As filed electronically with the Securities

and Exchange Commission on November 4, 2024

Registration No. 333-281990

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM

N-14

REGISTRATION

STATEMENT

UNDER

THE SECURITIES ACT OF 1933

☒ Pre-Effective

Amendment No. 3 ☐ Post-Effective Amendment No. ___

TORTOISE ENERGY

INFRASTRUCTURE CORPORATION

(Exact Name of Registrant

as Specified in Charter)

6363 College Boulevard,

Suite 100A

Overland Park, Kansas 66211

(Address of Principal Executive

Offices) (Zip Code)

(913) 981-1020

(Registrant’s Area

Code and Telephone Number)

Matthew G.P. Sallee

Diane Bono

6363 College Boulevard,

Suite 100A

Overland Park, Kansas 66211

(Name and Address of Agent

for Service)

With copies to:

Deborah Bielicke Eades

Vedder Price P.C.

222 N. LaSalle Street

Chicago, Illinois 60601

Approximate date of proposed public offering: As soon as practicable

after the effective date of this Registration Statement.

The Registrant hereby amends this Registration Statement on such date

or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states

that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until

the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section

8(a), may determine.

important: your

vote is required

TORTOISE MIDSTREAM

ENERGY FUND, INC.

TORTOISE ENERGY

INFRASTRUCTURE CORPORATION

[●], 2024

Dear Fellow Stockholders:

I am writing to inform you

of, and ask for your vote on, a very important matter affecting your investment in Tortoise Midstream Energy Fund, Inc. (the “Target

Fund”) and/or Tortoise Energy Infrastructure Corporation (the “Acquiring Fund” and, together with the Target Fund,

the “Funds” or each, individually, a “Fund”), each a Maryland corporation. A joint special meeting of stockholders

of the Funds (the “Meeting”) will be held on November 25, 2024, at the offices of Tortoise Capital Advisors, L.L.C., 6363

College Boulevard, Suite 100A, Overland Park, Kansas 66211 at 10:00 a.m. central time. At the Meeting, stockholders will be asked

to vote on a proposal to:

| |

● |

(Stockholders of the Target Fund) approve the merger

of the Target Fund with and into a wholly-owned subsidiary of the Acquiring Fund organized as a Maryland limited liability company

(the “Merger”). |

| ● | (Stockholders of the Acquiring

Fund) approve the issuance of Acquiring Fund common stock in connection with the Merger. |

The Board of Directors of

each Fund has determined that the Merger is advisable and in the best interests of the applicable Fund and unanimously recommends that

you vote “FOR” your Fund’s proposal. Enclosed in this booklet are (i) a Notice of Joint Special Meeting of

Stockholders; and (ii) a Joint Proxy Statement and Prospectus providing detailed information on the Acquiring Fund, including a

comparison of the Target Fund to the Acquiring Fund, and the Merger, including the reasons for proposing the Merger.

The enclosed materials explain

the proposals to be voted on at the Meeting in more detail, and I encourage you to review them carefully. No matter how large or small

your holdings, your vote is extremely important. You may vote in person at the Meeting, or you may authorize a proxy to vote your

shares using one of the methods below or by following the instructions on your proxy card:

| ● | By touch-tone telephone, simply

dial the toll-free number located on the enclosed proxy card. Please be sure to have your

proxy card available at the time of the call; |

| ● | By internet, please log on

to the voting website detailed on the enclosed proxy card. Again, please have your proxy

card handy at the time you access the website; or |

| ● | By returning the enclosed

proxy card in the postage-paid envelope. |

If you should have any questions

about the Meeting agenda or voting, please call our proxy agent, EQ Fund Solutions, LLC, at (877) 732-3618. Please note, at a reasonable

time after the mailing has been completed and our records indicate that you have not voted at that time, you may be contacted by our

proxy agent to confirm receipt of the proxy material and review your voting options.

On behalf of the Funds and

your fellow stockholders, I thank you for your prompt vote on these important matters.

| |

Sincerely yours,

Matthew G.P. Sallee

Chief Executive Officer and President

Tortoise Midstream Energy Fund, Inc.

Tortoise Energy Infrastructure Corporation |

IMPORTANT INFORMATION FOR

STOCKHOLDERS OF

TORTOISE MIDSTREAM ENERGY FUND, INC.

AND

TORTOISE ENERGY INFRASTRUCTURE CORPORATION

Although we recommend that

you read the enclosed Joint Proxy Statement and Prospectus (“Joint Proxy Statement/Prospectus”) in its entirety, for your

convenience, we have provided a brief overview of the proposals to be voted on at the joint special meeting of stockholders of Tortoise

Midstream Energy Fund, Inc. (the “Target Fund”) and Tortoise Energy Infrastructure Corporation (the “Acquiring Fund”

and, together with the Target Fund, the “Funds” or each, individually, a “Fund”).

Questions Regarding the Merger

| Q. | Why am I receiving the enclosed

Joint Proxy Statement/Prospectus? |

A. You

are receiving the Joint Proxy Statement/Prospectus as a stockholder of the Target Fund and/or the Acquiring Fund at the close of business

on the record date. At the joint special meeting of stockholders of the Funds (the “Meeting”), stockholders of the Funds

will be asked to vote on the following proposals:

| |

· |

(Stockholders of the Target Fund) To approve the merger

of the Target Fund with and into a wholly-owned subsidiary (the “Merger Sub”) of the Acquiring Fund (the “Merger”). |

| · | (Stockholders

of the Acquiring Fund) To approve the issuance of Acquiring Fund common stock in connection

with the Merger (the “Share Issuance”). |

With respect to each Fund,

the presence in person or by proxy of holders of shares entitled to cast a majority (i.e., greater than 50%) of the votes entitled to

be cast (without regard to class) constitutes a quorum. When a quorum is present at the Meeting, the affirmative vote of a majority of

the votes entitled to be cast is required to approve the Merger and the affirmative vote of a majority of votes cast is required to approve

the Share Issuance. Common stockholders and preferred stockholders, voting as a class, are entitled to vote on the above matters. Each

stockholder is entitled to one vote for each share of common stock and/or preferred stock owned by such stockholder.

A Merger Sub is being used

to accomplish the Merger for tax and corporate purposes. As soon as practicable following the completion or termination of the Merger,

the Merger Sub will merge with and into the Acquiring Fund and the Acquiring Fund will be the surviving entity in the subsidiary merger.

On September 4, 2024, the Board of Directors of each Fund (the “Boards” and each, a “Board”) unanimously determined

that the Merger, with respect to its Fund, is advisable and in the best interests of the applicable Fund. The Board of each Fund recommends

that you vote FOR your Fund’s proposal.

| Q. | Why is the Merger being recommended

by each Board? |

A. Over

the past several years, the Boards of the Funds and Tortoise Capital Advisors, L.L.C. (the “Adviser”), the investment adviser

for the Funds, have periodically evaluated various strategic alternatives for the Funds to enhance stockholder value, including potential

mergers, tender offers, and other product restructurings, and have entered into unsuccessful negotiations with third parties regarding

a potential merger. During a series of meetings held in July, August and September 2024, the Adviser proposed, and the Boards of the

Funds considered the Merger. At those meetings, the Adviser discussed with the Fund Boards its reasons for proposing the Merger. The

Adviser stated that it had conducted a review of its investment product offerings and fund structures and evaluated strategic alternatives

for each of the Funds in light of certain factors, including, among others, discount levels of the trading price of the Funds’

shares compared to net asset value (“NAV”), the use and risks of leverage, the marketplace for closed-end funds (“CEFs”)

in the energy infrastructure sector, and continued focus by activist investors on the Funds. Following a review with the Adviser of strategic

alternatives for each Fund, each Board believes the Merger may benefit its Fund and its stockholders through (among other reasons) the

following:

| |

● |

The potential for higher common stock net earnings and distribution levels

following the Merger, due to operating economies from the combined fund’s scale; |

| |

● |

The potential for narrowing the discount to NAV at which the Funds’

shares have traded, as a result of the larger size of the combined fund and an increased level of distributions in the Acquiring

