UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

or

☐ TRANSITION REPORT UNDER SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from

to

Commission file number: 001-41323

SOLIDION TECHNOLOGY, INC.

(Exact name of registrant as specified in its

charter)

| Delaware | | 87-1993879 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

13355 Noel Rd, Suite 1100 Dallas, TX | | 75240 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including

area code: (972) 918-5120

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, par value $0.0001 per share | | STI | | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g)

of the Act: None.

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant

(1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes

☒ No ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | | Emerging Growth Company | ☒ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or

issued its audit report. ☐

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error

corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s

executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☒ No ☐

At June 30, 2023, the last business day of the

registrant’s most recently completed second fiscal quarter, the aggregate market value of the common stock of the registrant held

by non-affiliates of the registrant was $41,430,352.

As of April 11, 2024, there were 86,900,398 shares of common stock

of the Company issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this

Report, to the extent not set forth herein, is incorporated herein by reference from the registrant’s definitive proxy statement

relating to the Annual Meeting of Stockholders to be held in 2024, which definitive proxy statement shall be filed with the Securities

and Exchange Commission no later than 120 days after the close of the fiscal year ended December 31, 2023.

EXPLANATORY NOTE

On February 2, 2024 (the “Closing Date”),

Nubia Brand International Corp., a Delaware corporation (“Nubia” and after the Transactions described herein, the “Combined

Company” or “Solidion Technology, Inc.”), consummated the previously announced business combination (the “Closing”)

pursuant to a Merger Agreement (as amended on August 25, 2023, the “Merger Agreement”), by and among Nubia, Honeycomb Battery

Company, an Ohio corporation (“HBC”), and Nubia Merger Sub, Inc., an Ohio corporation and wholly-owned subsidiary of Nubia

(“Merger Sub”). Pursuant to the Merger Agreement, Merger Sub merged with and into HBC (the “Merger,” and the

transactions contemplated by the Merger Agreement, the “Transactions”), with HBC surviving such merger as a wholly owned

subsidiary of Nubia, which was renamed “Solidion Technology, Inc.” upon Closing.

Unless the context otherwise requires, the “registrant” and the “Company” refer to Nubia prior to the Closing

and to the Combined Company and its subsidiaries following the Closing and “HBC” and “Honeycomb” refers to Honeycomb

Battery Company and its subsidiaries prior to the Closing and the business of the Combined Company and its subsidiaries following

the Closing. Unless otherwise defined herein, capitalized terms used in this Current Report on Form 8-K have the same meaning as set

forth in the definitive proxy statement (the “Proxy Statement”) filed with the Securities and Exchange Commission (the “SEC”)

on November 8, 2023 by Nubia.

The Company’s common stock, par value

$0.0001 per share (the “Common Stock”), is now listed on The Nasdaq Stock Market LLC (“NASDAQ Global”) under

the symbol “STI”. The Company's Public Warrants to purchase Common Stock at an exercise price of $11.50 per share,

previously listed under ticker “NUBIW”, were delisted from the Nasdaq and pending listing on The OTC Markets under the

symbol “STIW”. The audited financial statements included herein are those of Nubia prior to the consummation of the

Business Combination and the name change. Prior to the Business Combination, Nubia neither engaged in any operations nor generated

any revenue. Until the Business Combination, based on Nubia’s business activities, Nubia was a “shell company” as

defined under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

SOLIDION TECHNOLOGY,

INC.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2023

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains

forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, or the Securities Act, and Section 21E

of the Securities Exchange Act of 1934, or the Exchange Act. The statements contained in this report that are not purely historical are

forward-looking statements. Our forward-looking statements include, but are not limited to, statements regarding our or our management’s

expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts

or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The

words “anticipates,” “believe,” “continue,” “could,” “estimate,” “expect,”

“intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,”

“project,” “should,” “would” and similar expressions may identify forward-looking statements, but

the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this report may include,

for example, statements about our:

| ● | our

financial and business performance, including financial and business metrics; |

| ● | changes

in our strategy, future operations, financial position, estimated revenues and losses, projected

costs, prospects and plans; |

| ● | our

ability to develop a high-volume manufacturing line and otherwise scale in a cost-effective

manner; |

| ● | our

ability to add manufacturing capacity and the costs and timing to add such capacity; |

| ● | the

expected addressable market for our products; |

| ● | developments

relating to our competitors and industry; |

| ● | our

expectations regarding our ability to obtain and maintain intellectual property protection

and not infringe on the rights of others; |

| ● | our

future capital requirements and sources and uses of cash; |

| ● | our

ability to obtain funding for our operations; |

| ● | our

business, expansion plans and opportunities; and |

| ● | the

outcome of any known and unknown litigation and regulatory proceedings. |

The forward-looking statements contained in this

report are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can

be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve

a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance

to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include,

but are not limited to, those factors described under the heading “Risk Factors.” Should one or more of these risks or uncertainties

materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these

forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise, except as may be required under applicable laws.

As a result of a number of known and unknown

risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking

statements. Some factors that could cause actual results to differ include:

| ● | our

ability to execute our business model, including scaling production and increasing the addressable

market for our products and services; |

| ● | our

ability to raise capital; |

| ● | the

outcome of any legal proceedings that may be instituted against us; |

| ● | the

ability to maintain the listing of our securities on the Nasdaq; |

| ● | the

possibility that we may be adversely affected by other economic, business or competitive

factors, including supply chain interruptions, and may not be able to manage other risks

and uncertainties; |

| ● | changes

in applicable laws or regulations; |

| ● | the

possibility that we may be adversely affected by other economic, business, and/or competitive

factors; and |

| ● | other

risks and uncertainties described in this Annual Report on Form 10-K, including risk factors

discussed in Part I, Item 1A under the Heading, “Risk Factors”. |

PART I

ITEM 1. BUSINESS

In this Annual Report on Form 10-K (the

“Form 10-K”), references to the “Company” and to “Solidion” “we,” “us,”

and “our” refer to Solidion Technology, Inc.

Corporate History and Background

We were originally incorporated in Delaware on

June 14, 2021 under the name “Nubia Brand International Corp.” as a special purpose acquisition company, formed for the purpose

of effecting an initial business combination with one or more target businesses. On March 14, 2022 (the “IPO Closing Date”),

we consummated our initial public offering (the “IPO”). On February 2, 2024, we consummated the previously announced business

combination (the “Closing”) pursuant to a Merger Agreement, dated February 16, 2023 (as amended on August 25, 2023, the “Merger

Agreement”), by and among Nubia, Honeycomb Battery Company, an Ohio corporation (“HBC”), and Nubia Merger Sub, Inc.,

an Ohio corporation and wholly-owned subsidiary of Nubia (“Merger Sub”). Pursuant to the Merger Agreement, Merger Sub merged

with and into HBC (the “Merger,” and the transactions contemplated by the Merger Agreement, the “Transactions”),

with HBC surviving such merger as a wholly owned subsidiary of Nubia, which was renamed “Solidion Technology, Inc.” upon

Closing and we became the owner, directly or indirectly, of all of the equity interests of Honeycomb Battery Company and its subsidiaries.

In light of the fact that the Business Combination has closed and our ongoing business will be the business formerly operated by HBC,

this business section primarily includes information regarding HBC’s business.

Overview

Solidion

Technology, Inc, previously known as “Honeycomb Battery Company”, formerly the

energy solutions division of Global Graphene Group, Inc. (“G3”), is a Dallas,

TX, USA-based advanced battery technology company focused on the development and commercialization

of battery materials, components, cells, and selected module/pack technologies. The cofounder

of Solidion, Dr. Bor Z Jang, filed a U.S. patent application on graphene in 2002.

