--12-31Q3false0001763415 UnlimitedUnlimited00017634152024-06-3000017634152024-01-012024-09-300001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-052024-01-050001763415bitb:LukkaPrimeRateMember2024-01-012024-09-3000017634152024-01-102024-09-300001763415bitb:CoinbaseCustodyTrustCompanyLlcMember2024-01-012024-09-300001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-0900017634152024-01-080001763415bitb:InvestmentInBitcoinMember2024-09-300001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-112024-01-110001763415us-gaap:FairValueInputsLevel3Memberbitb:InvestmentsInCryptoAssetsMember2024-09-300001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-102024-01-100001763415bitb:BitwiseAssetManagementIncMember2024-01-102024-01-100001763415us-gaap:FairValueInputsLevel1Memberbitb:InvestmentsInCryptoAssetsMember2024-09-300001763415bitb:BitwiseAssetManagementIncMember2023-11-090001763415bitb:BitwiseInvestmentAdvisersLlcMember2024-01-092024-01-090001763415bitb:BitwiseAssetManagementIncMember2023-11-092023-11-090001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-0800017634152024-01-090001763415bitb:CmeCfBitcoinMember2024-01-012024-09-3000017634152023-01-012023-12-3100017634152023-12-3100017634152024-09-300001763415srt:MaximumMember2023-12-3100017634152024-11-060001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-1000017634152024-07-012024-09-300001763415us-gaap:FairValueInputsLevel2Memberbitb:InvestmentsInCryptoAssetsMember2024-09-300001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-050001763415bitb:BitwiseInvestmentManagerLlcMember2024-01-092024-01-09bitb:Trusteebitb:Bitcoinxbrli:purexbrli:sharesiso4217:USD

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended September 30, 2024.

or

☐ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to .

Commission File Number: 001-41902

BITWISE BITCOIN ETF

(Exact name of registrant as specified in its charter)

|

|

|

Delaware |

|

83-6613214 |

(State or other jurisdiction of |

|

(I.R.S. Employer |

incorporation or organization) |

|

Identification No.) |

Bitwise Investment Advisers, LLC

250 Montgomery Street, Suite 200

San Francisco, California 94104

(415) 707-3663

(Address, including zip code, and telephone number, including area code, of registrant’s primary executive offices)

|

|

|

|

|

Title of each class: |

|

Trading Symbol(s) |

|

Name of each exchange on which registered: |

Bitwise Bitcoin ETF Shares |

|

BITB |

|

NYSE Arca, Inc. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

|

|

|

|

|

|

Large Accelerated Filer |

☐ |

|

Accelerated Filer |

☐ |

|

|

|

|

|

|

|

Non-Accelerated Filer |

☒ |

|

Smaller Reporting Company |

☒ |

|

|

|

|

|

|

|

Emerging Growth Company |

☒ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided in Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act.). ☐ Yes ☒ No

The registrant had 74,290,000 outstanding shares as of November 6, 2024.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (the “Quarterly Report”) includes “forward-looking statements” with respect to the financial conditions, results of operations, plans, objectives, future performance and business of Bitwise Bitcoin ETF (the “Trust”). In some cases, you can identify forward-looking statements by terminology such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other than statements of historical fact) included in this Quarterly Report that address activities, events, or developments that will or may occur in the future, including such matters as movements in the crypto asset markets, the Trust’s operations, the plans of Bitwise Investment Advisers, LLC (the “Sponsor”), and references to the Trust’s future success and other similar matters, are forward-looking statements. These statements are only predictions. Actual events or results may differ materially from such statements. These statements are based upon certain assumptions and analyses the Sponsor has made based on its perception of historical trends, current conditions, and expected future developments, as well as other factors appropriate in the circumstances.

Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions is subject to a number of risks and uncertainties, including, but not limited to, any risk factors described in Part II, Item 1A. Risk Factors of this Quarterly Report on Form 10-Q and in Part I, Item 1A. Risk Factors or other sections of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2023, filed with the Securities and Exchange Commission (the “SEC”) on March 27, 2024.

Factors which could have a material adverse effect on the Trust's business, financial condition or results of operations and future prospects or which could cause actual results to differ materially from the Trust's expectations include, but are not limited to:

•the special considerations discussed in this Quarterly Report, including the regulatory and tax treatment of the transaction contemplated by that certain Asset Purchase and Contribution Agreement (the “Asset Purchase Agreement”) entered into by and among the Trust, the Sponsor, Osprey Bitcoin Trust (the “Osprey Trust”) and Osprey Funds, LLC, the sponsor of the Osprey Trust, on August 26, 2024 (the “Asset Purchase”);

•the ability of the Trust and the Osprey Fund to consummate the Asset Purchase, including the satisfaction or waiver (if applicable) of the conditions to the Asset Purchase Agreement, including, among others, (i) effectiveness of the registration statement on Form S-1 the Trust filed with the SEC on October 8, 2024; and (ii) receipt of approval for listing and trading on the NYSE Arca, Inc., the Shares of the Trust to be issued in connection with the asset purchase;

•the extreme volatility of trading price that bitcoin has experienced in recent periods and may continue to experience, which could have a material adverse effect on the value of the Shares of the Trust;

•the recentness of the development of bitcoin and other crypto assets, and the uncertain medium-to-long term value of the Shares due to a number of factors relating to the capabilities and technology developments regarding the use of bitcoin and other crypto assets and to the fundamental investment characteristics of bitcoin and other crypto assets;

•the value of the Shares depending on the acceptance of bitcoin and blockchain technologies, a new and rapidly evolving industry;

•the unregulated nature and lack of transparency surrounding the operations of blockchain technologies and crypto assets, which may adversely affect the value of bitcoin and the Shares;

•the limited history of the Trust;

•the possibility that the Shares may trade at a price that is at, above or below the Trust’s NAV per-share;

•changes in laws or regulations, or actions taken by governmental authorities or U.S. federal or state regulatory bodies, including the SEC and the Commodity Futures Trading Commission, that may affect the value of the Shares or restrict the use of bitcoin or other crypto assets, the mining activity or the operation of Bitcoin network, or the bitcoin market in a manner that adversely affects the value of the Shares;

•the possibility that the Trust or the Sponsor could be subject to regulation as a money service business or money transmitter, which could result in extraordinary expenses to the Trust or the Sponsor and also result in decreased liquidity for the Shares;

•regulatory changes or interpretations that could obligate the Trust or the Sponsor to register and comply with new regulations, resulting in potentially extraordinary, nonrecurring expenses to the Trust;

•potential conflicts of interest that may arise among the Sponsor or its affiliates and the Trust;

•the Trust’s reliance on the security, stability, and performance of its service providers, including the Bitcoin Custodian, Cash Custodian, Prime Execution Agent, and other intermediaries, which may be subject to operational failures, conflicts of interest, and regulatory actions, potentially adversely affecting its operations and the value of the Shares;

•general economic, market and business conditions, and political developments, including, without limitation, global pandemics and the societal and government responses thereto, which could negatively impact the value of the Trust’s holdings in bitcoin and significantly disrupt its operations; and

•any additional risk factors discussed in Part II, Item 1A. Risk Factors and Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Quarterly Report on Form 10-Q, as well as those described from time to time in the Trust’s future reports filed with the SEC.

All the forward-looking statements made in this Quarterly Report are qualified by these cautionary statements, and there can be no assurance that the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Shares.

Should one or more of these risks discussed in the section entitled “Risk Factors” or other uncertainties materialize, or should underlying assumptions prove incorrect, actual outcomes may vary materially from those described in forward-looking statements. Forward-looking statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made, and neither the Trust nor the Sponsor is under a duty to update any of the forward-looking statements to conform such statements to actual results or to reflect a change in the Sponsor’s expectations or predictions, other than as required by applicable laws. Investors are therefore cautioned against relying on forward-looking statements.

EMERGING GROWTH COMPANY STATUS

The Trust is an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act (the “JOBS Act”) and, as such, may elect to comply with certain reduced reporting requirements. For as long as the Trust is an emerging growth company, unlike other public companies, it will not be required to:

•provide an auditor’s attestation report on management’s assessment of the effectiveness of its system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002;

•comply with any new requirements adopted by the Public Company Accounting Oversight Board (“PCAOB”) requiring mandatory auditor rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer;

•comply with any new audit rules adopted by the PCAOB after April 5, 2012, unless the Securities and Exchange Commission determines otherwise;

•provide certain disclosure regarding executive compensation required of larger public companies; or

•obtain shareholder approval of any golden parachute payments not previously approved.