Fund after the Merger; |

| ● | Continuation of the Funds’ common investment objective

of seeking a high level of total return, emphasizing current distributions, and using the

same portfolio management team but implementing TYG’s broader investment focus within

the energy infrastructure sector; |

| ● | Continuation of the Funds’

CEF structure, where shares are not continuously offered and do not have daily redemptions

thereby avoiding the portfolio trading costs associated with managing flows in and out of

the Fund, and allowing for use of structural leverage (provided by preferred stock and indebtedness)

to potentially increase investment returns; |

| ● | The potential for greater secondary market liquidity and

improved secondary market trading for common stock as a result of the combined fund’s

greater share volume; and |

| |

● |

Lower net overall fees and expenses and total fund operating expenses (excluding

leverage and tax expense), in each case as a percentage of net assets of the combined fund. See “Proposal 1: Authorization

of the Merger— D. Additional Information About the Investment Policies of the Acquiring Fund and Management of the Funds—Compensation

and Expenses” in the Joint Proxy Statement/Prospectus at page 52 for further discussion regarding fund fees. |

Based

on the foregoing and as further described in the Joint Proxy Statement/Prospectus, each Board,

including the Directors who are not "interested persons," as defined in the Investment

Company Act of 1940, as amended (the "1940 Act"), of the Funds, unanimously approved

the Merger and determined that the Merger would be in the overall best interests of the Fund

and not dilutive to the interests of the stockholders thereof. Accordingly, the Target Fund

Board recommends that stockholders of the Target Fund approve the Merger and the Acquiring

Fund Board recommends that Acquiring Fund stockholders approve the Share Issuance. See “Proposal

1: Authorization of the Merger— C. Information About the Merger—Background and

Board Considerations Relating to the Proposed Merger” in the Joint Proxy Statement/Prospectus

at page 25 for additional information about each Board’s considerations relating to

the Merger.

| |

Q. |

How do the investment objectives, principal investments,

risks and portfolio management teams of the Funds compare? |

A. Each

Fund’s investment objective is to seek a high level of total return with an emphasis

on current distributions paid to stockholders. The Acquiring Fund primarily invests in equity

securities of energy infrastructure companies while the Target Fund primarily invests in

midstream energy entities in the energy infrastructure sector with an emphasis on natural

gas infrastructure entities. Under normal circumstances, the Acquiring Fund invests at least

90% of its total investments in securities of energy infrastructure companies. Under normal

circumstances, the Target Fund invests at least 80% of its total investments in equity securities

of midstream energy entities in the energy infrastructure sector, including master limited

partnerships (“MLPs”), with at least 50% of its total investments in equity securities

of natural gas infrastructure entities. In light of the foregoing, the Funds are subject

to similar, but not identical, risks. See “Proposal 1: Authorization of the Merger—

B. Risk Factors—Principal Risks Comparison” in the Joint Proxy Statement/Prospectus

at page 11, which includes a comparison of the principal risks associated with an investment

in each Fund. The Acquiring Fund has the same investment adviser and portfolio management

team as the Target Fund.

| Q. | Will the portfolios be repositioned

before the Merger? |

A. Yes,

prior to the Merger, the Target Fund expects to sell approximately 26% of its portfolio to

align its portfolio with the portfolio of the Acquiring Fund by deemphasizing natural gas

infrastructure holdings. These expenses will be borne by the Target Fund and its common stockholders,

and the Target Fund may realize capital gains and possibly ordinary income from such sales.

As of September 3, 2024, the Target Fund is estimated to realize capital gains of approximately

$1,600,000 (or $0.31 per share from such sales in advance of the Merger). It is anticipated

that such gains will be entirely offset by capital loss carryforwards. Actual market prices,

costs and capital gains or losses experienced by the Target Fund will depend on market conditions

at the time of the portfolio repositioning. As of November 30, 2023, the Target Fund and

the Acquiring Fund had short-term capital loss carryforwards of $461,393,378 and $259,460,371,

respectively.

| Q. | How will the Merger affect

stockholders of the Funds? |

A. If

the Merger is approved, upon the closing of the Merger, each common stockholder of the Target

Fund will become a common stockholder of the Acquiring Fund and thereafter cease to be a

common stockholder of the Target Fund. Each common stockholder of the Target Fund will receive

a number of shares of common stock of the Acquiring Fund (which number may not be equal to

the number of shares of Target Fund common stock held by such stockholder) representing an

aggregate net asset value equal to the aggregate net asset value of the share of Target Fund

common stock held by such stockholder immediately prior to the Merger (with cash being distributed

in lieu of fractional shares of the Acquiring Fund). Preferred stockholders of the Target

Fund will receive on a one-for-one basis newly issued preferred shares of the Acquiring Fund

having substantially the same terms as their Target Fund preferred shares as in effect immediately

before the Merger. The Target Fund will be merged with and into a wholly-owned subsidiary

of the Acquiring Fund, the assets and liabilities of the Target Fund will be combined with

the assets and liabilities of the wholly-owned subsidiary of the Acquiring Fund and the Target

Fund will cease its separate existence under Maryland law.

| Q. | Will common stockholders of

the Funds have to pay any fees in connection with the Merger? |

A. Yes.

Each Fund, and therefore its common stockholders, will bear the costs of the Merger whether

or not the Merger is consummated. Preferred stockholders will not bear any costs of the Merger.

Costs attributable to a particular Fund will be expensed to such Fund, while non-specific

costs will be allocated on a pro rata basis based upon each Fund’s net assets. Such

one-time expenses, which include legal and audit fees, filing fees, and printing and mailing

costs, are expected to be approximately $669,002, which equates to $427,139 or $0.04 per

share for the Acquiring Fund and $241,863 or $0.05 per share for the Target Fund as of May 31,

2024. Following the Merger, common stockholders of the Funds are expected to benefit from

reduced ongoing fees and expenses. Each Fund has engaged EQ Fund Solutions, LLC to assist

in the solicitation of proxies at an estimated cost of $287,319 plus reasonable expenses,

which is included in the expense estimate above.

| Q. | Is the Merger expected to

be a taxable event for Target Fund stockholders? |

A. The

Merger is intended to qualify as a “reorganization” for federal income tax purposes. Provided the Merger qualifies as a reorganization

for federal income tax purposes, each Target Fund stockholder generally will not recognize any gain or loss, except with respect to cash

received in lieu of a fractional share of Acquiring Fund common stock. The federal income tax consequences of the Merger to each Target

Fund stockholder will depend on such Target Fund stockholder’s own situation and many variables. You should consult with your tax

advisor for the specific tax consequences to you of the Merger. See “Proposal 1: Authorization of the Merger— C. Information

About the Merger—Federal Income Tax Consequences of the Merger” in the Joint Proxy Statement/Prospectus at page 38.

General Questions

| Q. | How does the Board of my Fund

suggest that I vote? |

A. After

careful consideration, the Board of each Fund recommends that you vote “FOR” the proposal for your Fund.

| Q. | How do I vote my shares? |

A. You may

vote in person at the Meeting, or you may authorize a proxy to vote your shares using one of the methods below or by following the instructions

on your proxy card:

| ● | By touch-tone telephone, simply

dial the toll-free number located on the enclosed proxy card. Please be sure to have your

proxy card available at the time of the call; |

| ● | By internet, please log on

to the voting website detailed on the enclosed proxy card. Again, please have your proxy

card handy at the time you access the website; or |

| ● | By returning the enclosed

proxy card in the postage-paid envelope |

Please note, however, that if your shares are

held of record by a broker, bank or other nominee and you wish to vote at the Meeting, you must obtain from the record holder a legal

proxy issued in your name. However, even if you plan to attend the Meeting, we urge you to authorize a proxy to vote your shares in advance

of the Meeting. That will ensure that your vote is counted should your plans change.

| Q. | Whom do I contact for further

information? |

A. You

may contact Investor Relations toll-free at (866) 362-9331 for further information.

| Q. | Will anyone contact me? |

A. You

may receive a call from EQ Fund Solutions, LLC, the proxy solicitor hired by your Fund, to verify that you received your proxy materials,

to answer any questions you may have about the proposals and to encourage you to authorize your proxy. We recognize the inconvenience

of the proxy solicitation process and would not impose it on you if we did not believe that the matters being proposed were important.