The research and development team led by cofounder Dr. Aruna Zhamu and Dr. Jang

invented graphene-enhanced batteries and built the world’s first manufacturing facility

for graphene-enabled silicon anode materials for lithium-ion batteries.

Solidion is recognized as a global leader in

intellectual property (“IP”) in both the high-capacity anode and the high-energy solid-state battery, as recognized by KnowMade,

a French company that specializes in research and analysis of scientific and patent information. Solidion is uniquely positioned to offer

advanced anode materials (delivering a specific capacity from 300 to 3,500+ milliampere-hours per gram mass (“mAh/g”))

as well as silicon-rich all-solid-state lithium-ion cells, anodeless lithium metal cells, and lithium-sulfur cells, each featuring an

advanced polymer or hybrid solid electrolyte that is most process-friendly. Subject to the Supply and License Agreement between G3 and

Solidion, which limits the manufacture of graphene and graphite products for use in our battery-related products and prohibits resale

to third parties, we believe we are well positioned to supply graphite-based anode materials from sustainable sources.

Our all-solid-state battery platform technology

is capable of transforming the entire electric vehicle (“EV”) battery space into a solid-state battery industry. We provide

solid-state cells that can be manufactured at scale using current lithium-ion cell production facilities, requiring no new design, no

new infrastructure, and no new supply chain. Our batteries are capable of delivering significantly extended EV range, improved battery

safety, lower cost per kilowatt hour, fastest time-to-market, and enable next-gen cathodes with the potential to replace expensive nickel

and cobalt with sulfur (S) and other more abundant elements.

We hold a total of over 520 patents (355 in the

United States and 165+ foreign patents) for next-gen batteries. KnowMade has acknowledged us as one of the two U.S.-based leaders

in solid-state electrolytes, as well as ranked us as the top company in the United States and top battery startup in the world in

silicon anode technology. Additionally, Lexis/Nexis has recognized us as a Global Top 100 Innovator.

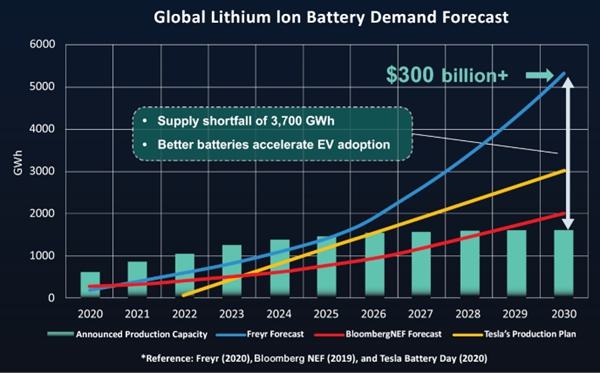

Industry Background

Vehicle electrification provides once-in-a-century

market opportunity, with an over $300 billion EV battery market by 2030. Transportation electrification has triggered a

new run of battery sourcing competition, with potentially up to approximately 5,300 GWh lithium battery demand by 2030, a 500%+ increase

from 2020, and a predicted supply shortfall of approximately 3,700 GWh (Fig. 1). In addition, battery-grade graphite demand is expected

to grow by a factor of 10x from 2019 to 2030. Graphite anode in batteries is expected to grow from 170,000 MT in 2018 to 2.23 million

MT in 2028.

Fig. 1 Global lithium-ion battery demand forecast

The battery technologies developed by Solidion

are aimed at addressing today’s EV battery challenges: the need for increased energy density, fire safety, fast charging and lower

cost.

Today’s EV batteries are largely based

on the lithium-ion cells wherein each cell is typically composed of an anode (negative electrode), a cathode (positive electrode), a

separator that electrically isolates the two electrodes, and a liquid electrolyte that permeates into both electrodes and provides a

medium through which lithium ions can whim back and forth between the anode and the cathode. These essential components are encased in

a protective housing, allowing two terminals to protrude out of the housing for connecting to an external circuit.

The incumbent anode material is graphite that

stores lithium ions to a theoretical specific capacity of 372 mAh/g (practically 340-360 mAh/g). A lithium-ion cell, having

a graphite anode and a lithium nickel cobalt manganese oxide cathode (NCM, 175-200 mAh/g), provides a specific energy of typically 220-250

watt-hours per kilogram (“Wh/kg”). By replacing graphite with silicon (Si), having a theoretical specific capacity of 3,580-4,000

mAh/g, one can obtain a cell having an energy density of 350-400 Wh/kg.

Large shortfall in global graphite anode

material supply. Anticipated shortfalls, relying on data from Benchmark Mineral Intelligence and estimations from peers, in graphite

anode material supply are approximately 400kt and 300kt in 2025 and 2030, respectively, within North America. Mining of natural graphite

and production of artificial graphite from petroleum or coal sources are generally viewed as not environmentally benign, and sustainable

sources of graphite are preferable. Market forecasters predict graphite demand from battery makers will grow by 23% – 27% each

year through 2028 and that planned capacity and projects in development will not be able to meet forecasted demand as soon as 2025. New

markets for EV and flame-retardant building materials (“FRBM”) are driving the demand forecast above existing and new sources

of supply of graphite.

None of the top 10 graphite suppliers is

located in North America. All of the top 10 global graphite anode material suppliers are based in Asia. Significant graphite

manufacturing capacity is needed in North America to fill the gap between North American supply and demand. We are well positioned to

be a leading supplier of various anode materials in North America and other regions. Solidion management team has worked in the

field of carbon and graphite materials for over 30 years, and the first to convert graphite to graphene. The team began to work

on the development of advanced graphite-, silicon oxide-, and silicon-based anode active materials for lithium-ion cells, and protected

lithium metal-based anodes in 2007 and it believes it has established the best IP portfolio in this space. The Supply and License Agreement

allows Solidion to manufacture graphene and graphite products for use in our battery-related products and prohibits resale of the manufactured

graphene and graphite products other than after modification to create electrode materials.

Current solid-state lithium metal batteries

are incompatible with current lithium-ion cell production equipment. This is the major barrier to widespread adoption. Oxide-based

sintered ceramic separators are brittle, expensive, and difficult to fabricate. Several technical issues, such as high interfacial impedance,

high stack-holding pressure, and low active material proportion, remain to be resolved.

Graphite may be replaced with lithium metal (Li)

in the anode to obtain a lithium metal battery, which is commonly believed to be capable of delivering an energy density in the range

of 400-500 Wh/kg, depending upon the cathode material used. However, such a potential benefit does not come without challenges.

During the charge-discharge cycles of a lithium metal cell, a needle-like feature called “lithium dendrites” may form on

the lithium metal in the anode. The dendrite can penetrate through a separator and reach the cathode side to cause internal shorting,

which poses fire and explosion hazards. In addition, repeated reactions between lithium and liquid electrolyte continue to consume both

the active lithium ions and the liquid electrolyte, leading to rapid capacity decay. These issues have thus far impeded the practical

utilization of lithium metal batteries to replace the conventional lithium-ion batteries for EV application. Solidion has been developing

lithium metal protection strategies aiming to address these technical issues.

The safety of lithium-ion or lithium metal batteries

hinges upon the availability of a non-flammable electrolyte. The liquid electrolytes commonly utilized in current lithium-ion batteries

contain a lithium salt dissolved in an organic solvent, which contains volatile molecules that can catch fire. In contrast, various types

of solid-state electrolytes, comprising less or no volatile chemical species, are being developed for both lithium-ion and lithium-metal

battery types. Further, solid-state electrolytes, when used as a separator, could significantly reduce or eliminate the lithium dendrite

issues.