The Trust will cease to be an “emerging growth company” upon the earliest of (i) when it has $1.235 billion or more in total annual gross revenues during its most recently completed fiscal year; (ii) when it is deemed to be a large accelerated filer under Rule 12b-2 promulgated pursuant to the Securities Exchange Act of 1934; (iii) when it has issued more than $1.0 billion of non-convertible debt over a three-year period; or (iv) the last day of the fiscal year following the fifth anniversary of its initial public offering.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933 for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies; however, the Trust is choosing to “opt out” of such extended transition period, and as a result, the Trust will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that the Trust’s decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Bitwise Bitcoin ETF

Table of Contents

PART I – FINANCIAL INFORMATION:

Item 1. Financial Statements (Unaudited)

BITWISE BITCOIN ETF

STATEMENTS OF ASSETS AND LIABILITIES

(Amounts in thousands, except Share and per-share amounts)

|

|

|

|

|

|

|

|

|

|

|

|

September 30, 2024 |

|

|

December 31, 2023* |

|

|

|

|

(unaudited) |

|

|

|

|

|

Assets |

|

|

|

|

|

|

|

Investment in bitcoin, at fair value (cost $2,068,421) |

|

$ |

2,502,767 |

|

|

$ |

— |

|

|

Bitcoin sold receivable |

|

|

9,672 |

|

|

|

— |

|

|

Cash |

|

|

— |

|

|

|

0 |

|

(1) |

Total assets |

|

|

2,512,439 |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

Liabilities |

|

|

|

|

|

|

|

Capital shares payable |

|

|

9,672 |

|

|

|

— |

|

|

Sponsor Fee payable |

|

|

371 |

|

|

|

— |

|

|

Total liabilities |

|

|

10,043 |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

Net Assets |

|

$ |

2,502,396 |

|

|

$ |

0 |

|

(1) |

|

|

|

|

|

|

|

|

Shares issued and outstanding, no par value, unlimited amount authorized |

|

|

72,380,000 |

|

|

4 |

|

(2) |

Net asset value per share (3) |

|

$ |

34.57 |

|

|

$ |

50.00 |

|

(2) |

* As of December 31, 2023, the Trust held initial seed capital amounting to $200 in cash.

(1) Amount represents less than $500.

(2) Prior to commencement of operations on January 10, 2024, Bitwise Asset Management, Inc. ("BAM"), the parent company of the Sponsor, redeemed the initial seed capital of 4 shares for $200.

(3) Net asset value per share calculated using the principal market valuation as of the date of the financial statements.

The accompanying notes are an integral part of the Financial Statements.

BITWISE BITCOIN ETF

SCHEDULE OF INVESTMENT

(Amounts in thousands, except quantity of bitcoin and percentages)

September 30, 2024 (Unaudited)*

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quantity |

|

|

|

|

|

|

|

|

Percentage of |

|

|

|

|

of bitcoin |

|

|

Cost |

|

|

Fair Value |

|

|

Net Assets |

|

|

Investment in bitcoin^ |

|

|

39,435.5408 |

|

|

$ |

2,068,421 |

|

|

$ |

2,502,767 |

|

|

|

100.01 |

|

% |

Total Investment |

|

|

|

|

$ |

2,068,421 |

|

|

|

2,502,767 |

|

|

|

100.01 |

|

|

Liabilities in excess of other assets |

|

|

|

|

|

|

|

|

(371 |

) |

|

|

(0.01 |

) |

|

Net Assets |

|

|

|

|

|

|

|

$ |

2,502,396 |

|

|

|

100.00 |

|

% |

* No comparative period presented as the Trust commenced operations on January 10, 2024.

^ Crypto assets do not have a singular country or geographic region, therefore country information is omitted.

The accompanying notes are an integral part of the Financial Statements.

Bitwise Bitcoin ETF

Statements of Operations

(Amounts in thousands)

|

|

|

|

|

|

|

|

|

|

|

Three months ended September 30, 2024 |

|

|

For the period

January 10, 2024 (commencement of operations) through September 30, 2024* |

|

|

|

(unaudited) |

|

|

(unaudited) |

|

Investment income |

|

|

|

|

|

|

Investment income |

|

$ |

— |

|

|

$ |

— |

|

Expenses |

|

|

|

|

|

|

Sponsor Fee |

|

|

1,170 |

|

|

|

2,848 |

|

Total Expenses |

|

|

1,170 |

|

|

|

2,848 |

|

Less: Waivers and Reimbursement |

|

|

(55 |

) |

|

|

(906 |

) |

Net Expenses |

|

|

1,115 |

|

|

|

1,942 |

|

Net investment loss |

|

|

(1,115 |

) |

|

|

(1,942 |

) |

|

|

|

|

|

|

|

Net realized and unrealized gain (loss) |

|

|

|

|

|

|

Net realized gain (loss) on investment in bitcoin transferred to pay Sponsor Fee |

|

|

359 |

|

|

|

593 |

|

Net realized gain (loss) on investment in bitcoin sold for redemptions |

|

|

(49,002 |

) |

|

|

(73,204 |

) |

Net change in unrealized appreciation (depreciation) on investment in bitcoin |

|

|

183,925 |

|

|

|

434,346 |

|

Net realized and unrealized gain (loss) |

|

|

135,282 |

|

|

|

361,735 |

|

Net increase (decrease) in net assets resulting from operations |

|

$ |

134,167 |

|

|

$ |

359,793 |

|

* No comparative financial statements have been provided as the Trust’s operations commenced on January 10, 2024.

The accompanying notes are an integral part of the Financial Statements.

Bitwise Bitcoin ETF

Statements of Changes in Net Assets

(Amounts in thousands, except change in Shares issued and redeemed)

|

|

|

|

|

|

|

|

|

|

|

|

Three months ended September 30, 2024 |

|

|

For the period

January 10, 2024 (commencement of operations) through September 30, 2024* |

|

|

|

|

(unaudited) |

|

|

(unaudited) |

|

|

Increase (decrease) in net assets resulting from operations |

|

|

|

|

|

|

|

Net investment loss |

|

$ |

(1,115 |

) |

|

$ |

(1,942 |

) |

|

Net realized gain (loss) on investment in bitcoin transferred to pay Sponsor Fee |

|

|

359 |

|

|

|

593 |

|

|

Net realized gain (loss) on investment in bitcoin sold for redemptions |

|

|

(49,002 |

) |

|

|

(73,204 |

) |

|

Net change in unrealized appreciation (depreciation) |

|

|

183,925 |

|

|

|

434,346 |

|

|

Net increase (decrease) in net assets resulting from operations |

|

|

134,167 |

|

|

|

359,793 |

|

|

|

|

|

|

|

|

|

|

Increase (decrease) in net assets from capital share transactions |

|

|

|

|

|

|

|

Creations for Shares issued |

|

|

609,099 |

|

|

|

2,843,884 |

|

|

Redemptions for Shares redeemed |

|

|

(490,528 |

) |

|

|

(701,281 |

) |

|

Net increase (decrease) in net assets resulting from capital share transactions |

|

|

118,571 |

|

|

|

2,142,603 |

|

|

Total increase (decrease) in net assets from operations and capital share transactions |

|

|

252,738 |

|

|

|

2,502,396 |

|

|

Net assets |

|

|

|

|

|

|

|

Beginning of period |

|

|

2,249,658 |

|

|

|

0 |

|

(1) |

End of period |

|

$ |

2,502,396 |

|

|

$ |

2,502,396 |

|

|

|

|

|

|

|

|

|

|

Shares issued and redeemed |

|

|

|

|

|

|

|

Shares issued |

|

|

18,100,000 |

|

|

|

93,080,000 |

|

|

Shares redeemed |

|

|

(14,570,000 |

) |

|

|

(20,700,000 |

) |

|

Net increase (decrease) in Shares issued and outstanding |

|

|

3,530,000 |

|

|

|

72,380,000 |

|

|

* No comparative financial statements have been provided as the Trust’s operations commenced on January 10, 2024.

(1) Prior to commencement of operations on January 10, 2024, BAM redeemed the initial seed capital of 4 shares for $200.00, Bitwise Investment Manager, LLC, an affiliate of the Sponsor, purchased 10,010 Shares of the Trust for $500,500 and then subsequently redeemed those shares and the Trust formally revised its NAV per-share from $50.00 per-share to $25.00 per-share.

