SECURITIES AND EXCHANGE COMMISSION

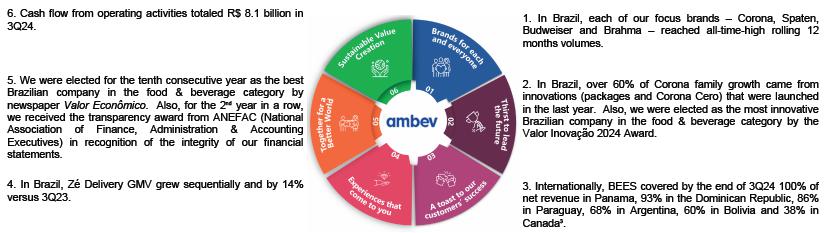

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange Act of 1934

For the month of October, 2024

Commission File Number 1565025

AMBEV S.A.

(Exact name of registrant as specified in its

charter)

AMBEV S.A.

(Translation of Registrant's name into English)

Rua Dr. Renato Paes de Barros, 1017 - 3rd

Floor

04530-000 São Paulo, SP

Federative Republic of Brazil

(Address of principal executive office)

Indicate by check mark whether the

registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form 40-F _______

Indicate

by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information

to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes _______ No ___X____

Page | 1

|

|

| |

|

AMBEV REPORTS 2024 THIRD QUARTER RESULTS[1]

“Our commercial performance delivered consistent top line growth,

and Normalized EBITDA grew by high-single digits with margins expanding once again.” – Jean Jereissati, CEO

| |

|

|

|

|

Total Volume (organic) |

|

Net Revenue (organic)

|

-0.6% vs LY |

|

|

+4.9% vs LY |

|

|

Consolidated volumes declined

by 0.6% (ex- Argentina, 1.3% growth). Brazil volumes grew 1.3% (+0.6% in Beer and +3.4% in NAB).

In Central America and the Caribbean (“CAC”) volumes declined by 0.5%, with Dominican Republic volumes up mid-single digits.

And soft industries in Argentina and Canada led to volume declines in Latin America South (“LAS”)

(-7.7%) and Canada (-1.4%).

|

|

Top line performance was driven

by net revenue per hectoliter (“NR/hl”) growth of 5.5%. Net revenue grew in all our

reporting segments: Brazil NAB +14.8%, LAS[2]

+6.9%, CAC +4.7%, Brazil Beer +3.5% and

Canada +0.1%.

|

| |

|

|

|

|

| |

|

|

|

|

Normalized EBITDA (organic)

|

|

Normalized Profit

|

+8.5% vs LY

|

|

|

R$ 3,579.6 million

|

|

Normalized

EBITDA growth was driven by CAC (+17.7%), LAS (+9.0%)

and Brazil (+7.8%, with NAB +21.7% and Beer +5.8%),

with a flat performance in Canada (0.0%). Gross margin expanded 180 bps to 50.3%, while Normalized

EBITDA margin expanded 110 bps

to 32.0%.

|

|

Normalized Profit declined by

11.4% compared to R$ 4,038.9 million in 3Q23, as increased income tax expenses in Brazil more

than offset Normalized EBITDA growth and better net finance results.

|

| |

|

|

|

|

| |

|

|

|

|

Cash flow from operating activities

|

|

Capital Allocation

|

R$ 8,108.4 million

|

|

|

|

|

Cash flow from operating activities

increased by 2.3% compared to R$ 7,923.0 million in 3Q23, mostly due to Normalized EBITDA growth

coupled with better working capital.

|

|

Our Board of Directors has approved a share buyback program

for the repurchase of up to 155,159,038 shares (which, based on the closing share price of October 30th, 2024, correspond to

approximately R$ 2 billion) to be executed within the next 18 months. For further details please see the Share Buyback Program section

on page 18.

|

[1]

The following operating and financial information, unless otherwise indicated, is presented in nominal Reais and prepared according to

the International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”)

and to the accounting practices issued by the Brazilian Accounting Standards Committee ("CPC”) and approved by the Brazilian

Securities and Exchange Commission (“CVM”). The information herein should be read together with our financial information

for the nine-month period ended September 30, 2024, filed with the CVM and submitted to the U.S. Securities and Exchange Commission (“SEC”).

[2]

The impacts resulting from applying Hyperinflation Accounting for our Argentinean subsidiaries, in accordance with IAS 29, are detailed

in the section Financial Reporting in Hyperinflationary Economies - Argentina (page 15). For YTD24, the definition of organic revenue

growth has been amended to cap the price growth in Argentina to a maximum of 2% per month (26.8% year-over-year). Corresponding adjustments

were made to all income statement related items in the organic growth calculations through scope changes. Further details on the cap methodology

are available at page 15.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 2 | |

| | |

MANAGEMENT

COMMENTS

Solid top line and bottom line growth, as well

as gross and Normalized EBITDA margins expansion

Our commercial execution coupled with operational leverage delivered

a mid-single digit topline growth and high-single digit bottom line growth (with Argentina organic results capped), with gross and Normalized

EBITDA margins expanding for the eighth consecutive quarter.

Brazil continued to lead the way. In Beer, premium/super premium

brands increased volumes by low twenties, and our core plus brands grew by low teens in the quarter. It was the 14th consecutive

quarter in which our premium/super premium brands growth outperformed total volumes. Our core brands declined by low-single digits, with

Brahma and Antarctica each delivering high-single digit volume growth. Moreover, brand health indicators continued to improve (with record

performance for Corona, Spaten, Budweiser and Original), which should support momentum going forward. In NAB, we achieved record volumes

for a third quarter, with growth continuing to be driven by health and wellness and energy brands.

In CAC, top line grew by mid-single digits and bottom line grew

in the high teens, with gross and Normalized EBITDA margins expansion. Performance was driven by the Dominican Republic, where we improved

volumes across all beer segments, led by Presidente family of brands. As for LAS and Canada, we delivered sequential improvement in the

quarter despite volume declines in Argentina and Canada given soft industries.

Cash COGS grew by low-single digits mostly driven by inflation and

lower tailwinds from commodity prices hedges, while Cash SG&A rose by mid-single digits due to higher investments behind our brands

and increased administrative expenses resulting from higher variable compensation accrual.

Normalized Profit decreased by 11.4%, with Normalized EBITDA growth

and improved net finance results more than offset by higher income tax expense in Brazil given lower deductibility relating to government

grants and IOC. And in terms of cash flow performance, cash flow from operating activities increased by R$185.5 million versus 3Q23.

YTD24 top line grew

by 4.7% (flat volumes and NR/hl +4.8%), and Normalized EBITDA increased by 12.0%, with gross and Normalized EBITDA margins expansion.