However, solid-state electrolytes bring along

other types of challenges to a battery designer, including a higher internal impedance (hence, lower power), lower anode or cathode active

material proportion (hence, lower-than-expected energy density), and a higher manufacturing cost. The latter challenge is largely a result

of the need to develop a new process and new equipment for producing the solid-state separator and for assembling the required components

into a battery cell.

Solidion has been developing two types of quasi-solid

or hybrid electrolytes, which are expected to have more practical manufacturability-at-scale — “solvent-in-salt”

and “solvent-in-polymer” electrolytes. Solidion’s effort also includes development of a versatile solid-state electrolyte

technology. Solidion’s electrolytes (FireShieldTM) aim to be process-friendly and compatible with current lithium-ion

cell manufacturing processes. Specifically, Solidion’s developments are focused to provide a disruptive material process technology

that would enable current lithium-ion cell manufacturing facilities to produce solid-state or quasi-solid electrolyte-based safe lithium

batteries without the need to significantly change existing equipment and facilities. This implies that the lithium-ion battery industry

can readily enjoy the benefits of solid-state, lithium metal batteries essentially immediately, not having to wait for a decade.

Solidion’s battery technology

is targeting to enable significant benefits across battery capacity, life, safety, and fast charging while minimizing cost. Solidion

is getting ready to commercialize the graphene-protected lithium metal anode technology, which is essential to the accelerated emergence

of a lithium metal battery industry. The process-friendly electrolytes are also ready to solidify Solidion’s leadership

position in converting the entire lithium battery industry into a quasi-solid and solid-state status.

In the automotive industry, most of the EV makers

are highly interested in silicon- and lithium metal-based anodes for improved EV driving range given the same battery weight or volume.

For instance, GM is experimenting with silicon-rich and lithium metal anodes, solid state and high voltage electrolytes, and dry processing

of electrodes for its next generation of Ultium batteries, due around 2025. Ford, VW and BMW are also working with battery start-ups

on the development of solid-state lithium metal and Si-based anodes.

Summary of EV Battery Market Demands

As discussed above, a lithium cell supply shortfall

of ~3,700 GWh by 2030 is projected. Also forecasted is a worldwide graphite supply shortage of 1.4 million tons/year by 2028. Mining

of natural graphite and production of artificial graphite from petroleum or coal sources are generally viewed as not environmentally

benign. The market demands Sustainable sources of graphite. The EV industry is aware of the potential shortage of critical elements such

as cobalt (Co) and nickel (Ni) that are commonly used in the cathode of a lithium-ion cell; alternative cathode materials are key to

a sustaining EV battery industry. The EV market is highly interested in next-gen batteries that exhibit the following features:

| |

● |

Significantly extended

driving range on one battery charge, which would alleviate range anxiety; |

| |

● |

Readily available solid-state

performance; |

| |

● |

Safer battery system without

fire or explosion hazards; |

| |

● |

Fast chargeability, with

a goal of achieving a charge to 80% in 15 minutes; and |

| |

● |

Lower battery cost, with

a goal of less than $100 per kilowatt-hour. |

EV batteries are required to meet stringent criteria,

including higher energy density to enable extended driving range, utilization of safer quasi-solid or solid-state electrolytes to enhance

safety, enhanced designs at various levels including material, cell, and module/pack, to facilitate fast charging, and reduced costs

per kilowatt-hour (kWh) for both anode and cathode materials to lower overall battery costs. Over the course of 15 years, Solidion has

focused its battery research and development endeavors precisely on tackling these challenges head-on.

Our Technologies and Products

Anode active materials

Our products include graphite-based anode materials.

What makes us be different from other manufacturers would be that we will have the flexibility to use raw materials from sustainable

sources. In order to reach the ambitious goal of net zero greenhouse gas emission by 2050, thorough examination of the entire supply

chain line can show insufficiencies. With the increasing trend of EVs on the road, proliferation of renewable energy – battery

systems, the scrutiny of battery material production impacts on the environment becomes increasingly relevant. Graphite is currently

indispensable as a battery anode material, dominating the vast majority of the rechargeable battery market due to its long-term cycle

life and low cost of production. Synthetic graphite is currently produced almost exclusively from petroleum coke and pitch. Solidion

proposes to manufacture battery-grade anode materials by introducing renewable and carbon negative biochar produced from waste biomass

as alternative feedstock. By collecting dead trees, trimming, and other waste biomass, the process of creating biochar sequesters the

elemental carbon and prevents the release of carbon as green-house gas through natural decomposition or wildfires. Hence the process

of converting waste biomass to biochar has been shown to be carbon neutral or even negative depending on the end use of the biochar.

Given that biochar when mixed into soil, can remain sequestered for scale of thousand years, it will likely remain as sequestered carbon

in a sealed cell until recycled and reused, hence prolonging its sequestered state. Solidion has developed a process technology that

is expected to allow cost-effective production of anode-grade graphite from this unique sustainable source. Subject to the Supply and

License Agreement we entered into with G3, Solidion is allowed to manufacture graphene and graphite products for use in our battery-related

products and prohibits resale of the manufactured graphene and graphite products other than after modification to create electrode materials.

Solidion has also developed a cost-effective

graphene/silicon or graphene/SiOx composite anode material that enables a significantly higher energy density (for example, an expected 20-30%

increase in the EV driving range) likely at a reduction in the cell cost in terms of U.S. dollars per kilowatt hour (“kWh”).

Graphene has proven to be effective in resolving the battery capacity decay problem caused by repeated volume expansion/shrinkage of

silicon. Solidion provides silicon-rich or SiOx-rich high-capacity anode materials that exhibit outstanding performance-to-cost ratio

and aims to significantly extend the EV driving range on one battery charge. Additionally, Tesla suggested on its 2020 “Battery

Day” that the best silicon anode should have low-cost silicon particles with a simple design to reduce material cost, instead of

highly engineered structures such as the Chemical Vapor Deposition process (“CVD”) used by our competitors. It should also

have elastic, ion-conducting polymer coating that protects these silicon particles, as well as highly elastic binder and some electrode

design used in the anode to maintain structural integrity of the electrode. We also have patents that cover these desired features of

silicon anode materials.

Safer Batteries

We plan to produce batteries that bridge the

performance and time-to-market gaps. A drop-in solution is expected to be compatible with today’s manufacturing process and

equipment. There are two paths we expect to narrow the gap between today’s battery technology and future solid-state performance:

silicon-rich solid-state lithium-ion cells and solid-state lithium metal batteries, which we expect to be ready for commercialization

in two to three years. Higher energy density and solid-state electrolytes are the key to the next generation of EV batteries. EV

batteries must deliver a higher energy density for extended driving range, contain only safe quasi-solid or solid-state electrolytes

for safety, improved designs at the material-, cell-, and module/pack-levels for fast charging, and lower anode and/or cathode costs

per kilowatt-hour for lower battery costs. Our team’s 15 years of battery research and development efforts have been precisely

directed at addressing these issues. Briefly speaking, we plan to produce the following batteries:

| |

● |

Generation

1: Solid-state lithium-ion cells featuring a silicon-rich anode and a quasi-solid or polymer-inorganic composite electrolyte (intended

to be launched in 2026). |

| |

|

|

| |

● |

Generation 2: Solid-state

lithium metal cells featuring a thin lithium metal anode or an initially lithium metal-free anode (“anode-less”) and

a polymer-inorganic composite electrolyte (expected 2026); and |

| |

|

|

| |

● |

Generation 3: Solid-state

lithium-sulfur cells featuring a lithium metal anode, a sulfur or conversion-type cathode, and an in situ curable polymer-inorganic

composite electrolyte (expected 2027). |

In summary, Solidion has superior technologies

that can be commercialized quickly to solve the EV industry’s most critical issues:

| |

● |

Cost: We believe

that Solidion technology can significantly lower cost/KWh of today’s batteries, accelerating adoption and enabling sustainable