The accompanying notes are an integral part of the Financial Statements.

Bitwise Bitcoin ETF

Statement of Cash Flows

(Amounts in thousands)

|

|

|

|

|

|

|

For the period

January 10, 2024 (commencement of operations) through September 30, 2024* |

|

|

|

(unaudited) |

|

Cash flow from operating activities |

|

|

|

Net increase (decrease) in net assets resulting from operations |

|

$ |

359,793 |

|

Adjustments to reconcile net increase in net assets resulting from operations to net

cash provided by (used in) operating activities: |

|

|

|

Purchases of bitcoin |

|

|

(2,750,279 |

) |

Proceeds from bitcoin sold |

|

|

609,247 |

|

Net realized (gain) loss from investment in bitcoin transferred to pay Sponsor Fee |

|

|

(593 |

) |

Net realized (gain) loss from investment in bitcoin sold for redemptions |

|

|

73,204 |

|

Net change in unrealized (appreciation) on investment in bitcoin |

|

|

(434,346 |

) |

Increase (Decrease) in Sponsor Fee payable |

|

|

371 |

|

Net cash provided by (used in) operating activities |

|

|

(2,142,603 |

) |

|

|

|

|

Cash flow from financing activities |

|

|

|

Creations for Shares issued |

|

|

2,843,884 |

|

Redemptions for Shares redeemed |

|

|

(701,281 |

) |

Net cash provided by (used in) financing activities |

|

|

2,142,603 |

|

|

|

|

|

Net increase (decrease) in cash |

|

|

— |

|

Cash, beginning of period (1) |

|

|

— |

|

Cash, end of period |

|

$ |

— |

|

|

|

|

|

Supplemental disclosure of noncash operating activities |

|

|

|

Transfer of bitcoin to pay for Sponsor Fee |

|

$ |

1,571 |

|

* No comparative financial statements have been provided as the Trust’s operations commenced on January 10, 2024.

(1) Prior to commencement of operations on January 10, 2024, BAM redeemed the initial seed capital of 4 shares for $200.

The accompanying notes are an integral part of the Financial Statements.

BITWISE Bitcoin ETF

Notes to Financial Statements

September 30, 2024 (Unaudited)

1. Organization

Bitwise Bitcoin ETF (the “Trust”), formerly Bitwise Bitcoin ETP Trust, is an investment trust organized on August 29, 2019, under Delaware law pursuant to a Declaration of Trust and Trust Agreement (the “Trust Agreement”). The Trust’s investment objective is to seek to provide exposure to the value of bitcoin held by the Trust, less the expenses of the Trust’s operations, generally just the sponsor’s management fee. In seeking to achieve its investment objective, the Trust’s sole asset is bitcoin. The Trust is an Exchange Traded Product (“ETP”) that issues common shares of beneficial interest (“Shares”) that are listed on the NYSE Arca, Inc. (the “Exchange”) under the ticker symbol “BITB,” providing investors with an efficient means to obtain market exposure to the price of bitcoin.

Bitwise Investment Advisers, LLC (the “Sponsor”) serves as the Sponsor for the Trust. The Sponsor arranged for the creation of the Trust and is responsible for the ongoing registration of the Shares for their public offering in the U.S. and the listing of Shares on the Exchange. The Sponsor develops a marketing plan for the Trust, prepares marketing materials regarding the Shares, and operates the marketing plan of the Trust on an ongoing basis. The Sponsor also oversees the additional service providers of the Trust and exercises managerial control of the Trust as permitted under the Trust Agreement. The Sponsor has agreed to pay all normal operating expenses of the Trust (except for litigation expenses and other extraordinary expenses) out of the Sponsor’s unitary management fee (the “Sponsor Fee”) and may determine in its sole discretion to assume legal fees and expenses of the Trust in excess of $500,000 per annum. The Sponsor also paid the costs of the Trust’s organization.

Delaware Trust Company acts as the trustee of the Trust (the “Trustee”) for the purpose of creating a Delaware statutory trust in accordance with the Delaware Statutory Trust Act (“DSTA”) which requires that the Trust have at least one trustee with a principal place of business in the State of Delaware.

The Trust purchases and sells bitcoin directly and it creates or redeems its Shares in cash-settled transactions in blocks of 10,000 Shares at the Trust’s net asset value (“NAV”) per-share and only in transactions with financial firms that are authorized to purchase or redeem Shares with the Trust (each, an “Authorized Participant”). An Authorized Participant will deliver, or cause to be delivered, cash to the Trust when it purchases Shares from the Trust, and the Trust will deliver cash to an Authorized Participant, or its designee, when it redeems Shares with the Trust. Authorized Participants, and their customers, may then, in turn, offer Shares to the public at prices that depend on various factors, including the supply and demand for Shares, the value of the Trust’s assets, and market conditions at the time of a transaction. Investors who buy or sell Shares during the day from their broker may do so at a premium or discount relative to the NAV of the Shares.

The Trust's registration statement on Form S-1 relating to its continuous public offering of Shares was declared effective by the U.S. Securities and Exchange Commission on January 10, 2024 and the Shares of the Trust were listed on the Exchange on January 11, 2024.

The statements of assets and liabilities and schedule of investment as of September 30, 2024, and the statements of operations, cash flows, and changes in net assets for the period ended September 30, 2024, have been prepared on behalf of the Trust and are unaudited. In the opinion of management of the Sponsor of the Trust, all adjustments (which include normal recurring adjustments) necessary to present fairly the financial position and results of operations for the period ended September 30, 2024, and for all interim periods presented have been made. In addition, interim period results are not necessarily indicative of results for a full-year period.

Prior to the commencement of operations on January 10, 2024, on November 9, 2023, BAM purchased 4 Shares at a per-share price of $50.00 for $200 in a transaction exempt from registration under Section 4(a)(2) of the 1933 Act (the “Seed Shares”). Delivery of the Seed Shares was made on November 9, 2023. On January 5, 2024, Bitwise Investment Manager, LLC (“BIM”), an affiliate of the Sponsor, purchased 10,010 Shares of the Trust at a per-Share price of $50.00 for $500,500. On January 10, 2024, BAM redeemed the entirety of its 4 Seed Shares for $200 and BIM redeemed the entirety of its 10,010 Shares for $500,500. Following the redemptions, on January 10, 2024, the Trust formally revised its NAV per-share from $50.00 per-share to $25.00 per-share. Additionally, on January 10, 2024, BIM purchased the initial 100,000 Shares of the Trust (the “Seed Baskets”) for $2,500,000, at $25.00 per-share. BIM acted

as a statutory underwriter in connection with the initial purchase of the Seed Baskets. On January 11, 2024, BIM sold all of its 100,000 Shares of the Trust for cash.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the Trust in the preparation of its financial statements.

Basis of presentation

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Trust is an investment company and follows the specialized accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC” or “Codification”) Topic 946, Financial Services—Investment Companies.

Use of Estimates

The preparation of the financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of these financial statements. Actual results could differ from those estimates.

Cash

Generally, the Trust does not intend to hold any cash. Cash includes non-interest bearing non-restricted cash with one institution. Cash in a bank deposit account, at times, may exceed U.S. federally insured limits. The Trust has not experienced any losses in such accounts and does not believe it is exposed to any significant credit risk on such bank deposits. On December 31, 2023, the Trust held $200 in cash relating to the issuance of the Seed Shares.

Investment Transactions and Revenue Recognition

The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as net change in unrealized appreciation or depreciation on investment in bitcoin. Realized gains and losses are calculated using the specific identification method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Sponsor Fee in bitcoin.

Investment Valuation - Principal Market NAV

U.S. GAAP defines fair value as the price the Trust would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. The Trust’s policy is to value investments held at fair value.

For financial statement reporting, the Trust identifies and determines the bitcoin principal market (or in the absence of a principal market, the most advantageous market) for U.S. GAAP purposes consistent with the application of the fair value measurement framework in FASB ASC Topic 820. A principal market is the market with the greatest volume and activity level for the asset or liability. The Principal Market NAV and the Principal Market NAV per-share are calculated using the fair value of bitcoin based on the price provided by this exchange market, as of 4:00 p.m. ET on the measurement date for U.S. GAAP purposes. The Trust determines its principal market (or in the absence of a principal market the most advantageous market) on a quarterly basis to determine which market is its Principal Market for the purpose of calculating fair value for the creation of quarterly and annual financial statements.