Normalized Profit declined by 6.7%.

| Financial highlights - Ambev consolidated |

|

|

|

|

|

|

|

|

| R$ million |

3Q23 |

3Q24 |

% As Reported |

%

Organic |

YTD23 |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

45,344.0 |

45,062.6 |

-0.6% |

-0.6% |

131,567.4 |

131,504.8 |

0.0% |

0.0% |

| Net revenue |

20,317.8 |

22,096.7 |

8.8% |

4.9% |

59,747.6 |

62,417.3 |

4.5% |

4.7% |

| Gross profit |

10,094.8 |

11,124.1 |

10.2% |

8.7% |

29,757.3 |

31,325.7 |

5.3% |

8.1% |

| % Gross margin |

49.7% |

50.3% |

60 bps |

180 bps |

49.8% |

50.2% |

40 bps |

160 bps |

| Normalized EBITDA |

6,584.3 |

7,063.4 |

7.3% |

8.5% |

18,303.9 |

19,409.2 |

6.0% |

12.0% |

| % Normalized EBITDA margin |

32.4% |

32.0% |

-40 bps |

110 bps |

30.6% |

31.1% |

50 bps |

220 bps |

| |

|

|

|

|

|

|

|

|

| Profit |

4,015.0 |

3,566.3 |

-11.2% |

- |

10,432.0 |

9,822.4 |

-5.8% |

- |

| Normalized profit |

4,038.9 |

3,579.6 |

-11.4% |

- |

10,559.7 |

9,855.9 |

-6.7% |

- |

| EPS (R$/shares) |

0.25 |

0.22 |

-11.4% |

- |

0.64 |

0.61 |

-5.5% |

- |

| Normalized EPS (R$/shares) |

0.25 |

0.22 |

-11.6% |

- |

0.65 |

0.61 |

-6.3% |

- |

Looking ahead, we remain focused on executing our commercial

strategy and are confident in our preparedness for the Summer season in South America, with healthier brands and sustained all-time-high

NPS levels. Our focus remains on delivering another year of top line growth (with a better balance between volumes and NR/hl), as well

as bottom line growth and gross and EBITDA margins expansion (led by costs and expenses discipline). We continue to expect our Cash COGS

per hectoliter in Brazil Beer (excluding non-Ambev marketplace products) to decrease between 0.5-3.0% in the year.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 3 | |

| | |

Ambev as a platform[3]

We remained focused on investing and executing in each of the six pillars of our platform framework:

Sustainability

As part of our ongoing commitment to foster moderate consumption

of alcoholic beverages, we held the 17th edition of “Beer Responsible Day”, with several initiatives to reinforce

that we are not interested in profiting from harmful consumption of our products. Over 10 thousand employees were engaged on awareness-raising

actions, visiting more than 100 thousand bars and restaurants across Brazil and distributing over 40,000 free bottles and cans of water

in regions and places where alcohol is consumed. Our campaign to incentivize moderate consumption on social media impacted more than 6

million people. Also, in the context of Responsible Day, we achieved a record of over 6 million units of Brahma 0.0, Budweiser Zero and

Corona Cero sold in a week.

Furthermore, to support the prevention of harmful consumption of

alcoholic beverages, we use technology and innovation to promote a balanced and responsible relationship in consumption. This quarter,

we expanded the offer of a digital health solution that analyzes population's consumption data and provides support and tools to reduce

excess consumption (e-SBI – screening and brief intervention).

[3] Considering BEES’ addressable market in Canada.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 4 | |

| | |

KEY

MARKETS PERFORMANCES

Brazil Beer: mid-single digit top line and

bottom line growth, with margin expansion

| · | Operating performance: volumes

were up 0.6% and top line grew by 3.5%, with NR/hl increasing sequentially (and by 2.9% vs. 3Q23), as the disciplined execution of our

revenue management strategy (with average prices to retailers growing in line with inflation), and positive brand mix were partially offset

by the impact of increased ICMS (VAT) taxable base in several States since the beginning of the year. Cash COGS/hl excluding the sale

of non-Ambev marketplace products declined by 1.3% primarily driven by hedged commodities prices tailwinds, while Cash SG&A increased

by 6.0%, led by higher S&M and administrative expenses partially offset by efficiencies in distribution (mainly given third-party

distributors mix). As a result, Normalized EBITDA grew by 5.8%, with Normalized EBITDA margin expanding 80 bps

to 34.9%. |

YTD24,

net revenue was up 4.9% (volumes +2.3% and NR/hl +2.5%), and Normalized EBITDA grew by 12.6%, with gross margin expansion of 200 bps,

and Normalized EBITDA margin expansion of 230 bps.

| · | Commercial highlights: the solid performance of our premium and

super premium brands delivered low-twenties volumes growth, led by Corona, Spaten and Original, which achieved their all-time-high brand

health indicators. Budweiser family drove core plus brands to low teens volumes growth, while in the core segment Brahma and Antarctica

each increased volumes by high-single digit. We continued to progress our digital initiatives, with BEES Marketplace growing GMV sequentially

and by 43% on a year-over-year basis, and Zé Delivery generating 16 million orders (+8% vs. 3Q23). |