Once your vote has been registered with the proxy solicitor, your name will be removed from the solicitor’s follow-up contact list.

| Q. | When will the proposed Merger

be completed? |

A. If

the Merger is approved by Target Fund stockholders, the Share Issuance is approved by Acquiring Fund stockholders and the conditions

to closing are satisfied (or otherwise waived), the Merger is expected to occur in the fourth quarter of 2024.

| Q. | What will happen if the required

stockholder approval is not obtained? |

A. If

the required stockholder approval is not obtained and, as a result, the Merger is not consummated, the Board of the Target Fund and Board

of the Acquiring Fund may take such actions as they deem in the best interests of the applicable Fund, including conducting additional

solicitations with respect to the proposals or continuing to operate each of the Target Fund and Acquiring Fund as a standalone fund.

Your vote is very important.

We encourage you as a stockholder to participate in your Fund’s governance by authorizing a proxy to vote your shares as soon as

possible. If enough stockholders fail to cast their votes, your Fund may not be able to hold its meeting or the vote and will be required

to incur additional solicitation costs to obtain sufficient stockholder participation.

TORTOISE MIDSTREAM ENERGY FUND, INC.

TORTOISE ENERGY INFRASTRUCTURE CORPORATION

6363 College Boulevard, Suite 100A

Overland Park, Kansas 66211

NOTICE OF JOINT special

meeting OF STOCKHOLDERS

TO BE HELD ON NOVEMBER 25, 2024

Notice is hereby given that

a joint special meeting of stockholders (the “Meeting”) of Tortoise Midstream Energy Fund, Inc. (the “Target Fund”)

and Tortoise Energy Infrastructure Corporation (the “Acquiring Fund”), each a Maryland corporation, will be held at 6363

College Boulevard, Suite 100A, Overland Park, Kansas 66211 on November 25, 2024 at 10:00 a.m. central time for the following purposes,

each as more fully described in the Joint Proxy Statement/Prospectus:

| |

· |

(Stockholders of the Target Fund) To consider and

vote upon the merger of the Target Fund with and into a wholly-owned subsidiary (the Merger Sub) of the Acquiring Fund. |

| · | (Stockholders

of the Acquiring Fund) To consider and vote upon the issuance of Acquiring Fund common stock

in connection with the merger of the Target Fund with and into a wholly-owned subsidiary

of the Acquiring Fund. |

Stockholders

of record as of the close of business on September 9, 2024 are entitled to notice of, and

to vote at, the Meeting or any adjournment or postponement thereof.

Common

stockholders and preferred stockholders voting as a class, are entitled to vote on the above

matters. Each stockholder is entitled to one vote for each share of common stock and/or preferred

stock owned by such stockholder.

A

Merger Sub is being used to accomplish the Merger for tax and corporate purposes. As soon

as practicable following the completion or termination of the Merger, the Merger Sub will

merge with and into the Acquiring Fund and the Acquiring Fund will be the surviving entity

in such merger. The Board of Directors of the Acquiring Fund and the Target Fund each

unanimously recommends stockholders vote “FOR” the proposal involving their Fund.

Whether or not you expect

to attend the Meeting, please authorize a proxy to vote your shares of stock by following the detailed instructions provided on your

proxy or voting instruction card.

IN ORDER TO AVOID THE ADDITIONAL EXPENSE OF

FURTHER SOLICITATION, THE BOARDS OF DIRECTORS ASK THAT YOU VOTE PROMPTLY, NO MATTER HOW MANY SHARES OF STOCK YOU OWN.

|

For the Boards of Directors,

Diane M. Bono

Secretary

Tortoise Midstream Energy Fund, Inc.

Tortoise Energy Infrastructure Corporation

[●], 2024 |

The information contained in this

Joint Proxy Statement/Prospectus is not complete and may be changed. We may not sell these securities until the registration statement

filed with the Securities and Exchange Commission is effective. This Joint Proxy Statement/Prospectus is not an offer to sell these securities,

and it is not soliciting an offer to buy these securities, in any jurisdiction where the offer or sale is not permitted.

SUBJECT

TO COMPLETION, DATED November 4, 2024

JOINT PROXY STATEMENT/PROSPECTUS

TORTOISE MIDSTREAM ENERGY FUND, INC.

TORTOISE ENERGY INFRASTRUCTURE CORPORATION

6363 College Boulevard, Suite 100A

Overland Park, Kansas 66211

(913) 981-1020

JOINT SPECIAL MEETING OF STOCKHOLDERS

[●], 2024

This Joint Proxy Statement/Prospectus

is furnished to you as a stockholder of Tortoise Energy Infrastructure Corporation (“TYG” or the “Acquiring Fund”)

and/or Tortoise Midstream Energy Fund, Inc. (“NTG” or the “Target Fund”), each a Maryland corporation registered

as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940

Act”). A joint special meeting of stockholders of the Acquiring Fund and the Target Fund (the “Meeting”) will be held

at 6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211 on November 25, 2024, at 10:00 a.m. central time, to consider

and vote on the items listed below and discussed in greater detail elsewhere in this Joint Proxy Statement/Prospectus. The Acquiring

Fund and the Target Fund are each sometimes referred to herein as a “Fund” and are sometimes referred to herein collectively

as the “Funds.” The Acquiring Fund following the Merger is sometimes referred to herein as the “Combined Fund.”

Stockholders of the Target

Fund will be asked to approve the merger (the “Merger”) of the Target Fund with and into a wholly-owned subsidiary of the

Acquiring Fund (the “Merger Sub”). Stockholders of the Acquiring Fund will be asked to consider and vote upon the issuance

of Acquiring Fund common stock in connection with the Merger (the “Share Issuance”).

Common

stockholders and preferred stockholders voting as a class, are entitled to vote on the above

matters. Each stockholder is entitled to one vote for each share of common stock and/or preferred

stock owned by such stockholder.

Even if you plan to attend

the Meeting, the Board of Directors of each of the Acquiring Fund and the Target Fund (the "Boards"" and each, a "Board")

requests that you authorize a proxy to vote your shares of stock as described in the enclosed proxy or voting instruction card so that

your vote will be counted if you later decide not to attend the Meeting. The approximate mailing date of this Joint Proxy Statement/Prospectus

and accompanying form of proxy is [●], 2024.

The

enclosed proxy cards and this Joint Proxy Statement/Prospectus are first being sent to stockholders

of the Funds on or about [●], 2024. Stockholders of record as of the close of business

on September 9, 2024 are entitled to notice of and to vote at the Meeting and any adjournments

or postponements.

The Board of Directors of

each Fund has determined that including these proposals in one Joint Proxy Statement/Prospectus will reduce costs and is advisable and

in the best interests of each Fund.

ADDITIONAL INFORMATION

The Board of Directors of

each Fund has unanimously determined that the Merger is advisable and in the best interests of the Fund, and the Board of Directors

of each Fund unanimously recommends that you vote FOR the proposal for your Fund.

This Joint Proxy Statement/Prospectus

explains concisely what you should know before voting on the Merger or investing in the Acquiring Fund. Please read it carefully and

keep it for future reference.

The

enclosed proxy cards and this Joint Proxy Statement/Prospectus are first being sent to stockholders

of the Funds on or about [●], 2024. Stockholders of record as of the close of business

on September 9, 2024 are entitled to notice of and to vote at the Meeting and any adjournments

or postponements.

The securities offered

by this Joint Proxy Statement/Prospectus have not been approved or disapproved by the Securities and Exchange Commission (the “SEC”),

nor has the SEC passed upon the accuracy or adequacy of this Joint Proxy Statement/Prospectus. Any representation to the contrary is

a criminal offense.