Specifically, the Trust utilizes a third-party valuation vendor, Lukka, Inc., to identify publicly available, well established and reputable crypto asset exchanges selected by Lukka, Inc. in their sole discretion, including Binance, Bitfinex, Bitflyer, Bitstamp, Bullish, Coinbase, Crypto.com, Gate.io, Gemini, HitBTC, Huobi, itBit, Kraken, KuCoin, LMAX, MEXC Global, OKX and Poloniex, and then calculating, on each valuation period, the highest volume exchange during the 60 minutes prior to 4:00 p.m. ET for bitcoin. The Sponsor then identifies that market as the principal market for bitcoin during that period, and uses the price for bitcoin from that venue

at 4:00 ET as the principal market price. In evaluating the markets that could be considered principal markets, the Trust considered whether the specific markets were accessible to the Trust, either directly or through an intermediary, at the end of each period.

The Principal Market and the Principal Market Price for bitcoin, which comprised the majority of the Trust’s assets for the three-month period ended September 30, 2024, was Coinbase with a price of $63,464.76 as of September 30, 2024.

Various inputs are used in determining the fair value of assets and liabilities. Inputs may be based on independent market data (“observable inputs”) or they may be internally developed (“unobservable inputs”). These inputs are categorized into a disclosure hierarchy consisting of three broad levels for financial reporting purposes. The level of a value determined for an asset or liability within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement in its entirety. The three levels of the fair value hierarchy are as follows:

Level 1: Unadjusted quoted prices in active markets for identical assets or liabilities;

Level 2: Inputs other than quoted prices included within Level 1 that are observable for the asset or liability either directly or indirectly, including quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not considered to be active, inputs other than quoted prices that are observable for the asset or liability, and inputs that are derived principally from or corroborated by observable market data by correlation or other means; and

Level 3: Unobservable inputs, including the Trust's assumptions used in determining the fair value of investments, where there is little or no market activity for the asset or liability at the measurement date.

The cost basis of the investment in bitcoin recorded by the Trust for financial reporting purposes is the fair value of bitcoin at the time of transfer. The cost basis recorded by the Trust may differ from proceeds collected by the Authorized Participant from the sale of the corresponding Shares to investors.

Given that bitcoin is actively traded and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy. The following summarizes the Trust’s assets accounted for at fair value at September 30, 2024* (amounts in thousands):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

Investment in bitcoin, at fair value |

|

$ |

2,502,767 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

2,502,767 |

|

* No comparative period presented as the Trust commenced operations on January 10, 2024.

Calculation of Net Asset Value (NAV) and NAV Per-Share

On each business day, as soon as practicable after 4:00 p.m. ET, the NAV of the Trust is obtained by subtracting all accrued fees and other liabilities of the Trust from the fair value of the bitcoin and other assets held by the Trust. The Bank of New York Mellon (the “Administrator”) computes the NAV per-share by dividing the NAV of the Trust by the number of Shares outstanding on the date the computation is made.

Income Taxes

The Trust is classified as a “grantor trust” for U.S. federal income tax purposes. As a result, the Trust itself is not subject to U.S. federal income tax. Instead, the Trust’s income and expenses “flow through” to the shareholders, and the Administrator reports the Trust’s income, gains, losses, and deductions to the Internal Revenue Service on that basis. The Sponsor has analyzed applicable tax laws and regulations and their application to the Trust, and does not believe that there are any uncertain tax positions that require recognition of a tax liability as of September 30, 2024.

The Trust is required to determine whether its tax positions are more likely than not to be sustained on examination by the applicable taxing authority, based on the technical merits of the position. Tax positions not deemed to meet a more likely than not threshold would be recorded as a tax expense in the current year. As of September 30, 2024 and December 31, 2023, the Trust has determined that no provision for income taxes is required and no liability for unrecognized tax benefits has been recorded. The Trust does not

expect that its assessment related to unrecognized tax benefits will materially change over the next 12 months. However, the Trust’s conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, the nexus of income among various tax jurisdictions; compliance with U.S. federal, U.S. state, and tax laws of jurisdictions in which the Trust operates in; and changes in the administrative practices and precedents of the relevant authorities. The Trust is required to analyze all open tax years. Open tax years are those years that are open for examination by the relevant income taxing authority. As of September 30, 2024, all tax years since inception remain open for examination. There were no examinations in progress at period end.

Organizational and offering costs

The costs of the Trust’s organization and the initial offering of the Shares are borne directly by the Sponsor. The Trust is not obligated to reimburse the Sponsor.

3. Fair Value of bitcoin

As of September 30, 2024,* the Trust held a net closing balance of 39,435.5408 bitcoin with a total market value of $2,500,633,274 based on the CME CF Bitcoin Reference Rate - New York Variant ("BRRNY") price of $63,410.65, used to determine the Trust's NAV. The total market value of the Trust's bitcoin held was $2,502,767,131 based on the price of bitcoin (Lukka Prime Rate) in the principal market (Coinbase) of $63,464.76, used to determine the Trust's Principal Market NAV.

The following represents the changes in quantity of bitcoin and the respective fair value for the period from January 10, 2024 to September 30, 2024*:

|

|

|

|

|

|

|

|

|

|

|

Quantity of bitcoin |

|

|

Fair Value

(amounts in thousands) |

|

Beginning balance as of January 10, 2024 (commencement of operations) |

|

|

0.0000 |

|

|

$ |

0 |

|

Purchases |

|

|

49,242.3896 |

|

|

|

2,750,279 |

|

Sales for the redemption of Shares |

|

|

(9,781.9044 |

) |

|

|

(607,676 |

) |

Bitcoin transferred for Sponsor Fee |

|

|

(24.9444 |

) |

|

|

(1,571 |

) |

Net realized gain (loss) on investment in bitcoin transferred to pay Sponsor Fee |

|

|

— |

|

|

|

593 |

|

Net realized gain (loss) on investment in bitcoin sold for redemptions |

|

|

— |

|

|

|

(73,204 |

) |

Change in unrealized appreciation (depreciation) on investment in bitcoin |

|

|

— |

|

|

|

434,346 |

|

Ending balance as of September 30, 2024* |

|

|

39,435.5408 |

|

|

$ |

2,502,767 |

|

* No comparative period presented as the Trust commenced operations on January 10, 2024.

4. Related Party Transactions and Agreements

The Trust pays the Sponsor Fee of 0.20% per annum of the Trust’s bitcoin holdings. For the six-month period commencing on January 11, 2024, the day the Shares are initially listed on the Exchange, the Sponsor waived the entire Sponsor Fee on the first $1 billion of Trust assets through July 10, 2024.

The Sponsor Fee is paid by the Trust to the Sponsor as compensation for services performed under the Trust Agreement and Sponsor Agreement. After the period during which all or a portion of the Sponsor Fee was waived, the Sponsor Fee has been accruing daily, since July 11, 2024, and is payable in bitcoin monthly in arrears. The Administrator calculates the Sponsor Fee on a daily basis by applying a 0.20% annualized rate to the Trust’s total bitcoin holdings, and the amount of bitcoin payable in respect of each daily accrual shall be determined by reference to the BRRNY. The NAV of the Trust is reduced each day by the amount of the Sponsor Fee calculated each day. On the last day of each month, an amount of bitcoin will be transferred from the Trust Bitcoin Account to the Sponsor Bitcoin Account equal to the sum of all daily Sponsor Fees accrued for the month in U.S. dollars divided by the BRRNY on the last day of the month. The Trust is not responsible for paying any fees or costs associated with the transfer of bitcoin to the Sponsor. In exchange for the Sponsor Fee, the Sponsor has agreed to assume and pay the normal operating expenses of the Trust, which include the Trustee’s monthly fee and out-of-pocket expenses, the fees of the Trust’s regular service providers (Cash Custodian, Bitcoin Custodian, Prime Execution Agent, Marketing Agent, Transfer Agent and Administrator), exchange listing fees, tax reporting fees, SEC registration fees, printing and mailing costs, audit fees and up to $500,000 per annum in ordinary legal fees and expenses. The Sponsor may determine in its sole discretion to assume legal fees and expenses of the Trust in excess of $500,000 per annum. The Sponsor also agreed to pay the costs of the Trust’s organization.