| Brazil Beer[4] |

|

|

|

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

23,213.4 |

- |

- |

130.9 |

23,344.3 |

0.6% |

0.6% |

| Net revenue |

9,552.5 |

- |

- |

333.9 |

9,886.3 |

3.5% |

3.5% |

| Net revenue/hl (R$) |

411.5 |

- |

- |

12.0 |

423.5 |

2.9% |

2.9% |

| COGS |

(4,790.7) |

- |

- |

(34.4) |

(4,825.1) |

0.7% |

0.7% |

| COGS/hl (R$) |

(206.4) |

- |

- |

(0.3) |

(206.7) |

0.2% |

0.2% |

| COGS excl. deprec. & amort. |

(4,326.8) |

- |

- |

(17.1) |

(4,343.9) |

0.4% |

0.4% |

| COGS/hl excl. deprec. & amort. (R$) |

(186.4) |

- |

- |

0.3 |

(186.1) |

-0.2% |

-0.2% |

| Gross profit |

4,761.8 |

- |

- |

299.5 |

5,061.3 |

6.3% |

6.3% |

| % Gross margin |

49.8% |

- |

- |

- |

51.2% |

140 bps |

140 bps |

| SG&A excl. deprec. & amort. |

(2,411.8) |

- |

- |

(143.8) |

(2,555.6) |

6.0% |

6.0% |

| SG&A deprec. & amort. |

(452.2) |

- |

- |

(0.5) |

(452.7) |

0.1% |

0.1% |

| SG&A total |

(2,864.0) |

- |

- |

(144.3) |

(3,008.3) |

5.0% |

5.0% |

| Other operating income/(expenses) |

385.1 |

57.1 |

- |

19.5 |

461.6 |

19.9% |

5.1% |

| Other operating income/(expenses) excl. impair. |

390.9 |

57.1 |

- |

13.7 |

461.6 |

18.1% |

3.5% |

| Normalized Operating Profit |

2,283.0 |

57.1 |

- |

174.6 |

2,514.7 |

10.1% |

7.6% |

| % Normalized Operating margin |

23.9% |

- |

- |

- |

25.4% |

150 bps |

100 bps |

| Normalized EBITDA |

3,204.8 |

57.1 |

- |

186.6 |

3,448.5 |

7.6% |

5.8% |

| % Normalized EBITDA margin |

33.5% |

- |

- |

- |

34.9% |

140 bps |

80 bps |

| |

|

|

|

|

|

|

|

| Brazil Beer |

|

|

|

|

|

|

|

| R$ million |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

66,791.6 |

- |

- |

1,543.7 |

68,335.3 |

2.3% |

2.3% |

| Net revenue |

27,533.3 |

- |

- |

1,352.0 |

28,885.3 |

4.9% |

4.9% |

| Net revenue/hl (R$) |

412.2 |

- |

- |

10.5 |

422.7 |

2.5% |

2.5% |

| COGS |

(14,123.5) |

- |

- |

(129.2) |

(14,252.7) |

0.9% |

0.9% |

| COGS/hl (R$) |

(211.5) |

- |

- |

2.9 |

(208.6) |

-1.4% |

-1.4% |

| COGS excl. deprec. & amort. |

(12,720.1) |

- |

- |

(84.4) |

(12,804.5) |

0.7% |

0.7% |

| COGS/hl excl. deprec. & amort. (R$) |

(190.4) |

- |

- |

3.1 |

(187.4) |

-1.6% |

-1.6% |

| Gross profit |

13,409.7 |

- |

- |

1,222.8 |

14,632.6 |

9.1% |

9.1% |

| % Gross margin |

48.7% |

- |

- |

- |

50.7% |

200 bps |

200 bps |

| SG&A excl. deprec. & amort. |

(7,456.1) |

- |

- |

(463.0) |

(7,919.1) |

6.2% |

6.2% |

| SG&A deprec. & amort. |

(1,259.9) |

- |

- |

(99.2) |

(1,359.1) |

7.9% |

7.9% |

| SG&A total |

(8,716.0) |

- |

- |

(562.2) |

(9,278.2) |

6.5% |

6.5% |

| Other operating income/(expenses) |

988.7 |

117.3 |

- |

253.1 |

1,359.1 |

37.5% |

25.6% |

| Other operating income/(expenses) excl. impair. |

994.4 |

117.3 |

- |

247.4 |

1,359.1 |

36.7% |

24.9% |

| Normalized Operating Profit |

5,682.4 |

117.3 |

- |

913.7 |

6,713.4 |

18.1% |

16.1% |

| % Normalized Operating margin |

20.6% |

- |

- |

- |

23.2% |

260 bps |

220 bps |

| Normalized EBITDA |

8,351.5 |

117.3 |

- |

1,051.9 |

9,520.8 |

14.0% |

12.6% |

| % Normalized EBITDA margin |

30.3% |

- |

- |

- |

33.0% |

270 bps |

230 bps |

[4] In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$ 410.3 (2.6% organic growth) and R$ (173.8) (1.3% organic

decline), respectively. In YTD24 net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on

the marketplace, were R$ 409.4 (2.2% organic growth) and R$ (175.4) (2.6% organic decline), respectively. The scope change in

Brazil Beer refers to tax credits and related effects.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 5 | |

| | |

Brazil NAB: double-digit top line and bottom-line growth, with margin

expansion

| · | Operating performance: volumes grew by 3.4% led by our health

and wellness brands. Top line increased by 14.8%, with NR/hl up 11.0%, mostly driven by revenue management initiatives coupled with a

positive brand mix. Cash COGS/hl rose by 5.4% on the back of sugar prices headwinds, overall inflation and brand mix, while Cash SG&A

increased by 13.6% given higher distribution and administrative expenses. |

In YTD24, net revenue grew by 14.6% (volumes +5.8% and

NR/hl +8.3%), and Normalized EBITDA was up 25.5%, with gross margin expansion of 230 bps, and Normalized EBITDA margin expansion

of 240 bps.

| · | Commercial highlights: sustained positive performance of health

& wellness and energy brands continued to lead non-alcoholic volumes, mainly led by no-sugar carbonated soft drinks, Gatorade and

Red Bull. Guaraná Antarctica family delivered high-single digit volumes growth, with Guaraná Antarctica Zero increasing

by high-fifties, while Pepsi Black rose volumes in the low-twenties. The mix of single serve packages also increased and gained weight

in the quarter. |

| Brazil NAB[5] |

|

|

|

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

8,211.6 |

- |

- |

281.4 |

8,493.0 |

3.4% |

3.4% |

| Net revenue |

1,806.3 |

- |

- |

266.7 |

2,073.0 |

14.8% |

14.8% |

| Net revenue/hl (R$) |

220.0 |

- |

- |

24.1 |

244.1 |

11.0% |

11.0% |

| COGS |

(1,067.9) |

- |

- |

(61.8) |

(1,129.7) |

5.8% |

5.8% |

| COGS/hl (R$) |

(130.0) |

- |

- |

(3.0) |

(133.0) |

2.3% |

2.3% |

| COGS excl. deprec. & amort. |

(1,010.7) |

- |

- |

(91.0) |

(1,101.7) |

9.0% |

9.0% |

| COGS/hl excl. deprec. & amort. (R$) |

(123.1) |

- |

- |

(6.6) |

(129.7) |

5.4% |

5.4% |

| Gross profit |

738.4 |

- |

- |

204.8 |

943.3 |

27.7% |

27.7% |

| % Gross margin |

40.9% |

- |

- |

- |

45.5% |

460 bps |

460 bps |

| SG&A excl. deprec. & amort. |

(450.2) |

- |

- |

(61.4) |

(511.6) |

13.6% |

13.6% |

| SG&A deprec. & amort. |

(49.8) |

- |

- |

(12.9) |

(62.7) |

25.8% |

25.8% |

| SG&A total |

(500.0) |

- |

- |

(74.3) |

(574.3) |

14.9% |

14.9% |

| Other operating income/(expenses) |

109.4 |

10.1 |

- |

(15.6) |

103.9 |

-5.1% |

-14.3% |

| Normalized Operating Profit |

347.9 |

10.1 |

- |

114.9 |

472.9 |

35.9% |

33.0% |

| % Normalized Operating margin |

19.3% |

- |

- |

-% |

22.8% |

350 bps |

300 bps |

| Normalized EBITDA |

454.9 |

10.1 |

- |

98.6 |

563.6 |

23.9% |

21.7% |

| % Normalized EBITDA margin |

25.2% |

- |

- |

- |

27.2% |

200 bps |

150 bps |

| |

|

|

|

|

|

|

|

| Brazil NAB |

|

|

|

|

|

|

|

| R$ million |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

23,717.2 |

- |

- |

1,377.1 |

25,094.3 |

5.8% |

5.8% |

| Net revenue |

5,238.3 |

- |

- |

763.2 |

6,001.5 |

14.6% |

14.6% |

| Net revenue/hl (R$) |

220.9 |

- |

- |

18.3 |

239.2 |

8.3% |

8.3% |

| COGS |

(3,005.6) |

- |

- |

(300.7) |

(3,306.3) |

10.0% |

10.0% |

| COGS/hl (R$) |

(126.7) |

- |

- |

(5.0) |

(131.8) |

4.0% |

4.0% |

| COGS excl. deprec. & amort. |

(2,870.1) |

- |

- |

(315.8) |

(3,186.0) |

11.0% |

11.0% |

| COGS/hl excl. deprec. & amort. (R$) |

(121.0) |

- |

- |

(5.9) |

(127.0) |

4.9% |

4.9% |

| Gross profit |

2,232.7 |

- |

- |

462.5 |

2,695.2 |

20.7% |

20.7% |

| % Gross margin |

42.6% |

- |

- |

- |

44.9% |

230 bps |

230 bps |

| SG&A excl. deprec. & amort. |

(1,377.7) |

- |

- |

(74.8) |

(1,452.4) |

5.4% |

5.4% |

| SG&A deprec. & amort. |

(186.3) |

- |

- |

(4.9) |

(191.2) |

2.6% |

2.6% |

| SG&A total |

(1,563.9) |

- |

- |

(79.7) |

(1,643.6) |

5.1% |

5.1% |

| Other operating income/(expenses) |

328.2 |

20.7 |

- |

(36.9) |

312.0 |

-4.9% |

-11.2% |

| Normalized Operating Profit |

997.0 |

20.7 |

- |

346.0 |

1,363.6 |

36.8% |

34.7% |

| % Normalized Operating margin |

19.0% |

- |

- |

-% |

22.7% |

370 bps |

340 bps |

| Normalized EBITDA |

1,318.7 |

20.7 |

- |

335.7 |

1,675.1 |

27.0% |

25.5% |

| % Normalized EBITDA margin |

25.2% |

- |

- |

- |

27.9% |

270 bps |

240 bps |

[5] The scope change in Brazil NAB refers to tax credits and related effects.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 6 | |