The Acquiring Fund will continue

to list and trade its shares on the New York Stock Exchange (the “NYSE”).

The below documents have

been filed with the SEC and contain additional information about the Funds and are incorporated by reference into (and legally considered

to be a part of) this Joint Proxy Statement/Prospectus:

| (i) | the Statement of Additional Information

(“SAI”) to this Joint Proxy Statement/Prospectus, dated [●], 2024; |

No other parts of the Funds’

Annual and Semi-Annual Reports to stockholders are incorporated by reference herein.

The foregoing documents can

be obtained on a web site maintained by the Funds’ investment adviser, Tortoise Capital Advisors, L.L.C. (the “Adviser”)

at www.tortoiseadvisors.com or each Fund will furnish, without charge, a copy of any such document to any stockholder upon request. Any

such request should be directed to the Adviser by calling 866-362-9331 or by writing to the respective Fund at its principal executive

offices at 6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211. The telephone number of the principal executive offices of

the Funds is 913-981-1020.

The Funds are subject to

the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended

(the “1940 Act”), and in accordance therewith are required to file reports and other information with the SEC. These reports,

proxy statements, registration statements and other information can be inspected and copied, after paying a duplicating fee, by electronic

request at publicinfo@sec.gov. In addition, copies of these documents may be viewed online or downloaded without charge from the SEC’s

website at www.sec.gov. Reports, proxy materials and other information concerning each Fund may be inspected at the offices of the NYSE,

11 Wall St., New York, NY 10005.

This Joint Proxy Statement/Prospectus

serves as a prospectus for the Acquiring Fund in connection with the Share Issuance. In this connection, no person has been authorized

to give any information or make any representation not contained in this Joint Proxy Statement/Prospectus and, if so given or made, such

information or representation must not be relied upon as having been authorized. This Joint Proxy Statement/Prospectus does not constitute

an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful

to make such offer or solicitation.

Table of Contents

PROPOSAL

1: AUTHORIZATION OF THE MERGER

a.

Synopsis

The following is a summary

of certain information contained elsewhere in this Joint Proxy Statement/Prospectus and is qualified in its entirety by reference to

the more complete information contained in this Joint Proxy Statement/Prospectus and in the Merger Statement of Additional Information.

Stockholders should read this entire Joint Proxy Statement/Prospectus carefully.

The Proposed Merger

If stockholders of the Target

Fund approve the Merger, the stockholders of the Acquiring Fund approve the Share Issuance, and the Merger is completed, each Target

Fund stockholder will receive a number of shares of common stock of the Acquiring Fund representing an aggregate net asset value equal

to the aggregate net asset value of the shares of Target Fund common stock held by such stockholder immediately prior to the closing

of the Merger (with cash being distributed in lieu of fractional shares of Acquiring Fund common stock), and, as such, each such Target

Fund stockholder will become a common stockholder of the Acquiring Fund and cease to be a stockholder of the Target Fund. The Merger

Sub is being formed for tax and corporate purposes solely to accomplish the Merger and will be merged with and into the Acquiring Fund

as soon as practicable following the Merger. Shares of common stock of the Target Fund would be exchanged for shares of common stock

of the Acquiring Fund on a tax-free basis for federal income tax purposes (although Target Fund stockholders who receive cash for their

fractional shares may incur certain tax liabilities). Notwithstanding the foregoing, the Merger involves additional tax implications

that could significantly impact the Funds and their stockholders. See “Proposal 1: Authorization of the Merger— C. Information

About the Merger—Federal Income Tax Consequences of the Merger” at page 38 for a further discussion of such tax implications.

The Acquiring Fund will issue to Target Fund stockholders book-entry interests for the shares of the Acquiring Fund registered in a “street

name” brokerage account held for the benefit of such stockholders. Like shares of common stock of the Target Fund, shares of

common stock of the Acquiring Fund are not deposits or obligations of, or guaranteed or endorsed by, any financial institution, are not

insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and involve risk, including the

possible loss of the principal amount invested.

The Merger Sub shall be the

surviving entity in the Merger. As soon as practicable following the completion or termination of the Merger, the Merger Sub will merge

with and into the Acquiring Fund and the Acquiring Fund will be the surviving entity in the subsidiary merger.

As a result of the Merger,

each series of Mandatory Redeemable Preferred Shares of the Target Fund that is outstanding as of the closing of the Merger (“Target

Fund MRP Shares”) will convert into a series of newly-issued Mandatory Redeemable Preferred Shares of the Acquiring Fund (“New

Acquiring Fund MRP Shares”) having substantially the same terms as such series of the Target Fund MRP Shares immediately prior

to the Merger. The aggregate liquidation preference of the New Acquiring Fund MRP Shares received by holders of Target Fund MRP Shares

in the Merger will equal the aggregate liquidation preference of the Target Fund MRP Shares of the applicable series held by such holders

immediately prior to the closing of the Merger. The New Acquiring Fund MRP Shares to be issued in the Merger will have equal priority

with the Acquiring Fund’s existing outstanding preferred stock as to the payment of dividends and the distribution of assets in

the event of the Acquiring Fund’s liquidation. In addition, the preferred stock of the Acquiring Fund, including the New Acquiring

Fund MRP Shares to be issued in connection with the Merger, will be senior in priority to the Acquiring Fund common stock as to payment

of dividends and the distribution of assets in the event of the Acquiring Fund’s liquidation.

Prior to the Merger, the

Target Fund expects to sell approximately 26% of its portfolio to align its portfolio with the portfolio of the Acquiring Fund by deemphasizing

natural gas infrastructure holdings. These expenses will be borne by the Target Fund and its common stockholders, and the Target Fund

may realize capital gains and possibly ordinary income from such sales. As of September 3, 2024, the Target Fund is estimated to realize

capital gains of approximately $1,600,000 (or $0.31 per share from such sales in advance of the Merger). It is anticipated that such

gains will be entirely offset by capital loss carryforwards. Actual market prices, costs and capital gains or losses experienced by the

Target Fund will depend on market conditions at the time of the portfolio repositioning. As of November 30, 2023, the Target Fund and

the Acquiring Fund had short-term capital loss carryforwards of $461,393,378 and $259,460,371, respectively.

If the Merger is not approved

by stockholders of the Target Fund, or if the Share Issuance is not approved by stockholders of the Acquiring Fund, the Board of the

Target Fund and the Board of the Acquiring Fund may take such action as they deem in the best interests of the applicable Fund, including

conducting additional solicitations or continuing to operate each of the Target Fund and Acquiring Fund as a standalone Maryland corporation

advised by the Adviser.

Background and Reasons

for the Proposed Merger

Over the past several years, the Boards of the

Funds and the Adviser have periodically evaluated various strategic alternatives for the Funds to enhance stockholder value, including

potential mergers, tender offers, and other product restructurings, and have entered into unsuccessful negotiations with third parties

regarding a potential merger. During a series of meetings held in July, August and September 2024, the Adviser proposed, and the Boards

of the Funds considered the Merger. At those meetings, the Adviser discussed with the Fund Boards its reasons for proposing the Merger.