The Trust may incur certain extraordinary, non-recurring expenses that are not assumed by the Sponsor, including but not limited to, taxes and governmental charges, any applicable brokerage commissions, financing fees, Bitcoin network fees and similar transaction fees, expenses and costs of any extraordinary services performed by the Sponsor (or any other service provider) on behalf of the Trust to protect the Trust or the Shareholders (including, for example, in connection with any fork of the Bitcoin blockchain, any Incidental Rights and any IR Asset, any indemnification of the Cash Custodian, Bitcoin Custodian, Prime Execution Agent, Transfer Agent, Administrator or other agents, service providers or counterparties of the Trust, and extraordinary legal fees and expenses, including any legal fees and expenses incurred in connection with litigation, regulatory enforcement or investigation matters.

See Note 1 for further discussion on related party capital transactions. As of September 30, 2024, the Sponsor owned no Shares of the Trust.

5. Creation and Redemption of Shares

When the Trust creates or redeems its Shares, it does so only in Baskets (blocks of 10,000 Shares) based on the quantity of bitcoin attributable to each Share of the Trust (net of accrued expenses and liabilities) multiplied by the number of Shares comprising a Basket (10,000). This is called the “Basket Amount.”

The Transfer Agent will facilitate the settlement of Shares in response to the placement of creation orders and redemption orders from Authorized Participants. The Trust has entered into the Cash Custody Agreement with BNY Mellon under which BNY Mellon acts as custodian of the Trust’s cash and cash equivalents. The Trust only creates or redeems its Shares at NAV.

Authorized Participants are the only persons that may place orders to create and redeem Baskets. Authorized Participants must be (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, that are not required to register as broker-dealers to engage in securities transactions described below, and (2) DTC Participants. To become an Authorized Participant, a person must enter into an Authorized Participant Agreement. The Authorized Participant Agreement provides the procedures for the creation and redemption of Baskets and for the delivery of the cash or Shares required for such creation and redemptions. The Authorized Participant Agreement and the related procedures attached thereto may be amended by the Trust, without the consent of any Shareholder or Authorized Participant. Authorized Participants must pay the Transfer Agent a non-refundable fee for each order they place to create or redeem one or more Baskets. The transaction fee may be waived, reduced, increased or otherwise changed by the Sponsor in its sole discretion. Authorized Participants who make deposits with the Trust in exchange for Baskets receive no fees, commissions or other form of compensation or inducement of any kind from either the Trust or the Sponsor, and no such person has any obligation or responsibility to the Sponsor or the Trust to effect any sale or resale of Shares.

Each Authorized Participant is required to be registered as a broker-dealer under the Securities Exchange Act of 1934, as amended, and a member in good standing with FINRA, or exempt from being or otherwise not required to be licensed as a broker-dealer or a member of FINRA, and is qualified to act as a broker or dealer in the states or other jurisdictions where the nature of its business so requires. Certain Authorized Participants may also be regulated under federal and state banking laws and regulations. Each Authorized Participant has its own set of rules and procedures, internal controls and information barriers as it determines is appropriate in light of its own regulatory regime.

6. Concentration of Risk

Substantially all the Trust’s assets are holdings of bitcoin, which creates a concentration risk associated with fluctuations in the price of bitcoin. Accordingly, a decline in the price of bitcoin will have an adverse effect on the value of the Shares of the Trust. The trading prices of bitcoin have experienced extreme volatility in recent periods and may continue to fluctuate significantly. Extreme volatility in the future, including substantial, sustained, or rapid declines in the trading prices of bitcoin, could have a material adverse effect on the value of the Shares and the Shares could lose all or substantially all of their value. Factors adversely impacting the value of bitcoin and the Shares may include an increase in the global bitcoin supply or a decrease in global bitcoin demand; market conditions of, and overall sentiment towards, the crypto assets and blockchain technology industry; trading activity on crypto asset exchanges, which, in many cases, are largely unregulated or may be subject to manipulation; the adoption of bitcoin as a medium of exchange, store-of-value or other consumptive asset and the maintenance and development of the open-source software protocol of the bitcoin network, and their ability to meet user demands; manipulative trading activity on crypto asset exchanges, which, in many cases, are largely unregulated; and forks in the bitcoin network, among other things.

Coinbase Custody Trust Company, LLC serves as the Trust’s custodian for bitcoin for which qualified custody is available (the “Bitcoin Custodian”). The Bitcoin Custodian is subject to change in the sole discretion of the Sponsor. At September 30, 2024, bitcoin

with a market value of $2,502,767,131 was held by the Bitcoin Custodian. No comparative period presented as the Trust commenced operations on January 10, 2024.

7. Financial Highlights*

Per-share Performance (for a Share outstanding throughout the periods presented)

|

|

|

|

|

|

|

|

|

|

|

|

Three months ended September 30, 2024 |

|

|

For the period

January 10, 2024 (commencement of operations) through September 30, 2024* |

|

|

Net asset value per-share, beginning of period |

|

$ |

32.67 |

|

|

$ |

25.00 |

|

|

Net investment loss 1 |

|

|

(0.02 |

) |

|

|

(0.03 |

) |

|

Net realized unrealized gain (loss) 2 |

|

|

1.92 |

|

|

|

9.60 |

|

|

Net change in net assets from operations |

|

|

1.90 |

|

|

|

9.57 |

|

|

Net asset value per-share, end of period |

|

$ |

34.57 |

|

|

$ |

34.57 |

|

|

|

|

|

|

|

|

|

|

Total return, at net asset value 2 |

|

|

5.82 |

|

% |

|

38.28 |

|

% |

|

|

|

|

|

|

|

|

Ratios to average net assets 3 |

|

|

|

|

|

|

|

Net investment loss |

|

|

(0.19 |

) |

% |

|

(0.14 |

) |

% |

Gross expenses |

|

|

0.20 |

|

% |

|

0.20 |

|

% |

Net expenses |

|

|

0.19 |

|

% |

|

0.14 |

|

% |

* No comparative financial statements have been presented as the Trust's operations commenced on January 10, 2024.

1.Calculated using average Shares outstanding.

2.Total returns are calculated based on the change in value during the reporting period. An individual shareholder’s total return and ratio may vary from the above total returns and ratios based on the timing of share transactions from the Trust.

8. Recently Issued Accounting Pronouncements

In December 2023, the FASB issued Accounting Standards Update (“ASU”) 2023-08, Intangibles—Goodwill and Other—Crypto Assets (Subtopic 350-60): Accounting for and Disclosure of Crypto Assets (“ASU 2023-08”). ASU 2023-08 is intended to improve the accounting for certain crypto assets by requiring an entity to measure those crypto assets at fair value each reporting period with changes in fair value recognized in net income. The amendments also improve the information provided to investors about an entity’s crypto asset holdings by requiring disclosure about significant holdings, contractual sale restrictions, and changes during the reporting period. ASU 2023-08 is effective for annual and interim reporting periods beginning after December 15, 2024. Early adoption is permitted for both interim and annual financial statements that have not yet been issued. The Trust adopted this new guidance with no material impact on its financial statements and disclosures as the Trust uses fair value as its method of accounting for Bitcoin in accordance with its classification as an investment company for accounting purposes.

9. Indemnifications

In the normal course of business, the Trust enters into contracts and agreements that contain a variety of representations and warranties and which provide general indemnifications. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred. The Trust expects the risk of any future obligation under these indemnifications to be remote.

10. Subsequent Events

In preparing these financial statements, the Sponsor has evaluated events and transactions for potential recognition or disclosure through the date these financial statements were issued. Management has determined that there were no additional material events that would require disclosure other than that which has already been discussed in these Notes to Financial Statements.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read together with, and is qualified in its entirety by reference to, our unaudited financial statements and related notes included elsewhere in this Quarterly Report, which have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). The following discussion may contain forward-looking statements based on assumptions we believe to be reasonable. Our actual results could differ materially from those discussed in these forward-looking statements.

Trust Overview

Bitwise Bitcoin ETF (the “Trust”) is a Delaware statutory trust formed on August 29, 2019. The Trust continuously issues common shares (“Shares”), representing units of undivided beneficial ownership of the Trust. The Shares are listed on the NYSE Arca Inc. (the “Exchange”) under the ticker symbol “BITB.” The Trust’s commencement of operations was January 10, 2024. Bitwise Investment Advisers, LLC (the “Sponsor”) serves as the sponsor of the Trust.