| | |

BRAZIL

| Brazil[6] |

|

|

|

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

31,425.0 |

- |

- |

412.2 |

31,837.2 |

1.3% |

1.3% |

| Net revenue |

11,358.8 |

- |

- |

600.5 |

11,959.3 |

5.3% |

5.3% |

| Net revenue/hl (R$) |

361.5 |

- |

- |

14.2 |

375.6 |

3.9% |

3.9% |

| COGS |

(5,858.6) |

- |

- |

(96.2) |

(5,954.8) |

1.6% |

1.6% |

| COGS/hl (R$) |

(186.4) |

- |

- |

(0.6) |

(187.0) |

0.3% |

0.3% |

| COGS excl. deprec. & amort. |

(5,337.5) |

- |

- |

(108.1) |

(5,445.6) |

2.0% |

2.0% |

| COGS/hl excl. deprec. & amort. (R$) |

(169.8) |

- |

- |

(1.2) |

(171.0) |

0.7% |

0.7% |

| Gross profit |

5,500.2 |

- |

- |

504.3 |

6,004.5 |

9.2% |

9.2% |

| % Gross margin |

48.4% |

- |

- |

- |

50.2% |

180 bps |

180 bps |

| SG&A excl. deprec. & amort. |

(2,861.9) |

- |

- |

(205.3) |

(3,067.2) |

7.2% |

7.2% |

| SG&A deprec. & amort. |

(502.0) |

- |

- |

(13.3) |

(515.3) |

2.7% |

2.7% |

| SG&A total |

(3,363.9) |

- |

- |

(218.6) |

(3,582.5) |

6.5% |

6.5% |

| Other operating income/(expenses) |

494.5 |

67.1 |

- |

3.9 |

565.5 |

14.4% |

0.8% |

| Other operating income/(expenses) excl. impair. |

500.3 |

67.1 |

- |

(1.9) |

565.5 |

13.0% |

-0.4% |

| Normalized Operating Profit |

2,630.9 |

67.1 |

- |

289.5 |

2,987.5 |

13.6% |

11.0% |

| % Normalized Operating margin |

23.2% |

- |

- |

-0% |

25.0% |

180 bps |

120 bps |

| Normalized EBITDA |

3,659.7 |

67.1 |

- |

285.2 |

4,012.0 |

9.6% |

7.8% |

| % Normalized EBITDA margin |

32.2% |

- |

- |

- |

33.5% |

130 bps |

80 bps |

| |

|

|

|

|

|

|

|

| Brazil |

|

|

|

|

|

|

|

| R$ million |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

90,508.8 |

- |

- |

2,920.8 |

93,429.6 |

3.2% |

3.2% |

| Net revenue |

32,771.5 |

- |

- |

2,115.2 |

34,886.7 |

6.5% |

6.5% |

| Net revenue/hl (R$) |

362.1 |

- |

- |

11.3 |

373.4 |

3.1% |

3.1% |

| COGS |

(17,129.1) |

- |

- |

(429.8) |

(17,559.0) |

2.5% |

2.5% |

| COGS/hl (R$) |

(189.3) |

- |

- |

1.3 |

(187.9) |

-0.7% |

-0.7% |

| COGS excl. deprec. & amort. |

(15,590.2) |

- |

- |

(400.2) |

(15,990.4) |

2.6% |

2.6% |

| COGS/hl excl. deprec. & amort. (R$) |

(172.3) |

- |

- |

1.1 |

(171.1) |

-0.6% |

-0.6% |

| Gross profit |

15,642.4 |

- |

- |

1,685.4 |

17,327.8 |

10.8% |

10.8% |

| % Gross margin |

47.7% |

- |

- |

- |

49.7% |

200 bps |

200 bps |

| SG&A excl. deprec. & amort. |

(8,833.8) |

- |

- |

(537.7) |

(9,371.5) |

6.1% |

6.1% |

| SG&A deprec. & amort. |

(1,446.2) |

- |

- |

(104.2) |

(1,550.3) |

7.2% |

7.2% |

| SG&A total |

(10,279.9) |

- |

- |

(641.9) |

(10,921.8) |

6.2% |

6.2% |

| Other operating income/(expenses) |

1,316.9 |

138.0 |

- |

216.2 |

1,671.1 |

26.9% |

16.4% |

| Other operating income/(expenses) excl. impair. |

1,322.7 |

138.0 |

- |

210.5 |

1,671.1 |

26.3% |

15.9% |

| Normalized Operating Profit |

6,679.4 |

138.0 |

- |

1,259.7 |

8,077.1 |

20.9% |

18.9% |

| % Normalized Operating margin |

20.4% |

- |

- |

- |

23.2% |

280 bps |

240 bps |

| Normalized EBITDA |

9,670.2 |

138.0 |

- |

1,387.7 |

11,195.9 |

15.8% |

14.4% |

| % Normalized EBITDA margin |

29.5% |

- |

- |

- |

32.1% |

260 bps |

220 bps |

[6] In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$ 365.9 (3.7% organic growth) and R$ (162.0) (0.1% organic decline),

respectively. In YTD24, net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on the marketplace,

were R$ 363.7 (2.9% organic growth) and R$ (162.4) (1.3% organic decline), respectively. The scope change in Brazil refers to tax

credits and related effects.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 7 | |

| | |

Central America and the Caribbean (CAC): mid-single

digit top line and double-digit bottom line growth, with margin expansion

| · | Operating performance: top line was up 4.7%, with NR/hl growing

by 5.2%, thanks to revenue management initiatives and positive package mix in the Dominican Republic, which also grew volumes by mid-single

digits. Cash COGS/hl was down 9.8% primarily due to FX tailwinds and lower freight prices, while Cash SG&A rose by 22.5% as a result

of greater investments behind our brands and higher administrative expenses. |

In YTD24, net revenue increased by 7.1% (volumes +2.7% and

NR/hl +4.3%), and Normalized EBITDA grew by 18.6%, with gross margin expansion of 490 bps, and Normalized EBITDA margin expansion

of 400 bps.

| · | Commercial highlights: in the Dominican Republic, volumes grew

in all beer segments. Premium brands grew volumes by mid-single digits (led by Corona family), while Presidente family improved volumes

in the low teens. Both families of brands improved their health indicators in the quarter. |

