A Base Metal No

More….

+

The

fears about

Cobalt's viability in Lithium Ion Batteries were long only

price-oriented but now the most crucial fear is on strategic access

grounds

+

Increased

Manganese weighting in new LiB formulations is driving a refocusing

on the potential of this metal

+

Manganese in not

problematical due to its image of being "cheap" and "not difficult"

on the supply-side. These are in fact its

two main virtues

+

The wild

gyrations in Vanadium's price has made Manganese look like a

tempting option to replace, in part, Vanadium in Redox Flow Batteries for mass

storage

+

Lack of Manganese

production or resources in North America, makes the few deposits

that exist, interesting as crucial assets in the hunt for

non-Chinese supply chains for LiBs

-

Cobalt is down, but not out for

the count, as a Lithium Ion Battery component

-

There is a

perception that Manganese (somewhat like Nickel) is prolific and

thus "nothing to worry about"

Manganese –

The Road Less Travelled in Battery Metals

The pace of

change in the battery space has shifted up a few gears since

a small

group of

developers moved into the Manganese space in

2016/7. Lithium plays first

proliferated (and then came tumbling back to earth) and then Cobalt

became the word on everyone's lips as the Cobalt crisis moved into

centre stage and focusing minds on supply issues in the battery

space. Manganese was regarded as the

worry-free component of the Lithium Ion Battery formulations,

however this ignored the fact that there is almost no production of

the metal in North America.

Now, however, the

metal is

receiving increasing attention for its potential to reduce the

Cobalt component in various battery types using that metal via the

rebalancing of the relative weightings of elements in the battery

cathode formulations, particularly Nickel/Cobalt/Manganese in NMC

batteries.

A Blizzard

of Technologies

Battery

technologies have been proliferating in recent years like mushrooms

after the rain. Most of the buzz in the mainstream media is about

battery options that extend the life of cellphones or laptops and

other PDAs or with regard to hybrid- or all-electric vehicles.

However, the really great economic

leap forward has to do with mass storage devices which mesh with

energy grids to provide off-peak storage of electricity. Industrial

or natural gas has been stored since its inception in the

industrial revolution in massive tanks, caverns or gasometers,

while a solution to massive electricity storage has been much more

elusive. With conventional dry-cell battery using two electrodes

separated by an electrolyte, it would require thousands of

individual cells, the size of soft drink cans, to be strung

together in a massive installation to create a mass storage battery

of any usefulness to be attached the grid.

The relevance of

this has been heightened with the burgeoning of alternative energy

sources (wind and solar) that are irregular in their generating

periods and do not always coincide with peak demand.

While Elon Musk

muses on giving his auto-batteries a life-after-death as

Powerwalls, the real mass storage device catching

attention is Redox Flow Batteries (RFBs), with Vanadium (hitherto)

being the main beneficiary

of investor

enthusiasm. However, this has overlooked the different ways in which

Manganese can be mobilized for battery and mass storage

technologies.

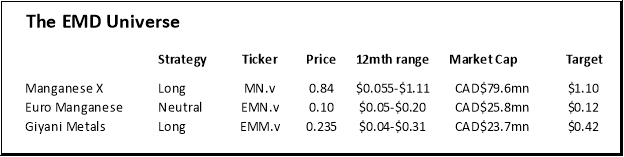

A Case

Study: Manganese X Energy

Like many other

companies, Manganese X (TSX-V:MN,

OTC: MNXXF) was launched upon the tide of

the second Battery Wave in the middle years of the last decade.

Many of the other names, particularly in Cobalt and Lithium ended

up grounded, on the rocks or sunk.

Though financing

was almost non-existent across the swathe of battery metal juniors,

the management at Manganese X Energy battened down the hatches and

stayed the course. Now that a certain confidence has returned to

the broader mining markets it has had a firming effect on even the

battery metals. However, the emphasis has shifted.

Lithium still remains central to the LiB story

but

cobalt has fallen

into deep disdain.

The market cap

is

up, and financing more

available, enhanced potential to finally kick up

the resource calculation, potential mine development and moreover

implementation of a demonstration plant prompt us to

maintain a

LONG

stance on

Manganese X Energy with a 12-month target price of

$1.10.

Conclusion

The issue

at the root of

all this though is the availability of

metal supplies. Lithium seemingly has a supply situation with

little in the way of constraints for a long way out.

Cobalt though is

relatively scarce, moreover with the Chinese having cornered the

supply, as least as it pertains to the largest producer, the

DRC. With no current supplies of

Manganese in the US or Canada,

and battery-grade

Manganese

processing capacity

under

Chinese

control, the US ambitions in the EV

space are essentially at the mercy of China.

The US is reduced

to the status of a Manganese scavenger unless it has access to not

only non-Chinese sources of ore, but also, and more

importantly regional Manganese

Sulphate

(MnSO4)

sources.

With the

strategic stockpile starting to have EMM added

again, for the first time since

2004, there is clearly rising concern in Washington.

It needs a

complete North American supply chain.

Combined the rise

of EVs and the possibility of Manganese muscling in on Vanadium's

turf in the VRB space and the developers in the EMM

(mining) space are few and far between. Increasingly the hunt for

enhanced economics in EV production will mean that cheaper, more

secure and more efficient battery formulations will be required and

Manganese might well be the secret sauce to make EV economics more

palatable to the mass market.

Sector Review

Christopher

Ecclestone

See complete

research report at:

http://hallgartenco.com/pdf/Battery/Manganese_Batteries_Sept2020.pdf

©

2020 Hallgarten & Company,

Ltd. All rights

reserved.