The Trust’s investment objective is to seek to provide shareholders of the Trust (“Shareholders”) with exposure to the value of bitcoin held by the Trust that is reflective of the actual bitcoin market in which investors can purchase or sell bitcoin, less the expenses of the Trust’s operations and other liabilities. In seeking to achieve its investment objective, the Trust holds bitcoin and establishes its net asset value (“NAV") by reference to the CME CF Bitcoin Reference Rate - New York Variant (“BRRNY”). The BRRNY was designed to provide a daily, 4:00 p.m. ET reference rate of the U.S. dollar price of one bitcoin and is calculated by CF Benchmarks Ltd. (the “Benchmark Provider”) based on an aggregation of executed trade flow of major bitcoin trading platforms (“Constituent Platforms”).

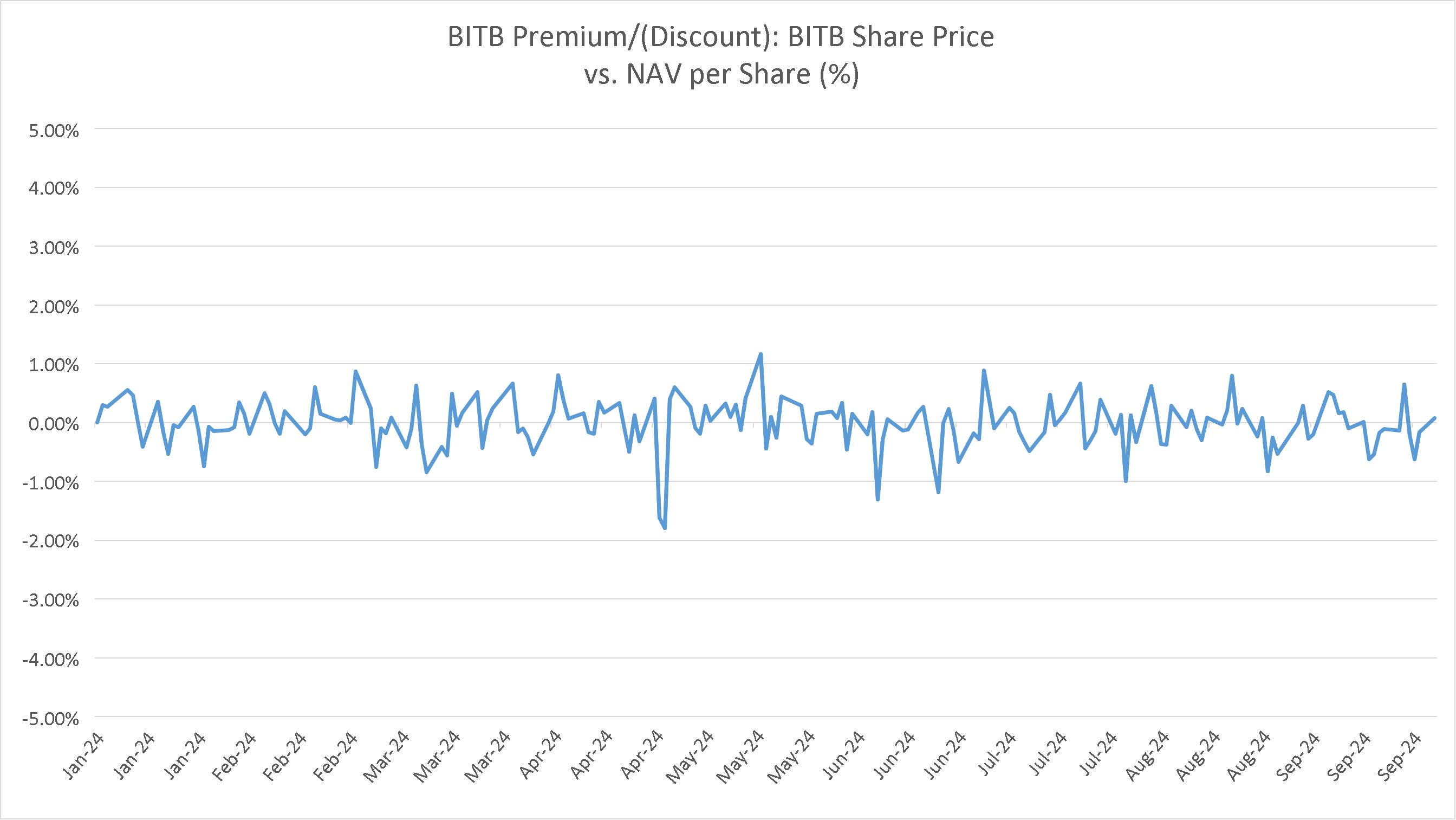

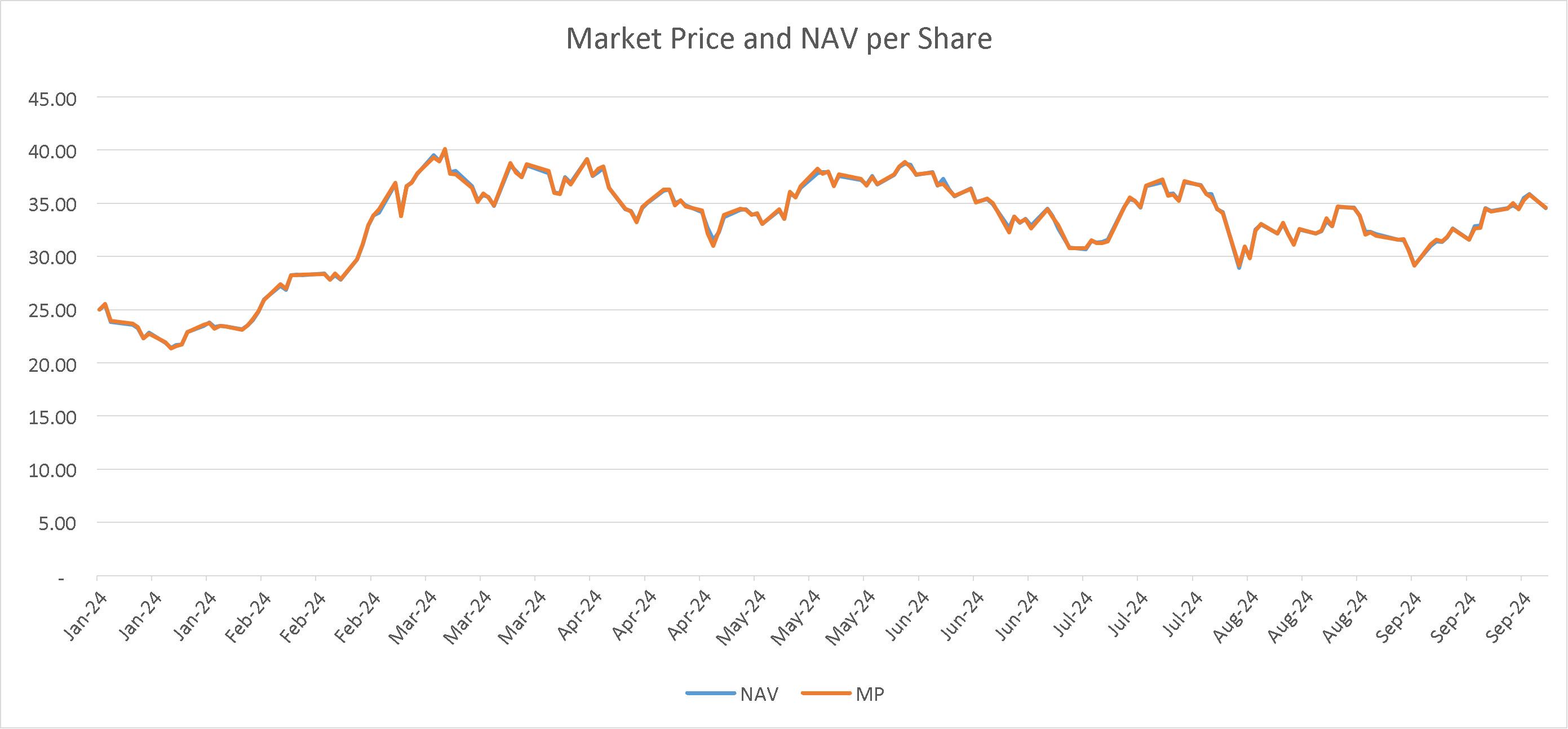

The Shares may trade at a premium over, or a discount to, the NAV per-share as a result of price volatility, trading volume and closings of the exchanges on which the Sponsor purchases bitcoins on behalf of the Trust due to fraud, failure, security breaches or otherwise, and the fact that supply and demand forces at work in the secondary trading market for Shares are related, but not identical, to the supply and demand forces influencing the market price of bitcoin. As a result of the foregoing, the price of the Shares as quoted on the Exchange has varied from the value of the Trust’s NAV per-share since the Shares were approved for quotation on January 11, 2024.