The Adviser stated that it had conducted a review of its investment product offerings and fund structures and evaluated strategic alternatives

for each of the Funds in light of certain factors, including, among others, discount levels of the trading price of the Funds’

shares compared to net asset value (“NAV”), the use and risks of leverage, the marketplace for closed-end funds (“CEFs”)

in the energy infrastructure sector, and continued focus by activist investors on the Funds. Following a review with the Adviser of strategic

alternatives for each Fund, each Board believes the Merger may benefit its Fund and its stockholders through (among other reasons) the

following:

| |

● |

The potential for higher common stock net earnings and distribution levels

following the Merger, due to operating economies from the combined fund’s scale; |

| |

● |

The potential for narrowing the discount to NAV at which the Funds’

shares have traded, as a result of the larger size of the combined fund and an increased level of distributions in the Acquiring

Fund after the Merger; |

| ● | Continuation of the Funds’ common investment objective

of seeking a high level of total return, emphasizing current distributions, and using the

same portfolio management team but implementing TYG’s broader investment focus within

the energy infrastructure sector; |

| ● | Continuation of the Funds’ CEF structure, where

shares are not continuously offered and do not have daily redemptions thereby avoiding the

portfolio trading costs associated with managing flows in and out of the fund, and allowing

for use of structural leverage (provided by preferred stock and indebtedness) to potentially

increase investment returns; |

| ● | The potential for greater secondary market liquidity and

improved secondary market trading for common stock as a result of the combined fund’s

greater share volume; and |

| |

● |

Lower net overall fees and expenses and total fund operating expenses (excluding

leverage and tax expense), in each case as a percentage of net assets, of the combined funds. |

Each Board considered that the Merger of its Fund

will allow stockholders of the Fund to continue their investment in a closed-end fund structure having the same investment adviser and

being managed by the same portfolio management team as the Funds. Each Fund Board considered the Adviser’s recommendation that

the Acquiring Fund continue the investment objectives and policies of both Funds – an objective to seek a high level of total return,

emphasizing current distributions --- through the Acquiring Fund’s investment strategy to invest in equity securities of energy

infrastructure companies more broadly than the Target Fund’s current strategy of investment in midstream energy companies primarily

in the natural gas infrastructure industry. The Boards considered that the Acquiring Fund would have an increased level of distributions

that potentially could lower the discount to NAV at which the Funds’ shares have traded. The potential tax consequences and expenses

of portfolio positioning transactions and distributions needed to accomplish the Merger and align to the TYG investment strategy, and

the estimated transaction costs for the Merger, were also considered by each Board. In addition, each Board noted that after the Merger

the Acquiring Fund would have lower overall fees and expenses, as a percentage of net assets. The Boards considered that the Merger may

have the additional benefits of avoiding the extraordinary costs associated with potential future proxy contests and litigation associated

with activist investors. The Boards also considered the value of certain stockholder claims and demands relating to the Funds, the evaluation

of such claims and demands by a committee of the Boards with the assistance of independent counsel, and the impact of the Merger on such

claims and demands.

Based on the foregoing and

as further described in the Proxy Statement/Prospectus, each Board, including the Directors who are not “interested persons”

(as defined in the 1940 Act) of the Funds, on September 4, 2024, unanimously approved the Merger and determined that the Merger would

be in the overall best interests of the Fund and not dilutive to the interests of the stockholders thereof. Accordingly, the Target Fund

Board recommends that stockholders of the Target Fund approve the Merger and the Acquiring Fund Board recommends that Acquiring Fund

stockholders approve the Share Issuance. See “Proposal 1: Authorization of the Merger—C. Information About the Merger—Background

and Board Considerations Relating to the Proposed Merger” at page 25 for additional information about each Board’s considerations

relating to the Merger.

Material Federal Income Tax Consequences of

the Merger

The Merger is intended to

qualify as a “reorganization” for federal income tax purposes. Provided the Merger qualifies as a reorganization for federal

income tax purposes, each Target Fund stockholder generally will not recognize any gain or loss, except with respect to cash received

in lieu of a fractional share of Acquiring Fund common stock. The foregoing, including that the Merger will qualify as a reorganization

for federal income tax purposes, will rely on the position that the New Acquiring Fund MRP Shares to be issued in the Merger, if any,

will constitute equity of the Acquiring Fund for federal income tax purposes. See “Proposal 1: Authorization of the Merger—C.

Information About the Merger—Federal Income Tax Consequences of the Merger” at page 38.

As a condition to the Funds’

obligation to consummate the Merger, each Fund will receive a tax opinion stating that the Merger will qualify as a reorganization for

federal income tax purposes. See “Proposal 1: Authorization of the Merger—C. Information About the Merger—Federal Income

Tax Consequences of the Merger” at page 38. If a stockholder chooses to sell Target Fund shares prior to the Merger, such sale

may generate taxable gain or loss.

Notwithstanding the foregoing,

the Merger involves additional tax implications that could significantly impact the Funds and their stockholders. The Target Fund expects

to distribute all its previously undistributed realized net investment income and net capital gains, if any, prior to the closing of

the Merger. All or a portion of such distribution may be taxable to Target Fund stockholders and will generally be taxed as ordinary

income or capital gains for federal income tax purposes. These distributions will be reinvested in additional shares of the Target Fund

unless the stockholder has made an election to receive distributions in cash. Such distributions will be taxable for federal income tax

purposes whether they are paid in cash or reinvested in additional shares.

The Target Fund also may

recognize gains or losses, including ordinary income recapture, because of portfolio sales effected prior to the Merger, including sales

anticipated in connection with the portfolio repositioning. Some or all of these portfolio sales may result in the Target Fund incurring

a federal income tax liability that will reduce the NAV of the Target Fund prior to the closing of the Merger, which would negatively

impact the consideration to be received by Target Fund stockholders in the Merger. In addition, these sales may increase the amount of

net investment income and net capital gain that the Target Fund will distribute prior to the closing of the Merger, which may be taxable

to Target Fund stockholders and will generally be taxed as ordinary income or capital gains for federal income tax purposes.

The federal income tax consequences

of the Merger to each Target Fund stockholder will depend on such Target Fund stockholder’s own situation and many variables. You

should consult with your tax advisor for the specific tax consequences of the Merger.

Comparison of the Funds

Each Fund is a Maryland corporation

registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940 (the “1940 Act”).

Each Fund (i) is managed by the Adviser, (ii) has an investment objective of providing a high level of total return with an

emphasis on current distributions, (iii) seeks to achieve that objective by investing primarily in midstream energy investments

in the energy infrastructure sector, while the Target Fund focuses on natural gas infrastructure entities, and (iv) has nearly identical

fundamental investment policies and similar nonfundamental investment policies. Each Fund was previously taxed as a C corporation and,

beginning with the fiscal year ending November 30, 2023, each Fund intends to qualify for special tax treatment afforded to a regulated

investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”).

After the Merger, the investment strategies and significant operating policies will be those of the Acquiring Fund.

Share Price Data.

The following tables set forth for the periods indicated therein, with respect to the Funds: (i) the high and low sales price for

common stock reported as of the end of the day on the applicable exchange; (ii) the high and low NAV of the common stock; and (iii) the

high and low of the premium/(discount) to NAV (expressed as a percentage of NAV) of the common stock.

