-of-the-money (that is, whose strike price is higher than the current market value or level of the underlying index), by

limiting the amount of options the Fund writes, and by attempting, through use of quantitative and statistical analysis, to identify options that are likely to provide

current income without undue risk of an untimely exercise.

Material Changes During the Fiscal Year ended October 31, 2023: There were no material changes to the option sleeve during the fiscal year ended

October 31, 2023.

The Fund’s Overall Portfolio. We monitor the weighting of each investment

strategy within the Fund’s portfolio on an ongoing basis and rebalance the Fund’s assets when we determine that such a rebalancing is necessary to align the

portfolio in accordance with the investment strategies described above. From time to time, we may make adjustments to the weighting of each investment strategy. Such

adjustments would be based on our review and consideration of the expected returns for each investment strategy and would factor in the stock, bond and money markets,

interest rate and corporate earnings growth trends, and economic conditions which support changing investment opportunities.

Allspring Global Dividend Opportunity Fund | 13

Objective, strategies and risks (unaudited)

The Fund

currently utilizes leverage principally through bank borrowings. The Fund may also enter into transactions including, among others, options, futures and forward contracts,

loans of portfolio securities, swap contracts, and other derivatives, as well as when-issued, delayed delivery, or forward commitment transactions, that may in some

circumstances give rise to a form of leverage. The Fund may use some or all of these transactions from time to time in the management of its portfolio, for hedging purposes,

to adjust portfolio characteristics, or more generally for purposes of attempting to increase the Fund’s investment return. There can be no assurance that the Fund will

enter into any such transactions at any particular time or under any specific circumstances. By using leverage, the Fund seeks to obtain a higher return for holders of common

shares than if it did not use leverage. Leveraging is a speculative technique, and there are special risks involved. There can be no assurance that the leveraging strategies

employed by the Fund, will be successful, and such strategies can result in losses to the Fund.

The investment policies of the Fund described above are non-fundamental and may be changed by the

Board of Trustees of the Fund so long as shareholders are provided with at least 60 days prior written notice of any change to the extent required by the rules under the 1940

Act.

Other investment techniques and strategies

As part of or in addition to the principal investment strategies discussed above, the Fund may at times invest a

portion of its assets in the investment strategies and may use certain investment techniques as described below.

Preferred Shares. The Fund may invest in preferred shares. Preferred shares are equity securities, but they have many characteristics of fixed income securities, such as a fixed dividend payment rate and/or a liquidity preference over the issuer’s common shares. However, because preferred shares are equity securities, they may be more susceptible to risks traditionally associated with equity investments than the Fund’s fixed income securities.

Real Estate Investment Trusts. The Fund may invest a portion of its assets in real estate investment trusts (“REITs”). REITs primarily invest in income-producing real estate or real estate related loans or interests. REITs are generally classified as equity REITs, mortgage REITs, or a combination of equity and mortgage REITs. Equity REITs invest the majority of their assets directly in real property and derive income primarily from the collection of rents. Equity REITs can also realize capital gains by selling properties that have appreciated in value. Mortgage REITs invest the majority of their assets in real estate mortgages and derive income from the collection of interest payments. The Fund will indirectly bear its proportionate share of any management and other expenses paid by REITs in which it invests in addition to the expenses paid by the Fund. Distributions received by the Fund from REITs may consist of dividends, capital gains, and/or return of capital.

Loans. The high yield sleeve of the Fund may invest in direct debt instruments

which are interests in amounts owed to lenders by corporate or other borrowers. The loans in which the sleeve invests primarily consist of direct obligations of a borrower.

The high yield sleeve of the Fund may invest in a loan at origination as a co-lender or by acquiring in the secondary market participations in, assignments of or novations of

a corporate loan. By purchasing a participation, the high yield sleeve of the Fund acquires some or all of the interest of a bank or other lending institution in a loan to a

borrower. The participations typically will result in the Fund having a contractual relationship only with the lender, not the borrower. The Fund will have the right to

receive payments of principal, interest and any fees to which it is entitled only from the lender selling the participation and only upon receipt by the lender of the payments from the borrower. Many such loans are secured, although some may be unsecured. Loans that are fully secured offer the Fund more protection than an unsecured loan in the event of non-payment of scheduled interest or principal. However, there is no assurance that the liquidation of collateral from a secured loan would satisfy the corporate borrower’s obligation, or that the collateral can be liquidated. Direct debt instruments may involve a risk of loss in case of default or insolvency of the borrower and may offer less legal protection to the Fund in the event of fraud or misrepresentation. In addition, loan participations involve a risk of insolvency of the lending bank or other financial intermediary. The markets in loans are not regulated by federal securities laws or the U.S. Securities and Exchange Commission.