EVs to quickly replace internal combustion engines. We also believe that our battery costs can be lower than those of future solid-state

battery-producing competitors. |

| |

● |

Time-to-market: Solidion’s

solid-state electrolytes are process-friendly, enabling the “future” solid-state batteries to be produced “now”

using existing/current lithium-ion battery production equipment. EV OEMs can utilize existing factories to qualify solid-state batteries

in two to three years, rather than waiting for four to seven years. This is in stark contrast to other solid-state

lithium metal battery companies that will hopefully begin mass production of all solid-state batteries in 2025-30. The implementation

of the conventional solid state battery technology requires large factory infrastructure rebuilds and will take years to develop.

Solidion will use existing factories, saving time to market, cost and supporting supply chain demand faster. |

| |

● |

Driving range: The

solid-state lithium batteries and lithium-sulfur batteries potentially can provide up to a 100% increase in range for the same size

battery, eliminating range anxiety. |

| |

|

|

| |

● |

Safety: Our fire/flame-resistant

quasi-solid and solid-state electrolytes make all types of rechargeable lithium battery safer. |

| |

● |

Battery charging time:

Reducing the recharge time to less than 15 minutes can help drive EV adoption and reduce charging infrastructure challenges. |

| |

● |

Total solutions: Low

costs and high performance of our batteries will make it economically viable for commercializing battery modules/packs for emergency

power applications. These power systems will be capable of connecting to grids and solar/wind-based power sources and will be available

for vehicle-to-home (V2H) charging. |

Apart from the EV sector, Solidion is strategically

exploring entry into diverse markets such as hand-held devices, energy storage systems (ESS), power tools, and e-bikes. We expect our

batteries to be poised to capture substantial market shares owing to their distinct advantages, including cost-effectiveness, superior

charging/discharging performance, safety features, extended cycle-life, and exceptional durability. These attributes are expected to

position us for significant growth and success across multiple sectors.

Summary of Solidion’s products and

stages of development.

| |

● |

Anode active materials: |

| ● | Graphite-based

anode materials (with flexibility to choose raw materials including sustainable sources)

are in the final stage of product development. |

| ● | Graphene-enhanced

silicon oxide ((SiOx) anode materials) are in the final stage of product development. |

| ● | Si-rich

anode materials: Small-scale manufacturing is in progress (currently 15 metric tons per annum

(“MTA”). We are planning expansion to >150 MTA by 2026. |

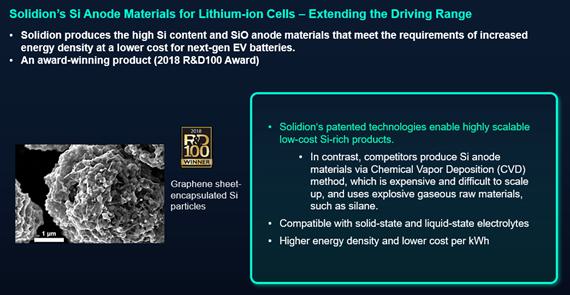

Fig. 2 SEM images of Solidion’s Si-rich

anode materials.

Our Competitive Strengths

In the automotive industry, the price of a vehicle

ultimately dictates the final decision of a potential customer, and the emerging EV industry is no exception. The U.S. DOE and the

EV industry experts have all agreed that EVs will become competitive against the internal combustion engine (ICE) vehicles when the battery

cost reaches a threshold of $100/KWh given comparable performance/safety characteristics.

Si-rich anode materials: The production

of Solidion’s Si-rich anode materials begins with a significantly lower starting material and follows a highly scalable, low-cost

process (Fig. 2). This is in stark contrast to competitors’ use of an expensive, toxic, and explosive gaseous silane and the high-cost

CVD process. According to Tesla’s analysis on its Battery Day in 2020, the CVD Si anode price is estimated to be > $100/KWh,

while Solidion’s product is expected to be lower than $6/kWh, which is approximately the price of currently used graphite anode

materials. Solidion is believed to be capable of cost-effectively producing the high Si content anode materials (graphene/elastomer encapsulated

Si particles, first-cycle efficiency up to 94% and specific capacity of 2,000-3,200 mAh/g) that would meet the requirements of increased

energy density and lower cost for next-gen EV batteries.

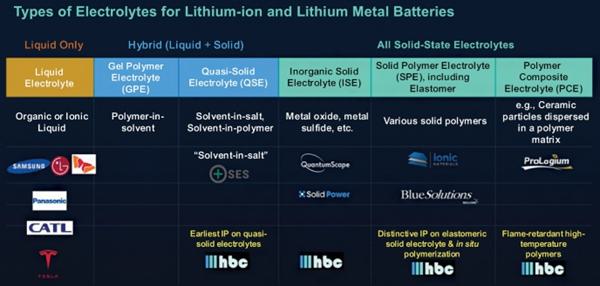

Process-friendly quasi-solid and solid-state

electrolytes: Solidion has been developing a truly disruptive solid-state platform technology that can help solidify the battery

safety of the EV industry. Our key electrolyte technologies may be summarized as follows: (a) we invented elastomeric solid electrolytes;

(b) we have highly significant IP in in-situ curing or in-situ solidification of polymer electrolytes; (c) we

invented quasi-solid electrolytes; (d) we developed thermally stable and flame-retardant polymer and polymer/inorganic hybrid electrolytes;

(e) our electrolytes are compatible with current Li-ion infrastructure and processes; and (f) We have versatile and easy-to-process

solid-state electrolytes for safe lithium-ion and lithium-metal batteries. As summarized in Fig. 3 below, we have earliest IP in quasi-solid

electrolytes (solvent-in-salt and solvent-in-polymer), and strong IP position in solid polymer electrolytes (in situ polymerization and

solid elastomeric electrolytes), and polymer composite electrolytes (elastic, flame-retardant and high-temperature polymer electrolytes).

Fig.3 Types of electrolytes for Li-ion and Li

metal batteries.

Lithium metal cells: Lithium metal

anode protection is key to the commercialization of all-solid-state or liquid-state lithium metal batteries (any battery that makes use

lithium metal as the anode active material; hence, higher energy density). We believe that Solidion has the most significant IP in the

area of lithium metal anode protection (50+ U.S. patents and many foreign patents). Our graphene- and/or polymer-enabled lithium

metal protection technologies aim to overcome technical barriers (for example, lithium dendrites, large interfacial impedance, etc.)

that have thus far impeded commercialization of solid-state lithium metal batteries. We believe that our graphene/polymer-based Li metal

protection layers are key enabling technologies for all types of solid-state lithium metal batteries. For instance, Solidion’s

anode-protecting layers and elastomeric solid electrolytes accelerate commercialization of ultra-thin lithium (Li-light) anode or anodeless

batteries, both featuring reduced cell weight and volume and thus higher energy densities.