| Target Fund |

| |

|

|

|

|

|

|

|

Premium/(Discount) as a % |

|

| |

|

Market Price(1) |

|

|

Net Asset Value(2) |

|

|

of Net Asset Value(3) |

|

| Quarter Ended |

|

High |

|

|

Low |

|

|

High |

|

|

Low |

|

|

High |

|

|

Low |

|

| February 2022 |

|

$ |

35.26 |

|

|

$ |

28.61 |

|

|

$ |

42.07 |

|

|

$ |

35.50 |

|

|

|

-16.2 |

% |

|

|

-19.4 |

% |

| May 2022 |

|

$ |

40.31 |

|

|

$ |

33.53 |

|

|

$ |

48.44 |

|

|

$ |

41.69 |

|

|

|

-16.8 |

% |

|

|

-19.6 |

% |

| August 2022 |

|

$ |

39.76 |

|

|

$ |

29.91 |

|

|

$ |

49.19 |

|

|

$ |

37.88 |

|

|

|

-19.2 |

% |

|

|

-21.0 |

% |

| November 2022 |

|

$ |

38.32 |

|

|

$ |

30.70 |

|

|

$ |

46.20 |

|

|

$ |

37.49 |

|

|

|

-17.1 |

% |

|

|

-18.1 |

% |

| February 2023 |

|

$ |

37.96 |

|

|

$ |

33.66 |

|

|

$ |

44.78 |

|

|

$ |

41.54 |

|

|

|

-15.2 |

% |

|

|

-19.0 |

% |

| May 2023 |

|

$ |

36.24 |

|

|

$ |

30.50 |

|

|

$ |

43.13 |

|

|

$ |

37.56 |

|

|

|

-16.0 |

% |

|

|

-18.8 |

% |

| August 2023 |

|

$ |

36.64 |

|

|

$ |

31.82 |

|

|

$ |

42.99 |

|

|

$ |

37.99 |

|

|

|

-14.8 |

% |

|

|

-16.2 |

% |

| November 2023 |

|

$ |

35.75 |

|

|

$ |

31.83 |

|

|

$ |

42.36 |

|

|

$ |

37.75 |

|

|

|

-15.6 |

% |

|

|

-15.7 |

% |

| February 2024 |

|

$ |

36.10 |

|

|

$ |

33.17 |

|

|

$ |

43.29 |

|

|

$ |

40.42 |

|

|

|

-16.6 |

% |

|

|

-17.9 |

% |

| May 2024 |

|

$ |

41.60 |

|

|

$ |

36.40 |

|

|

$ |

50.04 |

|

|

$ |

43.94 |

|

|

|

-16.9 |

% |

|

|

-17.2 |

% |

| August 2024 |

|

$ |

45.11 |

|

|

$ |

39.46 |

|

|

$ |

52.99 |

|

|

$ |

47.58 |

|

|

|

-14.9 |

% |

|

|

-17.1 |

% |

| (1) | Based on high and low closing market price for the

respective quarter. |

| (2) | Based on the net asset value on the day of the high

and low closing market prices, as applicable, as of the close of regular trading on the NYSE

(normally 4:00 p.m. eastern time). |

| (3) | Calculated based on the information presented. |

| Acquiring

Fund |

| |

|

|

|

|

|

|

|

Premium/(Discount)

as a % |

|

| |

|

Market

Price(1) |

|

|

Net

Asset Value(2) |

|

|

of

Net Asset Value(3) |

|

| Quarter

Ended |

|

High |

|

|

Low |

|

|

High |

|

|

Low |

|

|

High |

|

|

Low |

|

| February 2022 |

|

$ |

31.47 |

|

|

$ |

26.12 |

|

|

$ |

37.58 |

|

|

$ |

33.87 |

|

|

|

-16.3 |

% |

|

|

-22.9 |

% |

| May 2022 |

|

$ |

36.56 |

|

|

$ |

30.03 |

|

|

$ |

43.47 |

|

|

$ |

38.06 |

|

|

|

-15.9 |

% |

|

|

-21.1 |

% |

| August 2022 |

|

$ |

36.15 |

|

|

$ |

27.57 |

|

|

$ |

43.87 |

|

|

$ |

34.31 |

|

|

|

-17.6 |

% |

|

|

-19.6 |

% |

| November 2022 |

|

$ |

35.75 |

|

|

$ |

29.78 |

|

|

$ |

42.82 |

|

|

$ |

35.33 |

|

|

|

-16.5 |

% |

|

|

-15.7 |

% |

| February 2023 |

|

$ |

34.12 |

|

|

$ |

30.89 |

|

|

$ |

41.13 |

|

|

$ |

36.86 |

|

|

|

-17.0 |

% |

|

|

-16.2 |

% |

| May 2023 |

|

$ |

31.59 |

|

|

$ |

26.95 |

|

|

$ |

38.16 |

|

|

$ |

33.49 |

|

|

|

-17.2 |

% |

|

|

-19.5 |

% |

| August 2023 |

|

$ |

31.12 |

|

|

$ |

27.39 |

|

|

$ |

36.81 |

|

|

$ |

33.89 |

|

|

|

-15.5 |

% |

|

|

-19.2 |

% |

| November 2023 |

|

$ |

30.60 |

|

|

$ |

26.98 |

|

|

$ |

36.03 |

|

|

$ |

31.47 |

|

|

|

-15.1 |

% |

|

|

-14.3 |

% |

| February 2024 |

|

$ |

29.82 |

|

|

$ |

27.63 |

|

|

$ |

35.65 |

|

|

$ |

34.24 |

|

|

|

-16.4 |

% |

|

|

-19.3 |

% |

| May 2024 |

|

$ |

35.15 |

|

|

$ |

29.17 |

|

|

$ |

41.74 |

|

|

$ |

36.28 |

|

|

|

-15.8 |

% |

|

|

-19.6 |

% |

| August 2024 |

|

$ |

36.98 |

|

|

$ |

32.65 |

|

|

$ |

42.45 |

|

|

$ |

39.53 |

|

|

|

-12.9 |

% |

|

|

-17.4 |

% |

| (1) | Based on high and low closing market price for the

respective quarter. |

| (2) | Based on the net asset value on the day of the high

and low closing market prices, as applicable, as of the close of regular trading on the NYSE

(normally 4:00 p.m. eastern time). |

| (3) | Calculated based on the information presented. |

The shares of common stock

of each Fund have historically traded at a discount to net asset value. It is not possible to state whether the Acquiring Fund common

stock will trade at a premium or discount to net asset value following the Merger, or what the extent of any such premium or discount

might be.

Investment Objective and

Principal Investment Strategies. The Funds have similar investment objectives and policies, but there are differences. Each Fund’s

investment objective is to seek a high level of total return with an emphasis on current distributions paid to stockholders. Each of

the Funds has substantially identical fundamental investment policies, with the only difference being that the Acquiring Fund concentrates

(invests at least 25% or more of total assets) in the group of industries constituting the energy infrastructure sector, whereas the

Target Fund concentrates (invests at least 25% or more of total assets) in the group of industries constituting the energy sector. For

a complete listing of these fundamental investment policies of the Acquiring Fund see “Proposal 1: Authorization of the Merger—

D. Additional Information About the Investment Policies of the Acquiring Fund and Management of the Fund—Investment Policies”

at page 43.

The following summary compares

the current principal investment strategies and policies of the Acquiring Fund with the current principal investment policies and strategies

of the Target Fund as of the date of this Joint Prospectus/proxy Statement.

|

Acquiring

Fund(2) |

Compare |

| Non-Fundamental

Principal Investment Policies |

| |

| Principal Investment Strategy |

Principal Investment Strategy |

Principal Investment Strategy |

| |

|

|

| Under normal circumstances, the Target Fund invests

at least 80% of its total investments in equity securities of midstream energy entities in the energy infrastructure sector, including

MLPs, with at least 50% of its total investments in equity securities of natural gas infrastructure entities. |

Under normal circumstances, the Acquiring Fund

invests at least 90% of its total investments, defined as the value of all investments reported as total investments in its schedule

of investments, in securities of energy infrastructure companies. Energy infrastructure companies engage in the business of transporting,

processing, storing, distributing, or marketing natural gas, natural gas liquids, coal, crude oil, or refined petroleum products,

or exploring, developing, managing, or producing such commodities. Additionally, energy infrastructure includes renewables and power

infrastructure companies that generate, transport and distribute electricity. |

The Target Fund emphasizes natural gas infrastructure entities, while the Acquiring

Fund invests more broadly in energy infrastructure companies. |

| Master Limited Partnerships |

Master Limited Partnerships |

Master Limited Partnerships |

| |

|

|

| As a regulated investment company, the Target

Fund may invest up to 25% of its total assets in MLPs. |

As a regulated investment company, the Acquiring

Fund may invest up to 25% of its total assets in MLPs. |

Identical. |

| |

|

|

| Restricted Securities |

Restricted Securities |

Restricted Securities |

| |

|

|

| The Target Fund may also invest up to 50% of

its total investments in restricted securities, primarily through direct investments. The aggregate of all Target Fund investments

in private companies that do not have any publicly traded shares or units is limited to 5% of its total investments. |

The Acquiring Fund may invest up to 30% of its

total investments in restricted securities, primarily through direct placements. Subject to this policy, the Acquiring Fund may invest

without limitation in illiquid securities. The aggregate of all Acquiring Fund investments in private companies that do not have

any publicly traded shares or units are limited to 5% of its total investments. |