Asset-Backed Securities. Asset-backed securities are securities that represent

a participation in, or are secured by and payable from, a stream of payments generated by particular assets, most often a pool or pools of similar assets (e.g., trade

receivables). The credit quality of these securities depends primarily upon the quality of the underlying assets and the level of credit support and/or enhancement

provided.

The underlying assets (e.g., loans) are subject to prepayments which

shorten the securities’ weighted average maturity and may lower their return. If the credit support or enhancement is exhausted, losses or delays in payment may result

if the required payments of principal and interest are not made. The value of these securities also may change because of changes in the market’s perception of the

creditworthiness of the servicing agent for the pool, the originator of the pool, or the financial institution or Fund providing the credit support or

enhancement.

Derivatives. The Fund may purchase and sell derivative instruments such as exchange-listed and over-the-counter put and call options on securities, financial futures, equity, fixed-income and interest rate indices, and other financial instruments, purchase and sell financial futures contracts and options thereon, and enter into various interest rate transactions such as swaps, caps, floors or collars. The Fund also may purchase derivative instruments that combine features of these instruments. Collectively, all of the above are referred to as “derivatives.” The Fund generally seeks to use derivatives as a portfolio management or hedging technique to seek to protect against possible adverse changes in the market value of securities held in or to be purchased for the Fund’s portfolio, protect the value of the Fund’s portfolio, facilitate the sale of certain securities for investment purposes, manage the effective interest rate exposure of the Fund, manage the effective maturity or duration of the Fund’s portfolio, or establish positions in the derivatives markets as a temporary substitute for purchasing or selling particular securities.

The Fund may use a variety of other derivative instruments (including both long and short positions) for hedging purposes, to adjust portfolio

14 | Allspring Global Dividend Opportunity Fund

Objective, strategies and risks (unaudited)

characteristics, or more generally for purposes of attempting to increase the Fund’s investment return,

including, for example, buying and selling call and put options, buying and selling futures contracts and options on futures contracts, and entering into forward contracts

and swap agreements with respect to securities, indices, and currencies. There can be no assurance that the Fund will enter into any such transaction at any particular time

or under any specific circumstances.

With respect to the high yield sleeve, investments in derivatives are limited to 10% of the sleeve’s total assets in futures and options on securities and indices and in other derivatives. In addition, the sleeve may enter into interest rate swap transactions with respect to the total amount the high yield sleeve is leveraged in order to hedge against adverse changes in interest rates affecting dividends payable on any preferred shares or interest payable on borrowings constituting leverage. In connection with any such swap transaction, the Fund will segregate liquid securities in the amount of its obligations under the transaction.

The high yield sleeve does not use derivatives as a primary investment technique and generally

does not anticipate using derivatives for non-hedging purposes. In the event the sleeve uses derivatives for non-hedging purposes, no more than 3% of the sleeve’s total

assets will be committed to initial margin for derivatives for such purposes. The sleeve may use derivatives for a variety of purposes, including as a hedge against adverse

changes in securities market prices or interest rates and as a substitute for purchasing or selling securities.

Futures Contracts. In addition to the strategies described above, the Fund may purchase or sell futures contracts on foreign securities indices and other assets. The Fund may use futures contracts for hedging purposes, to adjust portfolio characteristics, or more generally for purposes of attempting to increase the Fund’s investment return.

Other Investment Companies. The Fund may invest in shares of other affiliated

or unaffiliated open-end investment companies (i.e., mutual funds), closed-end funds, exchange-traded funds (“ETFs”), UCITS funds (pooled investment vehicles

established in accordance with the Undertaking for Collective Investment in Transferable Securities adopted by European Union member states) and business development

companies. The Fund may invest in securities of other investment companies up to the limits prescribed in Section 12(d) under the 1940 Act, the rules and regulations

thereunder and any exemptive relief currently or in the future available to a Fund.