Lithium-sulfur and lithium-selenium cells:

Solidion researchers are pioneers in the field of graphene-enabled Li-S and Li-Se batteries, having 50+ U.S. patents and

numerous foreign patents in this subject. In particular, Solidion has developed nanostructured graphene-sulfur cathode that has (a) exceptionally

high sulfur content and utilization efficiency; (b) high specific capacity (up to 1,000 mAh/g); (c) high specific energy (theoretically

capable of up to 500 Wh/kg; over 2x that of traditional lithium-ion cells); and (d) minimal shuttle effect, enabling good cycle-life.

Beyond Lithium Chemistries: Solidion

has also developed impressive technologies in other types of batteries. Solidion is a pioneer in the field of aluminum-ion cells, having

quite likely the most significant IP in this topic. Solidion also has good IP in the sodium-ion cells.

In summary, Solidion is the inventor of many

key enabling battery technologies, including (as examples) graphene-enabled batteries, elastic polymer-protected batteries, quasi-solid

electrolytes, elastomeric solid-state electrolytes, flame-retardant polymer composite electrolytes, graphene-enabled bipolar electrodes

and batteries, etc. This massive IP portfolio provides EV and energy storage systems (ESS) industries with several disruptive battery

technologies, for example, (a) Si-rich anode having a high performance/cost ratio, (b) high-capacity sulfur cathode materials

(Co-, Ni-, and Mn-free), (c) highly process-friendly solid-state electrolytes, (d) protected lithium metal anode, essential

to the success of future lithium metal batteries, (e) fast chargeability, (f) aluminum-ion cells, and (g) sodium-ion cells.

We believe that Solidion’s battery products

have the following features or advantages:

| |

● |

Higher energy density.

Projected 20% to 80% increase in EV driving range to eliminate range anxiety. |

| |

● |

Solid-state performance.

With our target of facilitating the conversion of lithium-ion battery facilities into solid-state lithium battery production

lines we expect Solidion solid-state batteries to become available in two to three years. |

| |

● |

Safety. Quasi-solid

and solid-state electrolytes provide effective solutions to battery fire and explosion issues. |

| |

● |

Lower cost per kilowatt-hour.

We believe our technology could provide a cost advantage as compared to our competitors. We expect our high-capacity

anodes, cathodes, electrolyte technology and unique module/pack-level can result in energy density increases, lower pack system costs,

safety improvements, reduced cooling provisions, eliminated or reduced electrochemical formation, and the ability to use current

lithium-ion cell production equipment, |

| |

● |

Faster charging.

We are developing anode materials designs, innovative cell configurations, and both passive and active thermal management

at both cell- and pack-levels for improved charging speeds. |

Performance Improvements: We anticipate

that our Generation 2 all-solid-state lithium metal cells (expected 2026) and Generation 3 all-solid-state lithium-sulfur cells (expected

2027) would deliver significant performance improvements as compared to current conventional Li-ion cells (Fig. 4). Pack volume in watt

hours per liter (“Wh/L”) is expected to be 480 Wh/L for our 350 liter Generation 2 and 3 products as compared to 250 Wh/L

for current 350 liter Li-ion products. Pack energy, assuming the same pack volume, is expected to be 165 kWh for our Generation 2 and

3 products as compared to 85 kWh for current Li-ion products. Range is expected to be 620 miles for our Generation 2 and 3 products as

compared to 320 miles for current Li-ion products. Charge time is expected to be less than 15 minutes to increase from a 0% to 80% charge

for our Generation 2 and 3 products as compared to greater than 30 minutes to increase from 5% to 80% charge for current Li-ion products.

Power is expected to be 650 kW for our Generation 2 and 3 products as compared to 400 kW for current Li-ion products. Safety is expected

to be much improved through the use of our fire-resistant electrolyte technology in our Generation 2 and 3 products as compared to organic

electrolyte for current Li-ion products.

Fig.4 Comparison of different solid-state battery

cells.

Manufacturing and Supply

Solidion plans to become a supplier of all-solid-state

cells (for the EV, energy storage systems and portable electronics markets) and certain battery components/materials (for example,

graphite-, Si oxide-, and Si-rich anode materials and electrolytes) to select customers or strategic partners.

We have a sustainable graphite anode material

manufacturing plan. We plan to produce biomass-derived graphite anode materials, subject to the Supply and License Agreement, which allows

Solidion to manufacture graphene and graphite products for use in our battery-related products and prohibits resale of the manufactured

graphene and graphite products other than after modification to create electrode materials. During Phase 1, which we expect will

last three years, we intend to source proper biochar products from biochar suppliers and convert these products into graphite anode

materials using a proprietary process. After 3 years, we intend to implement a significantly lower temperature process for reduced

costs. Advantages of biochar as a raw material include sustainability and lower material cost compared to production of graphite from

petroleum or coal sources. In addition, heat treatment equipment for graphite production is available from multiple vendors located in

many counties or regions.

Our business is not raw-material-limited. As

an example, 100,000 tons of graphite requires about 400,000 tons of biomass, which is just 0.015% of the total available source of 2,700 million

tons available per year. 900 million tons of forest residues and wood processing residues combined are available, and an additional

1,800 million tons of biomass feedstock are available from the following species: distillers grains, orchard waste, almond shells,

mixed paper, corn waste, saw dust, switch-grass, cane bagasse, wheat straw, timber, acacia wood waste, fruit bunch, cassava waste and

palm kernel shell.

We expect to scale up our silicon anode material

production capacity from 15 MT per year, currently in Dayton, Ohio, to greater than 150 MT per year by 2026.

We plan to begin with the toll manufacturing/joint

venture (“TM/JV”) model for commercializing the solid-state battery technologies. At a later stage, we may consider building

our own facilities for producing certain specialty cells (such as bipolar or high-voltage cells) responsive to market demands. We expect

the TM/JV partners to acquire silicon-rich anode materials and electrolyte formulations from us as part of the TM/JV agreement. We will

also supply both graphite-dominant and silicon-rich anode materials to customers that choose to use liquid electrolytes in their lithium-ion

cells.

“Made in America” guidance.

On March 31, 2023, the U.S. Treasury Department and the IRS released proposed guidance on the new clean vehicle provisions of

the Inflation Reduction Act. To be eligible for a $7,500 credit, clean vehicles must meet sourcing requirements for both the critical

minerals and battery components contained in the vehicle. Vehicles that meet one of the two requirements are eligible for a $3,750 credit.

To meet the critical mineral requirement and be eligible for a $3,750 credit, an applicable percentage that increases each year of the

value of the critical minerals contained in the battery must be extracted or processed in the United States or a country with which the

United States has a free trade agreement, or be recycled in North America. Critical minerals in the EV battery must be extracted or processed

in the U.S., countries with which the U.S. has a free trade agreement or have been recycled in North America. By the end of 2026, the

applicable percentage will be 80% for the critical mineral requirement.

To meet the battery component requirement and

be eligible for a $3,750 credit, the applicable percentage of the value of the battery components must be manufactured or assembled in

North America — as mandated by the Inflation Reduction Act. By the end of 2026, the applicable percentage will be 80%

for the battery component requirement, and by the end of 2028, 100% of battery components must be manufactured and assembled in North

America by 2028 for a vehicle to be eligible for the clean vehicle tax credit.

In addition, beginning in 2024, an eligible clean

vehicle may not contain any battery components that are manufactured by a foreign entity of concern and beginning in 2025 an eligible

clean vehicle may not contain any critical minerals that were extracted, processed, or recycled by a foreign entity of concern.