The Target Fund may invest to a great degree

in restricted securities. |

| |

|

|

| Below Investment Grade |

Below Investment Grade |

Below Investment Grade |

| |

|

|

The Target

Fund may invest up to 20% of its total investments in debt securities of midstream energy

companies, including securities rated below investment grade (commonly referred to as “junk

bonds”). Below investment grade debt securities will be rated at least B3 by Moody’s

Investors Service, Inc. (“Moody’s”) and at least B- by Standard &

Poor’s Ratings Group (“S&P”) at the time of purchase, or comparably

rated by another statistical rating organization or if unrated, determined to be of comparable

quality by the Adviser. The Target Fund currently has no specific maturity policy with respect

to debt securities. |

The Acquiring Fund may invest up to 25% of its

total investments in debt securities of energy infrastructure companies, including certain securities rated below investment grade

(“junk bonds”). Below investment grade debt securities will be rated at least B3 by Moody’s and at least B−

by S&P at the time of purchase, or comparably rated by another statistical rating organization or if unrated, determined to be

of comparable quality by the Adviser. |

The Target Fund limits below investment grade

investments to 20% and the Acquiring Fund limits below investment grade investments to 25%. |

| |

|

|

| Single Issuer |

Single Issuer |

Single Issuer |

| |

|

|

The Target

Fund will not invest more than 10% of its total investments in any single issuer. |

The Acquiring Fund will not invest more than

10% of its total investments in any single issuer. |

Identical. |

| Short Sales |

Short Sales |

Short Sales |

| |

|

|

The Target

Fund will not engage in short sales. |

The Acquiring Fund will not engage in short sales. |

Identical. |

| Covered Call Options |

Covered Call Options |

Covered Call Options |

| |

|

|

| The Target Fund may write covered call options,

up to 10% of its total investments. |

The Acquiring Fund may write covered call options,

up to 10% of its total investments. |

Identical. |

| Temporary Defensive Measures |

Temporary Defensive Measures |

Temporary Defensive Measures |

| |

|

|

Although

inconsistent with the Target Fund’s investment objective, under (i) adverse market

or economic conditions which results in the Target Fund taking a temporary defensive position

or (ii) pending investment of offering or leverage proceeds, the Target Fund may invest

100% of its total investments in mutual funds, cash, cash equivalents, securities issued

or guaranteed by the U.S. Government or its instrumentalities or agencies, high quality,

short-term money market instruments, short-term debt securities, certificates of deposit,

bankers’ acceptances and other bank obligations, commercial paper or other liquid fixed

income securities. |

Under adverse market or economic conditions,

the Acquiring Fund may invest up to 100% of its total investments in securities issued or guaranteed by the U.S. Government or its

instrumentalities or agencies, short-term debt securities, certificates of deposit, bankers’ acceptances and other bank obligations,

commercial paper rated in the highest category by a rating agency or other liquid fixed income securities deemed by the Adviser to

be consistent with a defensive posture (collectively, “short-term securities”), or may hold cash. |

Unlike the Acquiring Fund, the Target Fund may utilize temporary defensive

measures pending investment of offering or leverage proceeds in addition to under adverse market or economic conditions. |

| |

|

|

| Interest Rate Transactions |

Interest Rate Transactions |

Interest Rate Transactions |

| |

|

|

| The Target Fund may use interest rate transactions

for economic hedging purposes only, in an attempt to reduce the interest rate risk arising from its leveraged capital structure.

The Target Fund does not intend to hedge the interest rate risk of its portfolio holdings. |

The Acquiring Fund may use interest rate transactions

for hedging purposes only, in an attempt to reduce the interest rate risk arising from its leveraged capital structure. The Acquiring

Fund does not intend to hedge the interest rate risk of its portfolio holdings. |

No material differences. Differences arise solely from word choice. |

| (1) | Investment limitations stated as

a maximum percentage of the Target Fund’s assets or investments are only applied immediately

after, and because of, an investment or a transaction by the Target Fund to which the limitation

is applicable (other than the limitations on borrowing). Accordingly, any later increase

or decrease resulting from a change in values, net assets or other circumstances will not

be considered in determining whether the investment complies with the Target Fund’s

investment limitations. We define total assets as the value of securities, cash or other

assets held, including securities or assets obtained through leverage, and interest accrued

but not yet received. We define “total investments” as the value of all investments

reported as total investments in the Fund’s schedule of investments. |

| (2) | Investment limitations stated as

a maximum percentage of the Acquiring Fund’s assets or investments are only applied

immediately after, and because of, an investment or a transaction by the Acquiring Fund to

which the limitation is applicable (other than the limitations on borrowing). Accordingly,

any later increase or decrease resulting from a change in values, net assets or other circumstances

will not be considered in determining whether the investment complies with the Acquiring

Fund’s investment limitations. All limitations that are based on a percentage of total

assets include assets obtained through leverage. |

Leverage. Each

Fund currently employs leverage through borrowings and preferred stock. Certain important ratios related to each Fund’s use of

leverage for the last three fiscal years are set forth below:

| Target Fund (NTG) | |

2023 | | |

2022 | | |

2021 | |

| Asset Coverage –—Preferred Stock | |

| 506 | % | |

| 480 | % | |

| 433 | % |

| Asset Coverage — Borrowings | |

| 680 | % | |

| 702 | % | |

| 543 | % |

| Acquiring Fund (TYG) | |

2023 | | |

2022 | | |

2021 | |

| Asset Coverage –—Preferred Stock | |

| 453 | % | |

| 402 | % | |

| 395 | % |

| Asset Coverage — Borrowings | |

| 677 | % | |

| 529 | % | |

| 519 | % |

Please refer to the financial

highlights in Appendix B for asset coverage ratios for each of the last ten fiscal years.

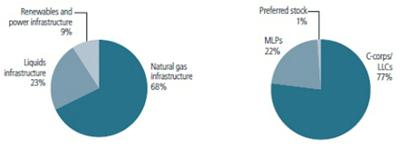

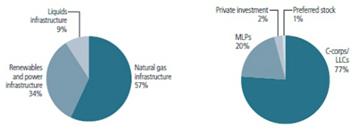

Asset Type. A comparison

of the asset type and investment structure of the portfolios of the Funds, as of May 31, 2024, is set forth below.

Target Fund

Acquiring Fund

Risks of the Funds.

Because the Target Fund and the Acquiring Fund have similar principal investment strategies, they are subject to some of the same risks,

including cybersecurity risk, epidemic risk, capital markets risk, restricted securities risk, equity securities risk, MLP risk, liquidity

risk, concentration risk and market discount risk, although the Target Fund is subject to certain additional risks due to its emphasis

on natural gas infrastructure entities. The Merger is also subject to certain risks, such as the risk that the anticipated benefits of

the Merger may not be realized, as well as certain tax-related risks and considerations. See “Proposal 1: Authorization of the

Merger— B. Risk Factors—Principal Risks Comparison” at page 11.

Description of the Shares.

The shares of the Target Fund and the Acquiring Fund have similar voting rights, the same rights with respect to the payment of dividends

and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the respective Fund and have no rights to

cumulative voting. Holders of shares of common and preferred stock of each Fund are entitled to one vote per share on any matter on which

the shares are entitled to vote.