Repurchase Agreements. The Fund may enter into repurchase agreements with

broker-dealers, member banks of the Federal Reserve System and other financial institutions. Repurchase agreements are arrangements under which the Fund purchases securities

and the seller agrees to repurchase the securities within a specific time and at a specific price. We review and monitor the creditworthiness of any institution which enters

into a repurchase agreement with the Fund. The counterparty’s obligations under the repurchase agreement are collateralized with U.S. Treasury and/or agency obligations with a market value of not less than 100% of the obligations, valued daily. Collateral is held by the Fund’s custodian in a segregated, safekeeping account for the benefit of the Fund. Repurchase agreements afford the Fund an opportunity to earn income on temporarily available cash at low risk. In the event that the counterparty to a repurchase agreement is unwilling or unable to fulfill its contractual obligations to repurchase the underlying security, the Fund may lose money, suffer delays, or incur costs arising from holding or selling the underlying security.

Reverse Repurchase Agreements. The Fund may enter into reverse repurchase agreements under which the Fund sells portfolio securities and agrees to repurchase them at an agreed-upon future date and price. Use of a reverse repurchase agreement may be preferable to a regular sale and later repurchase of securities, because it avoids certain market risks and transaction costs. At the time the Fund enters into a reverse repurchase agreement, it will segregate cash or other liquid assets having a value equal to or greater than the repurchase price (including accrued interest), and will subsequently monitor the account to ensure that the value of such segregated assets continues to be equal to or greater than the repurchase price. In the event that the buyer of securities under a reverse repurchase agreement files for bankruptcy or becomes insolvent, the Fund’s use of proceeds from the agreement may be restricted pending a determination by the other party, or its trustee or receiver, whether to enforce the Fund’s obligation to repurchase the securities. Reverse repurchase agreements may be viewed as a form of borrowing.

Private Placements. The Fund may invest in private placements and other

“restricted” securities. Private placement securities are securities sold in offerings that are exempt from registration under the Securities Act of 1933, as

amended (the “1933 Act”). They are generally eligible for sale only to certain eligible investors. Private placements often may offer attractive opportunities for

investment not otherwise available on the open market. However, private placement and other restricted securities typically cannot be resold without registration under the

1933 Act or the availability of an exemption from registration (such as Rules 144A), and may not be readily marketable because they are subject to legal or contractual delays

in or restrictions on resale. Because there may be relatively few potential qualified purchasers for such securities, especially under adverse market or economic conditions, or in the event of adverse changes in the financial condition of the issuer, the Fund could find it more difficult to sell such securities when it may be advisable to do so or it may be able to sell such securities only at prices lower than if such securities were more widely held and traded. Delay or difficulty in selling such securities may result in a loss to the Fund.

Securities Lending. While not currently engaged in securities lending, the Fund

retains the ability to do so in order to earn additional income in the form of fees or interest on securities received as collateral or the investment of any cash received as

collateral. When securities are on loan, the Fund receives interest or dividends on those securities. In a securities lending transaction, the net asset value of the Fund is

affected by an increase or decrease in the value of the securities loaned and by an increase or decrease in the value of the instrument in which collateral is invested. The

amount of securities lending activity undertaken by the Fund fluctuates from time to time. The Fund has the right under the lending agreement to recover the securities from

the borrower on demand. In the event of default or bankruptcy by the borrower, the Fund may be prevented from recovering the loaned securities or

Allspring Global Dividend Opportunity Fund | 15

Objective, strategies and risks (unaudited)

gaining

access to the collateral or may experience delays or costs in doing so. In such an event, the terms of the agreement allows the unaffiliated securities lending agent to use

the collateral to purchase replacement securities on behalf of the Fund or pay the Fund the market value of the loaned securities. The Fund bears the risk of loss with

respect to depreciation of its investment of the cash collateral.

Defensive and Temporary Investments. The Fund may hold some of its assets in cash or in money market instruments, including U.S. Government

obligations, shares of other mutual funds and repurchase agreements, or make other short-term investments for purposes of maintaining liquidity or for short-term defensive purposes when we believe it is in the best interests of the shareholders to do so. During these periods, the Fund may not achieve its objective.

Portfolio Turnover. It is the policy of the Fund not to engage in trading for

short-term profits although portfolio turnover is not considered a limiting factor in the execution of investment decisions for the Fund.