| CAC[7] |

|

|

|

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

3,124.8 |

- |

- |

(15.3) |

3,109.6 |

-0.5% |

-0.5% |

| Net revenue |

2,469.2 |

- |

274.0 |

115.2 |

2,858.5 |

15.8% |

4.7% |

| Net revenue/hl (R$) |

790.2 |

- |

88.1 |

40.9 |

919.3 |

16.3% |

5.2% |

| COGS |

(1,317.9) |

- |

(127.6) |

156.6 |

(1,288.9) |

-2.2% |

-11.9% |

| COGS/hl (R$) |

(421.7) |

- |

(41.0) |

48.3 |

(414.5) |

-1.7% |

-11.4% |

| COGS excl. deprec. & amort. |

(1,140.5) |

- |

(113.4) |

116.9 |

(1,137.0) |

-0.3% |

-10.3% |

| COGS/hl excl. deprec. & amort. (R$) |

(365.0) |

- |

(36.5) |

35.8 |

(365.6) |

0.2% |

-9.8% |

| Gross profit |

1,151.4 |

- |

146.4 |

271.8 |

1,569.7 |

36.3% |

23.6% |

| % Gross margin |

46.6% |

- |

- |

- |

54.9% |

830 bps |

850 bps |

| SG&A excl. deprec. & amort. |

(387.0) |

- |

(54.8) |

(87.1) |

(528.9) |

36.7% |

22.5% |

| SG&A deprec. & amort. |

(8.4) |

- |

(7.4) |

(42.8) |

(58.5) |

nm |

nm |

| SG&A total |

(395.3) |

- |

(62.2) |

(129.9) |

(587.4) |

48.6% |

32.9% |

| Other operating income/(expenses) |

(16.9) |

- |

0.3 |

18.8 |

2.1 |

-112.7% |

-111.0% |

| Normalized Operating Profit |

739.1 |

- |

84.5 |

160.7 |

984.4 |

33.2% |

21.7% |

| % Normalized Operating margin |

29.9% |

- |

- |

- |

34.4% |

450 bps |

490 bps |

| Normalized EBITDA |

924.9 |

- |

106.1 |

163.8 |

1,194.8 |

29.2% |

17.7% |

| % Normalized EBITDA margin |

37.5% |

- |

- |

- |

41.8% |

430 bps |

460 bps |

| |

|

|

|

|

|

|

|

| CAC |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| R$ million |

| Volume ('000 hl) |

8,821.3 |

- |

- |

237.7 |

9,059.0 |

2.7% |

2.7% |

| Net revenue |

7,248.4 |

- |

(9.3) |

514.1 |

7,753.2 |

7.0% |

7.1% |

| Net revenue/hl (R$) |

821.7 |

- |

(1.0) |

35.2 |

855.9 |

4.2% |

4.3% |

| COGS |

(3,694.7) |

- |

(13.9) |

115.5 |

(3,593.1) |

-2.7% |

-3.1% |

| COGS/hl (R$) |

(418.8) |

- |

(1.5) |

23.7 |

(396.6) |

-5.3% |

-5.7% |

| COGS excl. deprec. & amort. |

(3,286.4) |

- |

(17.5) |

115.4 |

(3,188.5) |

-3.0% |

-3.5% |

| COGS/hl excl. deprec. & amort. (R$) |

(372.6) |

- |

(1.9) |

22.5 |

(352.0) |

-5.5% |

-6.0% |

| Gross profit |

3,553.7 |

- |

(23.2) |

629.6 |

4,160.1 |

17.1% |

17.7% |

| % Gross margin |

49.0% |

- |

- |

- |

53.7% |

470 bps |

490 bps |

| SG&A excl. deprec. & amort. |

(1,254.0) |

- |

(6.6) |

(148.0) |

(1,408.6) |

12.3% |

11.8% |

| SG&A deprec. & amort. |

(179.0) |

- |

(0.4) |

2.4 |

(176.9) |

-1.1% |

-1.4% |

| SG&A total |

(1,433.0) |

- |

(6.9) |

(145.6) |

(1,585.5) |

10.6% |

10.2% |

| Other operating income/(expenses) |

(12.4) |

- |

0.3 |

20.5 |

8.3 |

-166.8% |

-164.3% |

| Normalized Operating Profit |

2,108.3 |

- |

(29.9) |

504.5 |

2,582.9 |

22.5% |

23.9% |

| % Normalized Operating margin |

29.1% |

- |

- |

- |

33.3% |

420 bps |

460 bps |

| Normalized EBITDA |

2,695.6 |

- |

(33.0) |

501.9 |

3,164.4 |

17.4% |

18.6% |

| % Normalized EBITDA margin |

37.2% |

- |

- |

- |

40.8% |

360 bps |

400 bps |

[7] In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$ 880.8 (4.3% organic growth) and R$ (331.1) (12.1% organic

decline), respectively. In YTD24, net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on

the marketplace, were R$815.5 (3.1% organic growth) and R$ (316.3) (8.9% organic decline), respectively.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 8 | |

| | |

Latin America South (LAS): high single-digit

top line and bottom line growth, amid a tough macroeconomic scenario in Argentina

| · | Operating performance: volumes were down 7.7% as inflationary

pressures on overall consumer demand in Argentina (where volumes declined by mid-teens) were partially offset by positive performances

in Bolivia and Chile. Top line increased by 6.9%, with NR/hl growing 15.9% mainly due to the execution of our revenue management strategy.

Cash COGS/hl and Cash SG&A continued to be impacted by overall inflation. |

In

YTD24, net revenue was up 3.8% (volumes -11.3% and

NR/hl +17.1%), and Normalized EBITDA rose by 8.4%, with

gross margin expansion of 60 bps,

and Normalized EBITDA margin expansion of 140 bps.

| · | Commercial highlights: in Argentina industry remains challenging,

but we continued to work to be better prepared for the future. We gained market share according to our estimates and the health indicator

of our brands improved. In Bolivia, volumes grew by low twenties, led mainly by the performance of our core brands, with a highlight to

Paceña. In Chile, our core plus segment drove low-single digits volume increase, and our brands gained market share according to

our estimates. In Paraguay, despite total volumes mostly impacted by a soft industry in the face of poor weather, our premium brands rose