Share Information.

| Fund | |

Authorized

Common

Shares | |

Common

Shares

Outstanding | | |

Par Value

Per Share | | |

Preemptive,

Appraisal or

Exchange Rights | |

Rights to

Cumulative

Voting | |

Exchange on

which Shares

are Listed |

| Target Fund | |

100,000,000 | |

| 5,092,810 | | |

$ | 0.001 | | |

None | |

None | |

NYSE |

| Acquiring Fund | |

100,000,000 | |

| 10,764,933 | | |

$ | 0.001 | | |

None | |

None | |

NYSE |

In addition, the Target Fund

currently has 550,151 outstanding shares of Mandatory Redeemable Preferred Stock (“MRP Shares”), with a liquidation value

of $25.00 per share plus any accumulated but unpaid distributions, whether or not declared. Holders of Target Fund MRP Shares are entitled

to receive cash interest payments each quarter at a fixed rate until maturity.

| Fund | |

MRP Series | |

MRP Shares

Outstanding | | |

Liquidation

Value | | |

Aggregate

Liquidation

Preference | | |

Mandatory

Redemption Date |

| Target Fund | |

Series E* | |

| 153,939 | | |

$ | 25.000 | | |

$ | 3,848,475 | | |

December 13, 2024 |

| Target Fund | |

Series F | |

| 96,212 | | |

$ | 25.000 | | |

$ | 2,405,300 | | |

December 13, 2027 |

| Target Fund | |

Series H | |

| 300,000 | | |

$ | 25.000 | | |

$ | 7,500,000 | | |

December 17, 2027 |

| * | Expected to be redeemed on or before

the Closing Date (as defined below). |

The Acquiring Fund currently has 3,566,061 outstanding

shares of MRP Shares, with a liquidation value of $10.00 per share plus any accumulated but unpaid distributions, whether or not declared.

Holders of Acquiring Fund MRP Shares are entitled to receive cash interest payments semi-annually at a fixed rate until maturity.

| Fund | |

MRP Series | |

MRP Shares

Outstanding | | |

Liquidation

Value | | |

Aggregate

Liquidation

Preference | | |

Mandatory

Redemption Date |

| Acquiring Fund | |

Series E | |

| 1,566,061 | | |

$ | 10.000 | | |

$ | 15,660,610 | | |

December 17, 2024 |

| Acquiring Fund | |

Series F | |

| 2,000,000 | | |

$ | 10.000 | | |

$ | 20,000,000 | | |

December 17, 2026 |

Distributions and Dividend

Reinvestment Plan. Each Fund has adopted a managed distribution policy. Annual distribution amounts are expected to fall in the range

of 7% to 10% of the average week-ending NAV per share for the prior fiscal semi-annual period, provided that the Acquiring Fund intends

to increase distributions by approximately 40% after the Merger. Distribution amounts will be reset both up and down to provide a consistent

return on trailing NAV. Under the managed distribution policy, distribution amounts will normally be reset in February and August,

with no changes in distribution amounts in May and November. A Fund may designate a portion of its distributions as capital gains

and may also distribute additional capital gains in the last quarter of the year to meet annual excise tax distribution requirements.

Distribution amounts are subject to change from time to time at the discretion of a Board of Directors of the Fund.

In connection with the managed

distribution policy, the Funds are relying on exemptive relief permitting them to make long-term capital gain distributions throughout

the year. NTG distributes a fixed amount per share of common stock, currently $0.81, each quarter to its common stockholders. TYG distributes

a fixed amount per common stock, currently $0.78, each quarter to its common stockholders.

Dividends from net investment

income of the Acquiring Fund, if any, are expected to be declared and paid quarterly by the Acquiring Fund. The Acquiring Fund will distribute

its net realized capital gains, if any, to stockholders at least annually. Distributions in cash from the Acquiring Fund may be reinvested

automatically in additional whole shares only if the broker through whom you purchased shares makes such option available, and such shares

will generally be reinvested by the broker based upon the market price of those shares and may be subject to brokerage commissions charged

by the broker. Distributions are taxable for federal income tax purposes whether they are paid in cash or reinvested in additional shares.

Fees and Expenses

The following tables set

forth the fees and expenses of investing in shares of the Target Fund and the Acquiring Fund. Expenses for the Target Fund and Acquiring

Fund are based on operating expenses for the six-month period ended May 31, 2024 (annualized). The pro forma annual operating expenses

are projections for a 12-month period, assuming each Fund’s capital structure and asset levels as of May 31, 2024. These pro

forma projections include the change in operating expenses expected because of the Merger, assuming the Combined Fund’s capital

structure and asset levels as of May 31, 2024. Investors may pay other fees, such as brokerage commissions and other fees to

financial intermediaries, which are not reflected in the table and example below.

| | |

NTG Target

Fund

Based on

Net Assets(1) | | |

TYG Acquiring

Fund

Based on

Net Assets(1) | | |

Combined

Fund

pro forma(2) | |

| Annual Fund Operating Expenses (expenses

that you pay each year as a percentage of the value of your investment) | |

| | |

| | |

| |

| Management Fees(3) | |

| 1.18 | % | |

| 1.22 | % | |

| 1.19 | % |

| Dividends and Expenses on Preferred Stock and Interest

and Related Expenses from Borrowings and Other Leverage Expenses | |

| 0.98 | % | |

| 1.18 | % | |

| 1.07 | %(4) |

| Other Expenses | |

| 0.55 | % | |

| 0.39 | % | |

| 0.31 | % |

| Income Tax Expense | |

| 0.02 | % | |

| 0.07 | % | |

| 0.05 | % |

| Total Fund Expenses | |

| 2.73 | % | |

| 2.86 | % | |

| 2.62 | % |

| Less Expenses Reimbursed by Adviser | |

| - | | |

| - | | |

| - | |

| Total Annual Fund Expenses (net of expense reimbursement) | |

| 2.73 | % | |

| 2.86 | % | |

| 2.62 | % |

| (1) | Based

on average daily net assets for the six-month period ended May 31, 2024. |

| (2) | Assumes

the consummation of the Merger. |

| (3) | The management

fee of each Fund is calculated based on its Managed Assets, which means the average daily

gross asset value of the Fund (which includes assets attributable to the principal amount

of any borrowings), minus accrued liabilities (other than the principal amount of such borrowings).

The management fee is presented in the table as a percentage of net assets. |

| (4) | Includes

the amortization of offering costs for the issuance of preferred shares by the Acquiring

Fund (TYG) in the Merger. |

Example

The following example is

intended to help you compare the costs of investing in the shares of the Combined Fund on a pro forma basis following the Merger with

the costs of investing in the Target Fund and the Acquiring Fund absent the Merger. An investor would pay the following expenses on a

$1,000 investment that is held for the time periods provided in the table, assuming that all dividends and other distributions are reinvested

and that operating expenses remain the same. The example also assumes a 5% annual return. The example should not be considered a representation

of future expenses or returns. Actual expenses may be greater or lesser than those shown whether you hold or sell your shares.

| |

|

1 Year |

|

|

3 Years |

|

|

5 Years |

|

|

10 Years |

|

| NTG Target Fund (based on net assets) |

|

$ |

28 |

|

|

$ |

85 |

|

|

$ |

145 |

|

|

$ |

307 |

|

| TYG Acquiring Fund (based on net assets) |

|

$ |

29 |

|

|

$ |

89 |

|

|

$ |

151 |

|

|

$ |

319 |

|

| Combined Fund (based on net assets) |

|

$ |

27 |

|

|

$ |

82 |

|

|

$ |

139 |

|

|

$ |

296 |

|

The Board of Directors

of the Target Fund recommends that stockholders approve the Merger at the Meeting to be held on November 25, 2024. Stockholder approval

of the Merger requires the affirmative vote of the majority of votes of the Target Fund entitled to be cast on the matter. Lenders under

the Funds’ unsecured revolving credit facility and senior notes will not vote on the Merger. See “Proposal 1: Authorization

of the Merger—C. Information About the Merger—Capitalization” at page 30.

Subject to the requisite

approval of the stockholders of the Target Fund with regard to the Merger and the requisite approval of the stockholders of the Acquiring

Fund with regard to the Share Issuance, it is expected that the closing date of the Merger (the “Closing Date”) will occur

in the fourth quarter of 2024, but it may be at a different time as described herein.

The Board of Directors

of the Target Fund unanimously recommends that Target Fund stockholders vote “FOR” the Merger.

B.

Risk Factors

In

evaluating the Merger, you should carefully consider the risks of the Acquiring Fund to which you will be subject if the Merger is approved