The following charts show the percentage of Premium/(Discount) of the Shares as quoted on the Exchange and the Trust’s NAV and a comparison of the NAV of the Trust vs the market price as quoted on the Exchange.

From January 11, 2024 to September 30, 2024, the Shares of the Trust traded at an average discount, based on closing prices at 4:00 p.m. ET, and estimated, unaudited, NAV per-share of 0.02%. During that same period, the highest premium was 1.17% on May 20, 2024, and the lowest premium was 0.01% on January 18, 2024. During that same period, the highest discount was 1.79% on May 1, 2024, and the lowest discount was 0.002% on June 25, 2024.

The following chart shows the price of bitcoin for the period January 1, 2023 through September 30, 2024, as quoted by the Benchmark Provider, using the BRRNY.

Results of Operations

As of September 30, 2024,* the Trust held a net closing balance of 39,435.5408 bitcoin with a total market value of $2,500,633,274 based on the BRRNY price of $63,410.65, used to determine the Trust's NAV. The total market value of the Trust's bitcoin held was $2,502,767,131 based on the price of bitcoin (Lukka Prime Rate) in the principal market (Coinbase) of $63,464.76, used to determine the Trust's Principal Market NAV.

* No comparative period presented as the Trust commenced operations on January 10, 2024.

For the Three Months Ended September 30, 2024*^

Net realized and unrealized gain on investment in bitcoin for the three months ended September 30, 2024, was approximately $135,282 which includes a realized gain of $359 on the sale of bitcoins to pay the Sponsor Fee, net realized loss on investment in bitcoin sold for redemptions of $49,002 and net change in unrealized appreciation on investment in bitcoin of approximately $183,925. Net realized and unrealized gain on investment in bitcoin for the period was driven by bitcoin price appreciation from $60,330.17 per bitcoin as of June 30, 2024 to $63,410.65 per bitcoin as of September 30, 2024. Net increase in net assets resulting from operations was approximately $134,167 for the three months ended September 30, 2024, which consisted of the net realized and unrealized gain on investment in bitcoin of $135,282, offset by the Sponsor Fee of $1,115. Net assets increased to approximately $2,502,396 on September 30, 2024, a 5.82% increase in NAV for the period. The increase in net assets primarily resulted from the aforementioned bitcoin price appreciation, net capital share transactions of approximately $118,571, and a net increase resulting from operations of $134,167.

For the Period from January 10, 2024 (Commencement of Operations) to September 30, 2024*^

Net realized and unrealized gain on investment in bitcoin for the period from January 10, 2024 to September 30, 2024, was approximately $361,735 which includes a realized gain of $593 on the sale of bitcoins to pay the Sponsor Fee, net realized loss on investment in bitcoin sold for redemptions of $73,204 and net change in unrealized appreciation on investment in bitcoin of approximately $434,346. Net realized and unrealized gain on investment in bitcoin for the period was driven by bitcoin price appreciation from $45,852.66 per bitcoin

as of January 10, 2024 to $63,410.65 per bitcoin as of September 30, 2024. Net increase in net assets resulting from operations was approximately $359,793 for the period from January 10, 2024 to September 30, 2024, which consisted of the net realized and unrealized gain on investment in bitcoin of $361,735, less the Sponsor Fee of $1,942. Net assets increased to approximately $2,502,396 on September 30, 2024, a 38.28% increase in NAV for the period. The increase in net assets primarily resulted from the aforementioned bitcoin price appreciation, net capital share transactions of approximately $2,142,603, and a net increase resulting from operations of $359,793.

* No full nine-month period or comparative period presented as the Trust commenced operations on January 10, 2024.

^ Amounts displayed are in the '000s, except for per-share/coin references

Liquidity and Capital Resources

The Trust agreed to pay the unitary Sponsor Fee of 0.20% per annum of the Trust’s bitcoin holdings. The Sponsor contractually waived the Sponsor Fee on the first $1 billion of Trust assets through July 10, 2024, and has been accruing at an annual rate of 0.20% of the Trust’s net assets since then. As a result, the only ordinary expense of the Trust is expected to be the Sponsor Fee. In exchange for the Sponsor Fee, the Sponsor has agreed to assume and pay the normal operating expenses of the Trust, which include the Trustee’s monthly fee and out-of-pocket expenses, the fees of the Trust’s regular service providers (Cash Custodian, Bitcoin Custodian, Prime Execution Agent, Marketing Agent, Transfer Agent and Administrator), exchange listing fees, tax reporting fees, SEC registration fees, printing and mailing costs, audit fees and up to $500,000 per annum in ordinary legal fees and expenses. The Sponsor may determine in its sole discretion to assume legal fees and expenses of the Trust in excess of $500,000 per annum. The Sponsor also agreed to pay the costs of the Trust’s organization.

The Trust may incur certain extraordinary, non-recurring expenses that are not assumed by the Sponsor, including but not limited to, taxes and governmental charges, any applicable brokerage commissions, financing fees, Bitcoin network fees and similar transaction fees, expenses and costs of any extraordinary services performed by the Sponsor (or any other service provider) on behalf of the Trust to protect the Trust or the Shareholders (including, for example, in connection with any fork of the Bitcoin blockchain, any Incidental Rights and any IR Asset), any indemnification of the Cash Custodian, Bitcoin Custodian, Prime Execution Agent, Transfer Agent, Administrator or other agents, service providers or counterparties of the Trust, and extraordinary legal fees and expenses, including any legal fees and expenses incurred in connection with litigation, regulatory enforcement or investigation matters.

The Trust does not hold a cash balance except in connection with the creation and redemption of Baskets (blocks of 10,000 Shares) or to pay expenses not assumed by the Sponsor. To pay for expenses not assumed by the Sponsor that are denominated in U.S. dollars, the Sponsor, on behalf of the Trust, may sell the Trust’s bitcoin as necessary to pay such expenses. The cash proceeds of the sale will be sent to the Sponsor to pay the expenses. Any remaining cash will be distributed back to the Cash Custodian. The Sponsor expects that the Trust will have an immaterial amount of cash flow from its operations and that its cash balance will be insignificant at the end of each reporting period. The Trust’s only sources of cash are proceeds from the sale of Baskets and bitcoin. The Trust will not borrow to meet liquidity needs.

The Trust is not aware of any trends, demands, conditions or events that are reasonably likely to result in material changes to its liquidity needs.

Off-Balance Sheet Arrangements and Contractual Obligations

As of December 31, 2023, the Trust has not used, nor does it expect to use in the future, special purpose entities to facilitate off-balance sheet financing arrangements and have no loan guarantee arrangements or off-balance sheet arrangements of any kind other than agreements entered into in the normal course of business, which may include indemnification provisions related to certain risks service providers undertake in performing services which are in the best interests of the Trust. While the Trust’s exposure under such indemnification provisions cannot be estimated, these general business indemnifications are not expected to have a material impact on a Trust’s financial position.

Sponsor Fee payments made to the Sponsor are calculated as a fixed percentage of the Trust’s NAV. As such, the Sponsor cannot anticipate the payment amounts that will be required under these arrangements for future periods as NAVs are not known until a future date.

No material changes have occurred during the period ended September 30, 2024.

Critical Accounting Policies

Principal Market and Fair Value Determination

The Trust’s periodic financial statements are prepared in accordance with the Financial Accounting Standards Board Accounting Standards Codification Topic 820, “Fair Value Measurements and Disclosures” (“ASC Topic 820”) and utilize an exchange-traded price from the Trust’s principal market for bitcoin on the Trust’s financial statement measurement date. The Sponsor determines in its sole discretion the valuation sources and policies used to prepare the Trust’s financial statements in accordance with U.S. GAAP. The Trust has engaged a third-party vendor to obtain a price from a principal market for bitcoin, which will be either the market the Trust normally transacts in for bitcoin or, if the Trust does not normally transact in any market or such market suffers an operational interruption and is unavailable, determined and designated by such third-party vendor daily based on its consideration of several exchange characteristics, including oversight, and the volume and frequency of trades. Under U.S. GAAP, such a price is expected to be deemed a Level 1 input in accordance with the ASC Topic 820 because it is expected to be a quoted price in active markets for identical assets or liabilities.