We expect that by the end of 2027, 80% of battery

materials and components made by Solidion will comply with the critical mineral and battery component requirements. We believe anode

materials for Lithium-ion cells would be domestically produced from renewable and recycled feedstocks without extraction or mining, and

that sulfur cathode materials will lessen the need for imported manganese, cobalt and nickel. We further believe that Solidion’s

local sourcing and manufacturing ability make it an ideal candidate for government grants and loans. However, there can be no assurance

that we will be able to scale up our production as anticipated in order to supply our battery technology to vehicles that may be eligible

for clean vehicle tax credits.

Summary of research, design, development,

manufacturing and commercialization.

| |

|

Product

Refinement |

|

Manufacturing/Commercialization |

| Pre-Production

(Pilot) |

|

Production |

| Steps |

|

Develop A,

B and C samples to meet technical expectations. |

|

● Design

and evaluate equipment for pilot plant

● Purchase

equipment

● Install

equipment

● Test

run

● Send

samples to customers |

|

● Plant

location survey

● Engineering

design

● Evaluate

equipment

● Purchase

equipment

● Install

equipment

● Test

run

● Send

samples to customers |

| |

|

|

|

|

|

|

| Potential

Material Obstacle |

|

With adequate resources,

we do not anticipate any material technical obstacles. |

|

The lead time of certain

equipment (for example, battery cell production equipment) is excessively long (9 – 18 months). We are interacting

proactively with potential suppliers in multiple regions in the hope of shortening the waiting period. |

|

● Same

lead time issue.

● Certain

production equipment (for example, SiOx production) must be custom-designed. We have started working with selected engineering design

companies and equipment manufacturers to overcome this engineering issue. |

Plans for production.

Synthetic graphite production — For phase

1, we expect to build a processing plant with production capacity of 10,000 MT by 2026, with a projected capital expenditure of $100-200

million and resulting in revenue of $90 – $100 million. We would plan to expand annual capacity to 180,000 MT by 2032.

Anode products — Our Dayton, Ohio, anode

materials production line has a current capacity of 15 MT per year, and we expect to scale it up to a capacity of >150 MT per year

by 2026.

Battery products — We expect to launch

Gen1 and Gen2 cells by 2026 and Gen3 by 2027.

Intellectual Property

Solidion has a portfolio of over 520 patents.

This portfolio contains many key patents for next generation EV batteries. Solidion is the inventor of graphene-enabled batteries, elastic

polymer-protected batteries, quasi-solid electrolytes, elastomeric solid-state electrolytes, advanced polymer/inorganic hybrid electrolytes,

and numerous other disruptive battery technologies. This massive intellectual portfolio provides the EV industry with what we believe

to be several key enabling battery technologies, such as silicon-rich anode having the highest performance/cost ratio, the highest-capacity

sulfur cathode materials (free of cobalt, nickel and manganese), the most process-friendly solid-state electrolytes, protected lithium

metal anode, fast chargeability, aluminum-ion cells and sodium-ion cells. Solidion holds more than 100 key U.S. patents on graphene-

or polymer-enhanced silicon-based materials. It holds more than 35 key U.S. patents on fire-resistant electrolytes for lithium batteries.

It holds more than 70 U.S. patents on key technologies for next-generation all-solid state or lithium metal batteries. It also holds

advanced current collector patents; these technologies are capable of extending cycle life and improving operating temperatures and voltages.

The year of expiration of these key U.S. patents generally ranges from as early as 2028 to as late as 2040. Most of the intellectual

property to be utilized by Solidion is intellectual property that is owned by Solidion (having been transferred from G3 to Solidion via

the Patent Assignment, dated as of February 8, 2023 (the “Patent Assignment”)). Solidion licenses a relatively small number

of patents relating to graphene and graphite production from G3 pursuant to the Supply and License Agreement, under which there are no

significant limitations. These patent rights are licensed on an irrevocable, non-exclusive, royalty-free basis.

We believe we have advanced IP in process-friendly

and cost-effective polymer/inorganic hybrid solid electrolytes that are fire/flame-resistant, which effectively overcomes the fire/explosion

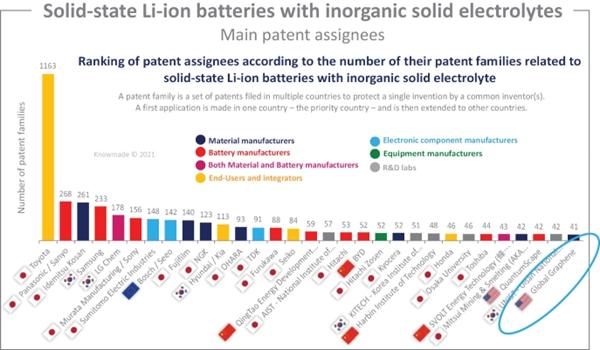

issues commonly associated with liquid electrolytes. KnowMade has analyzed more than 14,400 patent filings related to “solid-state

Li-ion batteries with inorganic solid electrolytes.” Solidion battery IP is one of only two U.S. companies recognized in its

list of the top 31 companies (Fig. 5).

Fig. 5 Solidion is recognized as a leader in solid-state

battery technologies.

Another KnowMade report (Fig. 6) has identified

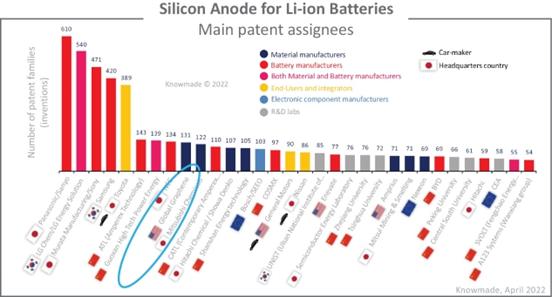

Solidion as the U.S. leader in the Si anode technology. In the USA, Solidion is No. 1 (having 131 patent families in the

Si anode), followed by GM (90), Enevate (77), and Amprius (71). Further, Honeycomb/G3 is ranked No. 9 in the entire battery industry,

after 8 major Li-ion battery cell producers; however, Solidion is No. 1 among all the battery start-ups in the world.

Fig. 6 Solidion is recognized as a leader in “Silicon

Anode for Li-ion Batteries.”

Our high silicon-content anode provides a drop-in

solution to enhancing the energy density of a lithium-ion battery. We have the earliest and most significant IP on elastic polymer-protected

silicon particles, which is the most cost-effective silicon anode as identified by Tesla on its “Battery Day” in 2020. We

are uniquely positioned to commercialize high silicon content-based all-solid-state batteries. We believe a partnership with Honeycomb

will help solidify an EV maker’s success as the worldwide leader in safe EVs for decades to come.

We are recognized as one of the Global Top 100

Innovators (Fig. 7), a testimony to not only the quantity but also the quality of our IP. In April 2022, LexisNexis published

“Innovation Momentum 2022: The Global Top 100,” a comprehensive IP report that recognized global technology companies with

exceptional technological relevance for the future, market coverage, and citation index. We were one of 12 companies recognized in the

report under the Chemicals and Materials industry sector, and one of only 2 such US-based companies that received the honor. Other innovators

listed in this sector are prominent EV battery companies such as LG Chem, Samsung SDI, and CATL. We are the only battery start-up listed

among these top 100 innovators.

Fig. 7 Third party validation of Solidion’s

IP quality

The strong IP portfolio enables Solidion to become a market and technology

leader in the battery space for decades to come.

Competition

We compete directly and indirectly with current

battery manufacturers and with an increasing number of companies that are developing new battery technologies and chemistries to address

the growing market for electrified mobility solutions. The EV battery industry is fast-growing and highly competitive. We primarily compete

with other silicon anode materials start-ups, such as Sila Nanotechnologies, Amprius Technologies and Group 14, which are all highly

promising battery companies.