by high-single digits, led by Bud 66 and Corona. |

| LAS[8] |

|

|

|

IAS 29

6M Impact |

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

8,307.9 |

- |

- |

- |

(642.9) |

7,665.0 |

-7.7% |

-7.7% |

| Net revenue |

3,898.0 |

3,203.2 |

(843.7) |

(2,145.4) |

269.8 |

4,381.8 |

12.4% |

6.9% |

| Net revenue/hl (R$) |

469.2 |

385.6 |

(110.1) |

(247.6) |

74.6 |

571.7 |

21.8% |

15.9% |

| COGS |

(1,972.8) |

(2,340.4) |

813.1 |

1,139.6 |

(137.5) |

(2,498.1) |

26.6% |

7.0% |

| COGS/hl (R$) |

(237.5) |

(281.7) |

106.1 |

125.1 |

(37.9) |

(325.9) |

37.2% |

15.9% |

| COGS excl. deprec. & amort. |

(1,758.8) |

(2,175.0) |

747.5 |

1,012.5 |

(92.4) |

(2,266.2) |

28.9% |

5.3% |

| COGS/hl excl. deprec. & amort. (R$) |

(211.7) |

(261.8) |

97.5 |

110.1 |

(29.8) |

(295.7) |

39.7% |

14.1% |

| Gross profit |

1,925.1 |

862.7 |

(30.6) |

(1,005.8) |

132.3 |

1,883.8 |

-2.1% |

6.9% |

| % Gross margin |

49.4% |

- |

- |

- |

- |

43.0% |

-640 bps |

0 bps |

| SG&A excl. deprec. & amort. |

(898.7) |

(1,071.2) |

312.5 |

605.9 |

(82.2) |

(1,133.7) |

26.1% |

9.1% |

| SG&A deprec. & amort. |

(92.8) |

(109.2) |

39.8 |

61.4 |

(11.8) |

(112.6) |

21.3% |

12.7% |

| SG&A total |

(991.5) |

(1,180.4) |

352.4 |

667.3 |

(94.0) |

(1,246.3) |

25.7% |

9.5% |

| Other operating income/(expenses) |

(6.1) |

47.9 |

(35.1) |

3.5 |

16.2 |

26.4 |

nm |

nm |

| Normalized Operating Profit |

927.6 |

(269.8) |

286.6 |

(335.0) |

54.6 |

663.9 |

-28.4% |

5.9% |

| % Normalized Operating margin |

23.8% |

- |

- |

- |

- |

15.2% |

-860 bps |

-20 bps |

| Normalized EBITDA |

1,234.5 |

4.8 |

181.2 |

(523.6) |

111.4 |

1,008.3 |

-18.3% |

9.0% |

| % Normalized EBITDA margin |

31.7% |

- |

- |

- |

- |

23.0% |

-870 bps |

60 bps |

| |

|

|

|

|

|

|

|

|

| LAS |

YTD23 |

Scope |

Currency Translation |

|

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| R$ million |

IAS 29

6M Impact |

| Volume ('000 hl) |

25,247.1 |

- |

- |

- |

(2,859.3) |

22,387.8 |

-11.3% |

-11.3% |

| Net revenue |

12,295.9 |

13,292.7 |

(10,801.2) |

(2,862.1) |

467.0 |

12,392.4 |

0.8% |

3.8% |

| Net revenue/hl (R$) |

487.0 |

526.5 |

(482.5) |

(60.6) |

83.1 |

553.5 |

13.7% |

17.1% |

| COGS |

(6,021.6) |

(8,479.4) |

6,385.5 |

1,501.3 |

(161.5) |

(6,775.8) |

12.5% |

2.7% |

| COGS/hl (R$) |

(238.5) |

(335.9) |

285.2 |

24.2 |

(37.7) |

(302.7) |

26.9% |

15.8% |

| COGS excl. deprec. & amort. |

(5,398.7) |

(7,743.3) |

5,728.6 |

1,330.3 |

(39.1) |

(6,122.1) |

13.4% |

0.7% |

| COGS/hl excl. deprec. & amort. (R$) |

(213.8) |

(306.7) |

255.9 |

20.3 |

(29.1) |

(273.5) |

27.9% |

13.6% |

| Gross profit |

6,274.3 |

4,813.3 |

(4,415.7) |

(1,360.7) |

305.4 |

5,616.6 |

-10.5% |

4.9% |

| % Gross margin |

51.0% |

- |

- |

- |

- |

45.3% |

-570 bps |

60 bps |

| SG&A excl. deprec. & amort. |

(2,986.8) |

(4,081.1) |

3,139.9 |

781.1 |

(130.7) |

(3,277.7) |

9.7% |

4.4% |

| SG&A deprec. & amort. |

(290.9) |

(391.8) |

327.4 |

77.4 |

(42.1) |

(319.9) |

10.0% |

14.5% |

| SG&A total |

(3,277.7) |

(4,472.9) |

3,467.3 |

858.5 |

(172.8) |

(3,597.6) |

9.8% |

5.3% |

| Other operating income/(expenses) |

31.9 |

(42.6) |

(12.1) |

8.8 |

32.8 |

18.8 |

-41.1% |

102.8% |

| Normalized Operating Profit |

3,028.5 |

297.9 |

(960.6) |

(493.4) |

165.4 |

2,037.8 |

-32.7% |

5.5% |

| % Normalized Operating margin |

24.6% |

- |

- |

- |

- |

16.4% |

-820 bps |

40 bps |

| Normalized EBITDA |

3,942.3 |

1,425.8 |

(1,944.8) |

(741.8) |

330.0 |

3,011.4 |

-23.6% |

8.4% |

| % Normalized EBITDA margin |

32.1% |

- |

- |

- |

- |

24.3% |

-780 bps |

140 bps |

[8] In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$ 564.5 (15.9% organic growth) and R$ (289.4) (13.9% organic

growth), respectively. In YTD24, net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on

the marketplace, were R$ 545.2 (17.1% organic growth) and R$ (266.0) (13.5% organic growth), respectively. Reported numbers are presented

applying Hyperinflation Accounting for our Argentinean operations, as detailed on page 15.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 9 | |

| | |

Canada: sequential improvement in both top

line and bottom line

| · | Operating performance: top line was up 0.1% with industry driven volumes decline (-1.4%)

offset by NR/hl growth (+1.5%) led by revenue management initiatives and continued premiumization of our portfolio. Cash SG&A efficiencies

offset Cash COGS/hl increase (in the face of 3Q23 tough comp), driving a flat Normalized EBITDA performance. |

In YTD24, net revenue

was down 3.7% (volumes -5.2% and NR/hl +1.5%), and Normalized EBITDA declined by 1.1%, with gross margin contraction of 50 bps, and Normalized

EBITDA margin expansion of 70 bps.

| · | Commercial highlights: our market share remained stable, according to

our estimates, improving throughout the quarter backed by the momentum of our beer portfolio. Four of our beer brands were in the top

five fastest growing brands in the country, led by Michelob Ultra which was number one. Our premium and core plus brands grew volumes

by low-single digits, led by Corona and Michelob Ultra, respectively. Our brand heath indicators improved, with a highlight to Corona

that continued to hold the highest indicator in the market. |

| Canada[9] |

|

|

|

|

|

|

|

| R$ million |

3Q23 |

Scope |

Currency Translation |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

2,486.3 |

- |

- |

(35.5) |

2,450.8 |

-1.4% |

-1.4% |

| Net revenue |

2,591.8 |

- |

304.0 |

1.3 |

2,897.1 |

11.8% |

0.1% |

| Net revenue/hl (R$) |

1,042.4 |

- |

124.0 |

15.7 |

1,182.1 |

13.4% |

1.5% |

| COGS |

(1,073.7) |

- |

(130.4) |

(26.8) |

(1,230.9) |

14.6% |

2.5% |

| COGS/hl (R$) |

(431.9) |

- |

(53.2) |

(17.2) |

(502.2) |

16.3% |

4.0% |

| COGS excl. deprec. & amort. |

(985.8) |

- |

(121.9) |

(40.7) |

(1,148.4) |

16.5% |

4.1% |

| COGS/hl excl. deprec. & amort. (R$) |

(396.5) |

- |

(49.8) |

(22.3) |

(468.6) |

18.2% |

5.6% |

| Gross profit |

1,518.0 |

- |

173.6 |

(25.4) |

1,666.2 |

9.8% |

-1.7% |

| % Gross margin |

58.6% |

|

- |

- |

57.5% |

-110 bps |

-100 bps |

| SG&A excl. deprec. & amort. |

(844.0) |

- |

(99.5) |

41.6 |

(901.8) |

6.9% |

-4.9% |

| SG&A deprec. & amort. |

(62.0) |

- |

(8.5) |

2.1 |

(68.3) |

10.2% |

-3.5% |

| SG&A total |

(905.9) |

- |

(108.0) |

43.8 |

(970.1) |

7.1% |

-4.8% |

| Other operating income/(expenses) |

3.2 |

- |

0.4 |

(2.3) |

1.3 |

-59.6% |

-73.6% |

| Normalized Operating Profit |

615.2 |

- |

66.1 |

16.0 |

697.3 |

13.3% |

2.6% |

| % Normalized Operating margin |

23.7% |

- |

- |

- |

24.1% |

40 bps |

60 bps |

| Normalized EBITDA |

765.2 |

- |

83.0 |

(0.0) |

848.2 |

10.9% |

0.0% |

| % Normalized EBITDA margin |

29.5% |

- |

- |

- |

29.3% |

-20 bps |

0 bps |

| |

|

|

|

|

|

|

|

| Canada |

|

|

|

|

|

|

|

| R$ million |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

6,990.2 |

- |

- |

(361.7) |

6,628.5 |

-5.2% |

-5.2% |

| Net revenue |

7,431.8 |

- |

228.5 |

(275.3) |

7,384.9 |

-0.6% |

-3.7% |

| Net revenue/hl (R$) |

1,063.2 |

- |

34.5 |

16.5 |

1,114.1 |

4.8% |

1.5% |

| COGS |

(3,144.9) |

- |

(97.9) |

79.1 |

(3,163.6) |

0.6% |

-2.5% |

| COGS/hl (R$) |

(449.9) |

- |

(14.8) |

(12.6) |

(477.3) |

6.1% |

2.8% |

| COGS excl. deprec. & amort. |

(2,929.0) |

- |

(91.5) |

63.3 |

(2,957.2) |

1.0% |

-2.2% |

| COGS/hl excl. deprec. & amort. (R$) |

(419.0) |

- |

(13.8) |

(13.3) |

(446.1) |

6.5% |

3.2% |

| Gross profit |

4,286.9 |

- |

130.6 |

(196.2) |

4,221.3 |

-1.5% |

-4.6% |

| % Gross margin |

57.7% |

|

- |

- |

57.2% |

-50 bps |

-50 bps |

| SG&A excl. deprec. & amort. |

(2,522.8) |

- |

(74.3) |

197.1 |

(2,399.9) |

-4.9% |

-7.8% |

| SG&A deprec. & amort. |

(194.5) |

- |

(6.3) |

(1.2) |

(202.0) |

3.8% |

0.6% |

| SG&A total |

(2,717.4) |

- |

(80.5) |

195.9 |

(2,601.9) |

-4.2% |

-7.2% |

| Other operating income/(expenses) |

15.9 |

- |

0.3 |

(6.5) |

9.7 |

-39.1% |

-41.0% |

| Normalized Operating Profit |

1,585.5 |

- |

50.4 |

(6.8) |

1,629.1 |

2.7% |

-0.4% |

| % Normalized Operating margin |

21.3% |

- |

- |

- |

22.1% |

80 bps |

80 bps |

| Normalized EBITDA |

1,995.8 |

- |

63.0 |

(21.4) |

2,037.4 |

2.1% |

-1.1% |

| % Normalized EBITDA margin |

26.9% |

- |

- |

- |

27.6% |

70 bps |

70 bps |

[9] In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$ 1,179.6 (1.3% organic growth) and R$ (466.8) (5.3% organic

