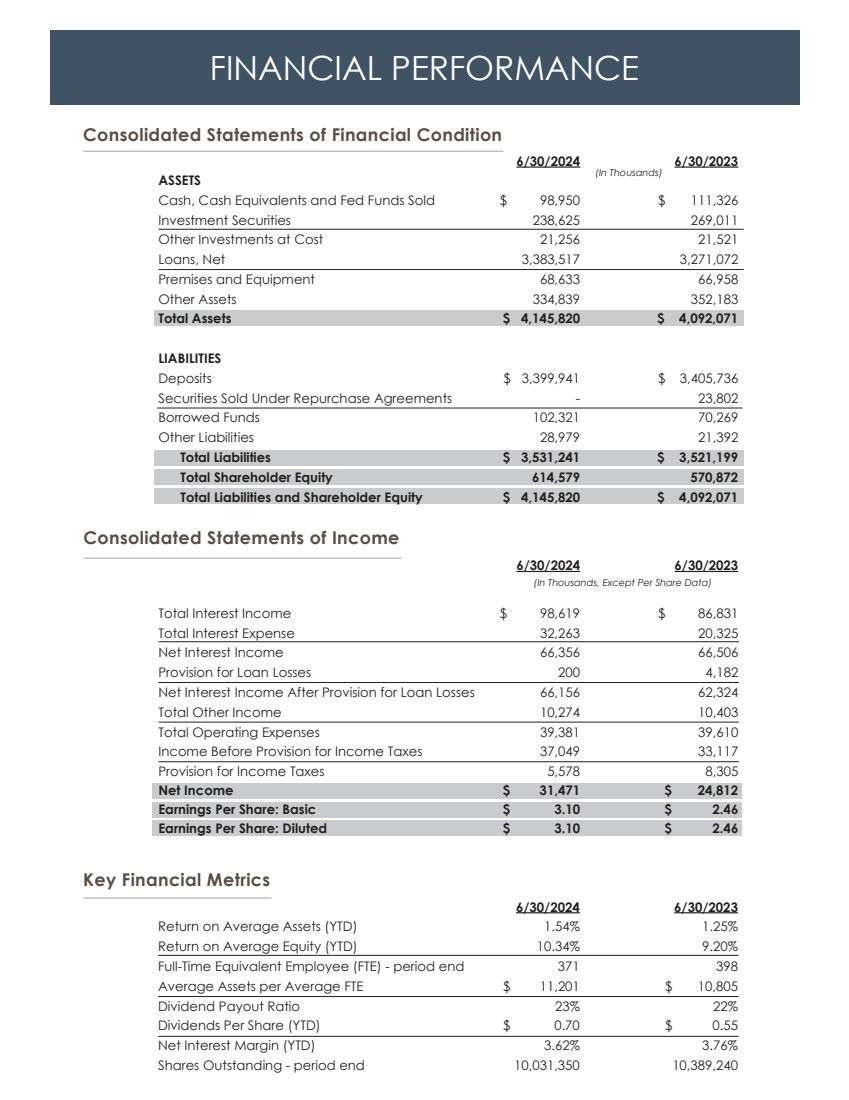

| FINANCIAL PERFORMANCE

6/30/2024 6/30/2023

Return on Average Assets (YTD) 1.54% 1.25%

Return on Average Equity (YTD) 10.34% 9.20%

Full-Time Equivalent Employee (FTE) - period end 371 398

Average Assets per Average FTE $ 11,201 $ 10,805

Dividend Payout Ratio 23% 22%

Dividends Per Share (YTD) $ 0.70 $ 0.55

Net Interest Margin (YTD) 3.62% 3.76%

Shares Outstanding - period end 10,031,350 10,389,240

6/30/2024 6/30/2023

ASSETS

Cash, Cash Equivalents and Fed Funds Sold $ 98,950 $ 111,326

Investment Securities 238,625 269,011

Other Investments at Cost 21,256 21,521

Loans, Net 3,383,517 3,271,072

Premises and Equipment 68,633 66,958

Other Assets 334,839 352,183

Total Assets $ 4,145,820 $ 4,092,071

LIABILITIES

Deposits $ 3,399,941 $ 3,405,736

Securities Sold Under Repurchase Agreements - 23,802

Borrowed Funds 102,321 70,269

Other Liabilities 28,979 21,392

Total Liabilities $ 3,531,241 $ 3,521,199

Total Shareholder Equity 614,579 570,872

Total Liabilities and Shareholder Equity $ 4,145,820 $ 4,092,071

6/30/2024 6/30/2023

Total Interest Income $ 98,619 $ 86,831

Total Interest Expense 32,263 20,325

Net Interest Income 66,356 66,506

Provision for Loan Losses 200 4,182

Net Interest Income After Provision for Loan Losses 66,156 62,324

Total Other Income 10,274 10,403

Total Operating Expenses 39,381 39,610

Income Before Provision for Income Taxes 37,049 33,117

Provision for Income Taxes 5,578 8,305

Net Income $ 31,471 $ 24,812

Earnings Per Share: Basic $ 3.10 $ 2.46

Earnings Per Share: Diluted $ 3.10 $ 2.46

Consolidated Statements of Financial Condition

Key Financial Metrics

Consolidated Statements of Income

(In Thousands)

(In Thousands, Except Per Share Data) |