Our competitors produce silicon anode materials

via CVD, which is believed to be expensive and challenging to scale up, and require explosive gaseous raw materials. In contrast, our

patented technologies are expected to allow us to produce highly scalable low-cost silicon-rich products that could be compatible with

solid-state and liquid-state electrolytes and have greater energy density and lower cost per kilowatt hour. Additionally, Solidion may

be perceived to compete with certain other solid-state or lithium metal battery start-ups, such as QuantumScape, Solid Power and SES. However,

we view these companies as potential strategic partners, not competitors. For instance, Solidion has complementary IPs that can help

each of these companies accelerate the commercialization of their lithium metal batteries (for example, by providing graphene/elastomer-protected

Li metal anode technologies). Our lithium metal protection technologies are capable of addressing certain known issues associated with

rigid inorganic solid electrolytes, such as large electrode/electrode interfacial impedance and the typically high stack-holding pressure.

Solidion’s solid state batteries are expected

to be produced at scale and cost-effectively using current lithium-ion cell production process and equipment, thus enabling fast time-to-market

compared to all-solid-state batteries. This versatile platform technology could potentially transform the lithium-ion battery industry

into producers of safe, solid-state batteries for EV, ESS, consumer electronics, and other power storage applications.

The following two charts summarize the key attributes

that differentiate Solidion’s products and technologies from certain of our competitors (Fig. 8 and Fig. 9):

Fig. 8 A brief summary of Solidion’s product/technology

attributes vs. other key silicon anode-focused battery start-ups.

Fig. 9 A brief summary of Solidion’s product/technology

attributes vs. other key lithium metal cell-focused battery start-ups.

Human Capital

We believe that our success is driven by our

team of technology innovators and experienced business leaders. We seek to hire and develop employees who are dedicated to our strategic

mission. As of March 2024, we employed 32 full time employees, 2 part time employees and 1 temporary employee.

We are committed to maintaining equitable compensation

programs including equity participation. We offer market-competitive salaries and strong equity compensation aimed at attracting and

retaining team members capable of making exceptional contributions to our success. Our compensation decisions are guided by the external

market, role criticality, and the contributions of each team member.

Facilities

Our corporate headquarters are located at 13355

Noel Rd., Suite 1100, Dallas, Texas, and our telephone number is (972) 918-5120.

Our Research and development and manufacturing

operations are located in Dayton, Ohio, where we own a building of approximately 27,646 square feet and lease a building of approximately

7,097 square feet.

Government Regulation and Compliance

There are government regulations pertaining to

battery safety, transportation of batteries, use of batteries in vehicles, factory safety and disposal of hazardous materials. We will

ultimately have to comply with these regulations to sell our battery products into market.

For example, we expect to become subject to federal

and state environmental laws and regulations regarding the handling and disposal of hazardous substances and solid waste, to include

electronic waste and battery cells. These laws regulate the generation, storage, treatment, transportation, and disposal of solid and

hazardous waste and may impose strict, joint and several liability for the investigation and remediation of areas where hazardous substances

may have been released or disposed. In the course of ordinary operations, we, through third parties and contractors, might in the future

handle hazardous substances within the meaning of the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”)

and similar state statutes and, as a result, may be jointly and severally liable for all or part of the costs required to clean up sites

at which these hazardous substances have been released into the environment. We might also become subject to the strict requirements

of the Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes for the generation or disposal of solid

waste, which may include hazardous waste.

Solidion expects to use existing factories to

produce solid-state batteries. The Occupational Safety and Health Act (“OSHA”), and comparable laws in other jurisdictions,

regulate the protection of the health and safety of workers in such factories. In addition, the OSHA hazard communication standard requires

that information be maintained about any hazardous materials used or produced in operations and that this information be provided to

employees, state and local government authorities, and the public.

The use, storage and disposal of battery packs

is regulated under federal law. We expect any batteries we produce will be required to conform to mandatory regulations governing the

transport of “dangerous goods” that may present a risk in transportation, which includes lithium-ion batteries, and are subject

to regulations issued by the Pipeline and Hazardous Materials Safety Administration (“PHMSA”). These regulations are based

on the UN Recommendations on the Safe Transport of Dangerous Goods Model Regulations and related UN Manual Tests and Criteria. The regulations

vary by mode of transportation when these items are shipped, such as by ocean vessel, rail, truck or air.

We expect that the EVs that would use our battery

technology would be subject to numerous regulatory requirements established by the National Highway Traffic Safety Administration (“NHTSA”),

including applicable U.S. federal motor vehicle safety standards (“FMVSS”). EV manufacturers must self-certify that the vehicles

meet or are exempt from all applicable FMVSSs before a vehicle can be imported into or sold in the U.S. There are numerous FMVSSs that

we expect would apply to vehicles that would use our battery technology. Examples of these requirements include:

| ● | Electric Vehicle

Safety — limitations on electrolyte spillage, battery retention and avoidance of electric

shock following specified crash tests; |

| ● | Crash Tests for

High-Voltage System Integrity — preventing electric shock from high voltage systems

and fires that result from fuel spillage during and after motor vehicle crashes. |

These standards and regulations cover various

aspects of battery safety, including electrical safety, mechanical safety, thermal safety, and environmental safety. They are developed

by organizations such as the Society of Automotive Engineers (also known as SAE), Underwriters Laboratories (“UL”), and regulatory

bodies such as NHTSA to ensure that batteries used in EVs meet specific safety requirements before being installed in a vehicle. There

are significant similarities among these standards; different EV makers require the battery suppliers to follow different standards.

We will work with UL and select EV makers to determine the required tests and to obtain the necessary safety certifications.

The United States Advanced Battery Consortium

(also known as USABC) provides the Battery Abuse Testing Manual for Electric and Hybrid Vehicle Applications, which defines abuse tests

for rechargeable energy storage systems (“RESSs”) used in electric vehicle applications. These tests evaluate the response

of RESS technologies to conditions or events that are outside of normal use. The manual recommends tests such as controlled crush, penetration,

thermal ramp, overcharge, and external short circuit tests across the cell, module, and pack levels (except for thermal ramp testing

at the pack level due to practical limitations). We plan to conduct internal safety tests at the cell levels, including nail penetration,

overcharging, and over-discharging at elevated temperatures, during the final research and development and prototyping stages. For the

remaining safety tests at the cell level, we will rely on third parties, such as UL, for safety certification purposes. We will also

collaborate with EV manufacturers to perform safety tests at the module and pack levels.

The timeline for conducting safety tests on batteries

for EVs will vary depending on factors such as the battery type, required testing standards, and the availability of testing facilities.

Typically, it takes several weeks to months to complete all the necessary safety tests at each level. Additionally, if any issues or

failures are identified during the testing process, additional time may be required to address these issues and retest the battery.

For more information, see “Risk Factors

— Risks Related to Legal and Regulatory Compliance” discussing regulations and regulatory risks related to product liability,

tax, employment, export controls, trade, data collection, privacy, environmental, health and safety, anti-corruption and anti-bribery

compliance.”

Legal Proceedings

There is no material litigation, arbitration

or governmental proceeding currently pending against us or any members of our management team in their capacity as such.

ITEM 1A. RISK FACTORS

Investing in our securities involves a high

degree of risk. Before making an investment decision, you should carefully consider the risks and uncertainties described below, together

with all of the other information in this Annual Report on Form 10-K, including the section titled “Management’s Discussion

and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto

included elsewhere in this Annual Report on Form 10-K. Our business, financial condition, results of operations or prospects could also

be harmed by risks and uncertainties not currently known to us or that we currently do not believe are material. If any of the risks

actually occur, our business, financial condition, results of operations and prospects could be adversely affected. In that event, the

market price of our securities could decline, and you could lose part or all of your investment.