growth), respectively. In YTD24, net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on

the marketplace, were R$ 1,112.1 (1.4% organic growth) and R$ (444.7) (2.9% organic growth), respectively.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 10 | |

| | |

AMBEV

CONSOLIDATED

| Ambev[10] |

|

|

Currency Translation |

IAS 29

6M Impact |

|

|

|

|

| R$ million |

3Q23 |

Scope |

Organic Growth |

3Q24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

45,344.0 |

- |

- |

- |

(281.5) |

45,062.6 |

-0.6% |

-0.6% |

| Net revenue |

20,317.8 |

3,203.2 |

(265.7) |

(2,145.4) |

986.9 |

22,096.7 |

8.8% |

4.9% |

| Net revenue/hl (R$) |

448.1 |

70.6 |

(5.9) |

(47.2) |

24.7 |

490.4 |

9.4% |

5.5% |

| COGS |

(10,223.0) |

(2,340.4) |

555.2 |

1,139.6 |

(103.9) |

(10,972.6) |

7.3% |

1.0% |

| COGS/hl (R$) |

(225.5) |

(51.6) |

12.3 |

25.0 |

(3.7) |

(243.5) |

8.0% |

1.6% |

| COGS excl. deprec. & amort. |

(9,222.4) |

(2,175.0) |

512.2 |

1,012.5 |

(124.3) |

(9,997.1) |

8.4% |

1.3% |

| COGS/hl excl. deprec. & amort. (R$) |

(203.4) |

(48.0) |

11.4 |

22.2 |

(4.0) |

(221.9) |

9.1% |

2.0% |

| Gross profit |

10,094.8 |

862.7 |

289.4 |

(1,005.8) |

883.0 |

11,124.1 |

10.2% |

8.7% |

| % Gross margin |

49.7% |

- |

- |

- |

- |

50.3% |

60 bps |

180 bps |

| SG&A excl. deprec. & amort. |

(4,991.6) |

(1,071.2) |

158.3 |

605.9 |

(332.9) |

(5,631.5) |

12.8% |

6.7% |

| SG&A deprec. & amort. |

(665.1) |

(109.2) |

24.0 |

61.4 |

(65.8) |

(754.8) |

13.5% |

9.9% |

| SG&A total |

(5,656.7) |

(1,180.4) |

182.2 |

667.3 |

(398.7) |

(6,386.3) |

12.9% |

7.0% |

| Other operating income/(expenses) |

474.7 |

115.0 |

(34.4) |

3.5 |

36.5 |

595.3 |

25.4% |

7.7% |

| Other operating income/(expenses) excl. impair. |

480.5 |

115.0 |

(34.4) |

3.5 |

30.8 |

595.3 |

23.9% |

6.4% |

| Normalized Operating Profit |

4,912.8 |

(202.7) |

437.3 |

(335.0) |

520.8 |

5,333.1 |

8.6% |

10.6% |

| % Normalized Operating margin |

24.2% |

0.0% |

0.0% |

0.0% |

0.0% |

24.1% |

-10 bps |

130 bps |

| Exceptional items above EBITDA |

(16.6) |

(1.5) |

1.7 |

1.9 |

(4.3) |

(18.9) |

13.5% |

25.8% |

| Net finance results |

(837.9) |

- |

- |

- |

- |

(681.5) |

-18.7% |

- |

| Share of results of joint ventures |

1.4 |

- |

- |

- |

- |

36.8 |

nm |

- |

| Income tax expense |

(44.7) |

- |

- |

- |

- |

(1,103.3) |

nm |

- |

| Profit |

4,015.0 |

- |

- |

- |

- |

3,566.3 |

-11.2% |

- |

| Attributable to Ambev holders |

3,911.7 |

- |

- |

- |

- |

3,460.3 |

-11.5% |

- |

| Attributable to non-controlling interests |

103.3 |

- |

- |

- |

- |

106.0 |

2.7% |

- |

| |

|

|

|

|

|

|

|

|

| Normalized profit |

4,038.9 |

- |

- |

- |

- |

3,579.6 |

-11.4% |

- |

| Attributable to Ambev holders |

3,935.4 |

- |

- |

- |

- |

3,473.5 |

-11.7% |

- |

| |

|

|

|

|

|

|

|

|

| Normalized EBITDA |

6,584.3 |

72.0 |

370.3 |

(523.6) |

560.5 |

7,063.4 |

7.3% |

8.5% |

| % Normalized EBITDA margin |

32.4% |

- |

- |

- |

- |

32.0% |

-40 bps |

110 bps |

| |

|

|

|

|

|

|

|

|

| Ambev |

|

|

|

|

|

|

|

|

| R$ million |

YTD23 |

Scope |

Currency Translation |

IAS 29

6M Impact |

Organic Growth |

YTD24 |

% As Reported |

%

Organic |

| Volume ('000 hl) |

131,567.4 |

- |

- |

- |

(62.6) |

131,504.8 |

0.0% |

0.0% |

| Net revenue |

59,747.6 |

13,292.7 |

(10,582.0) |

(2,862.1) |

2,820.9 |

62,417.3 |

4.5% |

4.7% |

| Net revenue/hl (R$) |

454.1 |

101.0 |

(80.5) |

(21.7) |

21.7 |

474.6 |

4.5% |

4.8% |

| COGS |

(29,990.3) |

(8,479.4) |

6,273.6 |

1,501.3 |

(396.8) |

(31,091.6) |

3.7% |

1.3% |

| COGS/hl (R$) |

(227.9) |

(64.4) |

47.7 |

11.4 |

(3.2) |

(236.4) |

3.7% |

1.4% |

| COGS excl. deprec. & amort. |

(27,204.4) |

(7,743.3) |

5,619.7 |

1,330.3 |

(260.6) |

(28,258.2) |

3.9% |

1.0% |

| COGS/hl excl. deprec. & amort. (R$) |

(206.8) |

(58.9) |

42.7 |

10.1 |

(2.1) |

(214.9) |

3.9% |

1.0% |

| Gross profit |

29,757.3 |

4,813.3 |

(4,308.4) |

(1,360.7) |

2,424.2 |

31,325.7 |

5.3% |

8.1% |

| % Gross margin |

49.8% |

- |

- |

- |

- |

50.2% |

40 bps |

160 bps |

| SG&A excl. deprec. & amort. |

(15,597.4) |

(4,081.1) |

3,059.1 |

781.1 |

(619.3) |

(16,457.7) |

5.5% |

4.0% |

| SG&A deprec. & amort. |

(2,110.5) |

(391.8) |

320.8 |

77.4 |

(145.1) |

(2,249.1) |

6.6% |

6.9% |

| SG&A total |

(17,707.9) |

(4,472.9) |

3,379.8 |

858.5 |

(764.4) |

(18,706.8) |

5.6% |

4.3% |

| Other operating income/(expenses) |

1,352.2 |

95.4 |

(11.5) |

8.8 |

263.0 |

1,707.9 |

26.3% |

19.4% |

| Other operating income/(expenses) excl. impair. |

1,358.0 |

95.4 |

(11.5) |

8.8 |

257.2 |

1,707.9 |

25.8% |

18.9% |

| Normalized Operating Profit |

13,401.6 |

435.9 |

(940.0) |

(493.4) |

1,922.7 |

14,326.8 |

6.9% |

14.3% |

| % Normalized Operating margin |

22.4% |

- |

- |

- |

- |

23.0% |

60 bps |

210 bps |

| Exceptional items above EBITDA |

(168.0) |

(12.6) |

11.1 |

2.4 |

118.9 |

(48.2) |

-71.3% |

-70.8% |

| Net finance results |

(2,909.2) |

- |

- |

- |

- |

(1,703.7) |

-41.4% |

- |

| Share of results of joint ventures |

(15.2) |

- |

- |

- |

- |

1.8 |

-112.0% |

- |

| Income tax expense |

122.7 |

- |

- |

- |

- |

(2,754.4) |

nm |

- |

| Profit |

10,432.0 |

- |

- |

- |

- |

9,822.4 |

-5.8% |

- |

| Attributable to Ambev holders |

10,114.3 |