Principal risks

An investment in the Fund may lose money, is not a deposit of a bank, is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, and is primarily subject to the risks briefly summarized below.

Market Risk. The values of, and/or the income generated by, securities held by

a Fund may decline due to general market conditions or other factors, including those directly involving the issuers of such securities. Securities markets are volatile and

may decline significantly in response to adverse issuer, regulatory, political, or economic developments. Different sectors of the market and different security types may

react differently to such developments. Political, geopolitical, natural and other events, including war, terrorism, trade disputes, government shutdowns, market closures,

inflation, natural and environmental disasters, epidemics, pandemics and other public health crises and related events have led, and in the future may lead, to economic uncertainty, decreased economic activity, increased market volatility and other disruptive effects on U.S. and global economies and markets. Such events may have significant adverse direct or indirect effects on a Fund and its investments. In addition, economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions.

Equity Securities Risk. The values of equity securities may experience periods

of substantial price volatility and may decline significantly over short time periods. In general, the values of equity securities are more volatile than those of debt

securities. Equity securities fluctuate in value and price in response to factors specific to the issuer of the security, such as management performance, financial condition,

and market demand for the issuer’s products or services, as well as factors unrelated to the fundamental condition of the issuer, including general market, economic and

political conditions. Investing in equity securities poses risks specific to an issuer, as well as to the particular type of company issuing the equity securities. For

example, investing in the equity securities of small- or mid-capitalization companies can involve greater risk than is customarily associated with investing in stocks of

larger, more-established companies. Different parts of a market, industry and sector may react differently to adverse issuer, market, regulatory, political, and economic developments. Negative news or a poor outlook for a particular industry or sector can cause the share prices of securities of companies in that industry or sector to decline. This risk may be heightened for a Fund that invests a substantial portion of its assets in a particular industry or sector.

Foreign Investment Risk. Foreign investments may be subject to lower liquidity, greater price volatility and risks related to adverse political, regulatory, market or economic developments. Foreign companies may be subject to significantly higher levels of taxation than U.S. companies, including potentially confiscatory levels of taxation, thereby reducing the earnings potential of such foreign companies. Foreign investments may involve exposure to changes in foreign currency exchange rates. Such changes may reduce the U.S. dollar value of the investments. Foreign investments may be subject to additional risks, such as potentially higher withholding and other taxes, and may also be subject to greater trade settlement, custodial, and other operational risks than domestic investments. Certain foreign markets may also be characterized by less stringent investor protection and disclosure standards.

Debt Securities Risk. Debt securities are subject to credit risk and interest

rate risk. Credit risk is the possibility that the issuer or guarantor of a debt security may be unable, or perceived to be unable or unwilling, to pay interest or repay

principal when they become due. In these instances, the value of an investment could decline and the Fund could lose money. Credit risk increases as an issuer’s credit

quality or financial strength declines. The credit quality of a debt security may deteriorate rapidly and cause significant deterioration in the Fund’s net asset value.

Interest rate risk is the possibility that interest rates will change over time. When interest rates rise, the value of debt securities tends to fall. The longer the terms of

the debt securities held by a Fund, the more the Fund is subject to this risk. If interest rates decline, interest that the Fund is able to earn on its investments in debt

securities may also decline, which could cause the Fund to reduce the dividends it pays to shareholders, but the value of those securities may increase. Some debt securities

give the issuers the option to call, redeem or prepay the securities before their maturity dates. If an issuer calls, redeems or prepays a debt security during a time of declining interest rates, the Fund might have to reinvest the proceeds in a security offering a lower yield, and therefore might not benefit from any increase in value as a result of declining interest rates. Very low or negative interest rates may magnify interest rate risk. Changing interest rates, including rates that fall below zero, may have unpredictable effects on markets, may result in heightened market volatility and may detract from Fund performance to the extent the Fund is exposed to such interest rates. Interest rate changes and their impact on the Fund and its share price can be sudden and unpredictable. Changes in market conditions and government policies may lead to periods of heightened volatility in the debt securities market, reduced liquidity Fund investments and an increase in Fund redemptions.

16 | Allspring Global Dividend Opportunity Fund

Objective, strategies and risks (unaudited)

High Yield Securities Risk. High yield securities and unrated securities of