Investment Company Considerations

The Trust is an investment company for U.S. GAAP purposes and follows accounting and reporting guidance in accordance with the FASB ASC Topic 946, Financial Services – Investment Companies. The Trust uses fair value as its method of accounting for bitcoin in accordance with its classification as an investment company for accounting purposes. The Trust is not a registered investment company under the Investment Company Act of 1940. U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates and these differences could be material.

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

As a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934, as amended, the Trust is not required to provide the information required by this item.

Item 4. Controls and Procedures.

Disclosure Controls and Procedures

The Trust maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in its Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in the SEC rules and forms, and that such information is accumulated and communicated to the Principal Executive Officer and Principal Financial Officer of the Sponsor performing functions equivalent to those a principal executive officer and principal financial officer of the Trust would perform if the Trust had any officers, as appropriate to allow timely decisions regarding required disclosure.

Under the supervision and with the participation of the Principal Executive Officer and the Principal Financial Officer of the Sponsor, the Sponsor conducted an evaluation of the Trusts disclosure controls and procedures, as defined under Exchange Act Rule 13a-15(e). Based on this evaluation, the Principal Executive Officer and the Principal Financial Officer of the Sponsor concluded that, as of September 30, 2024, the Trust’s disclosure controls and procedures were effective.

There are inherent limitations to the effectiveness of any system of disclosure controls and procedures, including the possibility of human error and the circumvention or overriding of the controls and procedures.

Changes in Internal Control over Financial Reporting

There were no changes in the Trust’s internal control over financial reporting that occurred during the quarter ended September 30, 2024, that have materially affected, or are reasonably likely to materially affect, the Trust’s internal control over financial reporting.

PART II – OTHER INFORMATION:

Item 1. Legal Proceedings

None.

Item 1A. Risk Factors

As a smaller reporting company, the Trust is not required to provide the information required by this item.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

c)The Trust does not purchase Shares directly from its Shareholders. In connection with its redemption of Baskets held by Authorized Participants, the Trust redeemed 1,457 Baskets (comprising 14,570,000 Shares) during the period from July 22, 2024 (commencement of operations) to September 30, 2024. The following table summarizes the redemptions by Authorized Participants during the period:

|

|

|

|

|

|

|

|

|

Period |

|

Total Shares Redeemed |

|

|

Average Price Per Share |

|

July 1, 2024 – July 31, 2024 |

|

|

4,590,000 |

|

|

$ |

35.89 |

|

August 1, 2024 – August 31, 2024 |

|

|

6,240,000 |

|

|

$ |

33.04 |

|

September 1, 2024 – September 30, 2024 |

|

|

3,740,000 |

|

|

$ |

31.99 |

|

Item 3. Defaults Upon Senior Securities

None.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Other Information

No executive officers or directors of the Sponsor have adopted, modified, or terminated trading plans under either a “Rule 10b5-1 trading arrangement” or "non-Rule 10b5-1 trading arrangement" (as such terms defined in Item 408 of Regulation S-K of the 1933 Act) for the three-month period ended September 30, 2024.

Asset Purchase Transactions

As previously disclosed in the Trust’s Current Report on Form 8-K filed with the SEC on August 30, 2024, the Trust, the Sponsor, Osprey Bitcoin Trust (the “Osprey Trust”) and Osprey Funds, LLC, the sponsor of the Osprey Trust, entered into an Asset Purchase and Contribution Agreement (the “Asset Purchase Agreement”), pursuant to which the Osprey Fund will sell and the Trust will purchase all of the bitcoin owned by the Osprey Fund (the “Acquired Bitcoin”), and the Trust will issue an amount of Shares (the “Consideration Shares”) with a combined NAV equal to the value of the Acquired Bitcoin as determined by reference to the BRRNY (the “Asset Purchase”).

Consummation of the Asset Purchase is subject to the satisfaction or waiver of closing conditions that are contained in the Asset Purchase Agreement. These include, among others, (i) the effectiveness of the registration statement on Form S-1 the Trust filed with the SEC on October 8, 2024; (ii) Osprey Trust’s adoption of a Plan of Dissolution and Liquidation that provides for the dissolution and liquidation of the Osprey Trust following the sale of the Acquired Bitcoin to the Trust (the “Liquidating Distributions”); (iii) the receipt of a legal opinion regarding the tax-free nature of the Asset Purchase and the Liquidating Distributions; (iv) the receipt of approval for listing and trading the Consideration Shares on the Exchange; and (v) other customary conditions.

The Trust and the Sponsor expect the Asset Purchase to close in the fourth quarter of 2024.

Item 6. Exhibits.

Listed below are the exhibits, which are filed as part of this quarterly report on Form 10‑Q (according to the number assigned to them in Item 601 of Regulation S-K of the 1933 Act):

* These exhibits are furnished with this Quarterly Report on Form 10-Q and are not deemed filed with the SEC and are not incorporated by reference in any filing of Bitwise Bitcoin ETF under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, whether made before or after the date hereof, and irrespective of any general incorporation language contained in such filings.

GLOSSARY OF DEFINED TERMS

The following terms may be used throughout this Quarterly Report, including the consolidated financial statements and related notes.

1933 Act: The Securities Act of 1933.

Administrator: BNY Mellon.

Advisers Act: The Investment Advisers Act of 1940.

Agent Execution Model: The model whereby the Prime Execution Agent, acting in an agency capacity, conducts bitcoin purchases and sales on behalf of the Trust with third parties through its Coinbase Prime service pursuant to the Prime Execution Agreement.

Authorized Participant: One that purchases or redeems Baskets from or to the Trust.

BAM: Bitwise Asset Management, Inc., the parent company of the Sponsor.

Basket: A block of 10,000 Shares used by the Trust to issue or redeem Shares.

Basket Amount: The quantity of bitcoin attributable to each Share of the Trust (net of accrued but unpaid expenses and liabilities) multiplied by the number of Shares comprising a Basket (10,000)

Benchmark Provider: CF Benchmarks Ltd.

bitcoin (lowercase): The native unit of account and medium of exchange on the Bitcoin network.

Bitcoin (uppercase): The software protocol and peer-to-peer network used for the creation, transfer and possession of bitcoin, as recorded on the Bitcoin blockchain.

Bitcoin Custodian: Coinbase Custody Trust Company, LLC, a New York New York State limited liability trust company.

Bitcoin Custody Agreement: The custody agreement between the Bitcoin Custodian and the Trust pursuant to which the Trust Bitcoin Agreement is established.

Bitcoin Trading Counterparty: The bitcoin trading counterparties that have been approved by the Sponsor.

Bitlicense: The license required by NYSDFS for virtual currency business activity conducted in New York State. The term often is used to describe the regulations promulgated under the New York Banking Law that authorize such licensing process.

BNY Mellon: The Bank of New York Mellon, a national association bank in New York that serves as the Administrator and Transfer Agent.

BRR: CME CF Bitcoin Reference Rate.

BRRNY: CME CF Bitcoin Reference Rate - New York Variant, calculated by CF Benchmarks Ltd.and published by the CME Group, is the CF Bitcoin-Dollar US Settlement Price that determines the U.S. dollar price of one bitcoin as of 4:00 p.m. ET daily, based on aggregated executed trade flows from major bitcoin trading platforms.

Business Day: Any day other than a day when the Exchange or the New York Stock Exchange is closed for regular trading.

Cash Custodian: BNY Mellon.

Commodity Exchange Act: Commodity Exchange Act of 1936.

CFTC: Commodity Futures Trading Commission, an independent agency with the mandate to regulate commodity futures and options in the U.S.

CME: The Chicago Mercantile Exchange.

CME Bitcoin Real Time Price: The CME CF Bitcoin Real Time Index, a pricing index continuously published by the CME Group at one second intervals that calculates the U.S. dollar price of one bitcoin on constituent crypto asset trading platforms.

Code: Internal Revenue Code of 1986.

Constituent Platform: The major bitcoin trading platforms that serve as the pricing sources for the calculation of the CME CF Bitcoin Reference Rate – New York Variant and CME CF Bitcoin Real Time Index.

Cryptocurrency: A token such as bitcoin that is the native asset of a crypto asset network.

Crypto asset: A token, such as a cryptocurrency, that is the native asset of or issued on a digital asset network and secured using public private key cryptography or similar cryptographic credentials.

DTC: The Depository Trust Company, the securities depository for the Shares.

DTC Participant: An entity that has an account with DTC.

DSTA: Delaware Statutory Trust Act.

ERISA: Employee Retirement Income Security Act of 1974.