Risks Related to Solidion’s Business and Operations

Risks Related to Development and Commercialization

If our batteries fail to perform as expected,

our ability to develop, market and sell our batteries would be adversely affected.

Our batteries may contain defects in design and

manufacture that may cause them to not perform as expected or that may require repairs, recalls and design changes. Our batteries are

inherently complex and incorporate technology and components that have not been used for certain applications and that may contain defects

and errors, particularly when first introduced to such applications. Although our batteries undergo quality control testing prior to

release for shipment, there can be no assurance that we will be able to detect and fix all defects prior to shipment, and nonconformances,

defects or errors could occur or be present in batteries that we release for shipment to customers. If our batteries fail to perform

as expected, our customers may delay deliveries, our customer may terminate orders or we may initiate product recalls, each of which

could adversely affect our sales and brand and could adversely affect our business, financial condition, prospects and results of operations.

Our battery architecture is different from our

peers’ and may behave differently in customer use applications, certain applications of which we have not yet evaluated. This could

limit our ability to deliver to certain applications. In addition, our historical data on the performance and reliability of our batteries

is limited, and therefore our batteries could fail unexpectedly in the field resulting in significant warranty costs or brand damage

in the market. Further, the structure of our battery is different from traditional lithium-ion batteries and therefore our batteries

could be susceptible to different and unknown failure modes leading our batteries to fail and cause a safety event in the field. Such

an event could result in the failure of our end customers’ product as well as the loss of life or property, resulting in severe

financial penalties for us, including the loss of revenue, cancelation of supply contracts and the inability to win new business due

to reputational damage in the market. In addition, consistent with industry norms, we would anticipate that when we enter into agreements

to supply our battery products to end product manufacturers, that the terms of these agreements may require us to bear certain costs

relating to recalls and replacements of end products when such recalls and replacements are due to defects of our battery products that

are incorporated in such end products.

OEMs may elect to pursue other battery

cell technologies, which likely would impair our revenue generating ability.

OEMs are motivated to develop and commercialize

improved battery cell technologies. To that end, OEMs partners have invested, and are likely to continue to invest in the future, in

their own development efforts and, in certain cases, in joint development agreements with our current and future competitors. If other

technology is developed more rapidly than our high-capacity anode and high-energy solid-state battery technology, or if such competing

technologies are determined to be more efficient or effective than our high-capacity anode and high-energy solid-state battery technology,

our partners may elect to adopt and install a competitor’s technology or products over ours, which could materially impact our

business, financial results, and prospects.

We have only conducted preliminary safety

testing on our high-capacity anode and high-energy solid-state battery technology, and our technology will require additional and extensive

safety testing prior to being installed in electric vehicles.

To achieve acceptance by automotive OEMs, our

anticipated commercial-sized our high-capacity anode and high-energy solid-state battery technology will have to undergo

extensive safety testing. We cannot assure you such tests will be successful, and we may identify different or new safety issues in our

development or the commercial cells that have not been present in our prototype cells. If we have to make design changes to address any

safety issues, we may have to delay or suspend commercialization, which could materially damage our business, prospects, financial condition,

operating results and brand.

We rely on complex equipment for our operations,

and production involves a significant degree of risk and uncertainty in terms of operational performance and costs.

We rely heavily on complex equipment for our

operations and the production of our high-capacity anode and high-energy solid-state battery technology. The work required to integrate

this equipment into the production of our high-capacity anode and high-energy solid-state battery technology is time intensive and

requires us to work closely with the equipment providers to ensure that it works properly with our proprietary technology. This integration

involves a degree of uncertainty and risk and may result in the delay in the scaling up of production or result in additional cost to

our high-capacity anode and high-energy solid-state battery technology.

Our current manufacturing facilities require,

and we expect our future manufacturing facilities will require, large-scale machinery and equipment. Such machinery and equipment may

unexpectedly malfunction and require repairs and spare parts to resume operations, which may not be available when needed. In addition,

because this equipment has historically not been used to build our high-capacity anode and high-energy solid-state batteries,

the operational performance and costs associated with this equipment is difficult to predict and may be influenced by factors outside

of our control, such as, but not limited to, failures by suppliers to deliver necessary components of our products in a timely manner

and at prices and volumes acceptable to us, environmental hazards and associated costs of remediation, difficulty or delays in obtaining

governmental permits, damages or defects in systems, industrial accidents, fires, seismic activity and other natural disasters.

Problems with our manufacturing equipment could

result in the personal injury to or death of workers, the loss of production equipment, damage to manufacturing facilities, monetary

losses, delays and unanticipated fluctuations in production. In addition, in some cases operational problems may result in environmental

damage, administrative fines, increased insurance costs and potential legal liabilities. Any of these operational problems, or a combination

of them could have a material adverse effect on our business, results of operations, cash flows, financial condition or prospects.

We may obtain licenses on technology that

has not been commercialized or has been commercialized only to a limited extent, and the success of our business may be adversely affected

if such technology does not perform as expected.

From time to time, we may license from third

parties technologies that have not been commercialized or which have been commercialized only to a limited extent. These technologies

may not perform as expected within our high-capacity anode and high-energy solid-state batteries and related products. If the cost,

performance characteristics, manufacturing process or other specifications of these licensed technologies fall short of our targets,

our projected sales, costs, time to market, competitive advantage, future product pricing and potential operating margins may be adversely

affected.

Substantial increases in the prices for

our raw materials and components, some of which are obtained from a limited number of sources where demand may exceed supply, could materially

and adversely affect our business.

We rely on third-party suppliers for components

and equipment necessary to develop our high-capacity anode and high-energy solid-state battery technology. We face risks relating

to the availability of these materials and components, including that we will be subject to demand shortages and supply chain challenges

and generally may not have sufficient purchasing power to eliminate the risk of price increases for the raw materials and tools we need.

To the extent that we are unable to enter into commercial agreements with our current suppliers or our replacement suppliers on favorable

terms, or these suppliers experience difficulties meeting our requirements, the development and commercial progression of our high-capacity

anode and high-energy solid-state battery technology and related technologies may be delayed.

Separately, we may become subject to various

supply chain requirements regarding, among other things, conflict minerals and labor practices. We may be required to incur substantial

costs to comply with these requirements, which may include locating new suppliers if certain issues are discovered. We may not be able

to find any new suppliers for certain raw materials or components required for our operations, or such suppliers may be unwilling or

unable to provide us with products.

Any disruption in the supply of components, equipment

or materials could temporarily disrupt research and development activities or production of our high-capacity anode and high-energy

solid-state battery technology until an alternative supplier is able to supply the required material. Changes in business conditions,

unforeseen circumstances, governmental changes, and other factors beyond our control or which we do not presently anticipate, could also

affect our suppliers’ ability to deliver components or equipment to us on a timely basis. Any of the foregoing could materially

and adversely affect our results of operations, financial condition and prospects.

Currency fluctuations, trade barriers, tariffs

or shortages and other general economic or political conditions may limit our ability to obtain key components or equipment for our high-capacity

anode and high-energy solid-state battery technology or significantly increase freight charges, raw material costs and other expenses

associated with our business, which could further materially and adversely affect our results of operations, financial condition and

prospects.

We may be unable to adequately control

the costs associated with our operations and the components necessary to build our high-capacity anode and high-energy solid-state batteries,