- |

- |

- |

- |

9,556.9 |

-5.5% |

- |

| Attributable to non-controlling interests |

317.7 |

- |

- |

- |

- |

265.5 |

-16.4% |

- |

| |

|

|

|

|

|

|

|

|

| Normalized profit |

10,559.7 |

- |

- |

- |

- |

9,855.9 |

-6.7% |

- |

| Attributable to Ambev holders |

10,240.4 |

- |

- |

- |

- |

9,590.2 |

-6.3% |

- |

| |

|

|

|

|

|

|

|

|

| Normalized EBITDA |

18,303.9 |

1,563.8 |

(1,914.8) |

(741.8) |

2,198.1 |

19,409.2 |

6.0% |

12.0% |

| % Normalized EBITDA margin |

30.6% |

- |

- |

- |

- |

31.1% |

50 bps |

220 bps |

[10]In 3Q24, net revenue per hectoliter and Cash COGS per hectoliter,

excluding the sale of non-Ambev products on the marketplace, were R$479.5 (5.3% organic growth) and R$ (211.9) (1.2% organic growth),

respectively. In YTD24, net revenue per hectoliter and Cash COGS per hectoliter, excluding the sale of non-Ambev products on the marketplace,

were R$ 463.4 (4.4% organic growth) and R$ (204.8) (0.2% organic growth), respectively. The scope changes refer to tax credits and related

effects in Brazil.

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 11 | |

| | |

OTHER

OPERATING INCOME/EXPENSES

| Other operating income/(expenses) |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| R$ million |

| |

|

|

|

|

| Government grants/NPV of long term fiscal incentives |

425.4 |

479.4 |

1,180.9 |

1,301.1 |

| Credits/(debits) taxes extemporaneous |

- |

22.9 |

- |

22.9 |

| (Additions to)/reversals of provisions |

(0.8) |

(8.0) |

(12.5) |

(19.9) |

| Gain/(loss) on disposal of fixed assets, intangible assets and operations in associates |

12.0 |

33.0 |

54.6 |

74.9 |

| Net other operating income/(expenses) |

38.2 |

68.0 |

129.3 |

328.9 |

| |

|

|

|

|

| Other operating income/(expenses) |

474.7 |

595.3 |

1,352.2 |

1,707.9 |

EXCEPTIONAL

ITEMS

Exceptional items corresponded to

restructuring expenses primarily linked to centralization and restructuring projects in Brazil, LAS, CAC and Canada.

| Exceptional Items |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| R$ million |

| |

|

|

|

|

| Restructuring |

(16.1) |

(18.4) |

(72.4) |

(47.4) |

| IAS 29/CPC 42 (hyperinflation) application effect |

(0.5) |

(0.5) |

(0.9) |

(0.8) |

| Legal Fees |

- |

- |

(94.7) |

- |

| |

|

|

|

|

| Exceptional Items |

(16.6) |

(18.9) |

(167.9) |

(48.2) |

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 12 | |

| | |

NET

FINANCE RESULTS

Net finance

results in 3Q24 totaled R$ (681.5) million, an improvement of R$ 156.4 million compared to

3Q23, broken down as follows:

| · | Interest income totaled R$ 502.5 million, mainly explained by: (i) interest

rate update on Brazilian tax credits of R$ 190.7 million, and (ii) interest income of R$ 184.9 million from cash balance investments in

Brazil and Argentina, with average reference interest rate of 11% in Brazil and 35% in Argentina. |

| · | Interest expense totaled R$ (487.5)

million, mainly impacted by: (i) fair value adjustments of payables pursuant to by IFRS 13 (CPC 46) of R$ (245.6) million, (ii) lease

liabilities interest accruals of R$ (44.1) million in accordance with IFRS 16 (CPC 06 R2), (iii) interest on tax incentives of R$ (41.6)

million, and (iv) CND put option interest accruals of R$ (27.9) million. |

| · | Losses on derivative instruments of R$ (170.3)

million, mainly explained by (i) hedging carry costs related to our FX exposure of US$ 1.9 billion in Brazil, with approximately 4.1%

carry cost, and (ii) hedging carry costs related to commodities. We did not incur hedging costs related to FX exposure in Argentina this

quarter; however, we still maintain an FX exposure of US$ 312.4 million in the country. |

| · | Losses on non-derivative instruments of R$ (161.5)

million, driven by losses on third-party payables and intercompany balance sheet consolidation. |

| · | Taxes on financial transactions of R$ (45.7) million. |

| · | Other financial expenses of R$ (219.5)

million, mainly explained by accruals on legal contingencies, letter of credit expenses, pension plan expenses and bank fees. |

| · | Non-cash financial expense of R$ (99.4)

million resulting from the adoption of Hyperinflation Accounting in Argentina. |

| Net finance results |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| R$ million |

| |

|

|

|

|

| Interest income |

421.0 |

502.5 |

1,286.9 |

1,603.4 |

| Interest expenses |

(631.4) |

(487.5) |

(1,907.8) |

(1,536.4) |

| Gains/(losses) on derivative instruments |

(469.4) |

(170.3) |

(1,571.3) |

(513.5) |

| Gains/(losses) on non-derivative instruments |

(172.2) |

(161.5) |

(769.6) |

(252.4) |

| Taxes on financial transactions |

(43.1) |

(45.7) |

(149.4) |

(146.6) |

| Other net financial income/(expenses) |

(88.8) |

(219.5) |

(336.6) |

(614.5) |

| Hyperinflation Argentina |

145.9 |

(99.4) |

538.6 |

(243.6) |

| |

|

|

|

|

| Net finance results |

(837.9) |

(681.5) |

(2,909.2) |

(1,703.7) |

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 13 | |

| | |

DEBT

BREAKDOWN

| Debt breakdown |

December 31, 2023 |

September 30, 2024 |

| R$ million |

Current |

Non-current |

Total |

Current |

Non-current |

Total |

| |

|

|

|

|

|

|

| Local Currency |

1,043.4 |

1,571.8 |

2,615.2 |

934.5 |

1,565.4 |

2,499.9 |

| Foreign Currency |

254.7 |

631.2 |

885.9 |

276.6 |

603.8 |

880.4 |

| Consolidated Debt |

1,298.1 |

2,203.0 |

3,501.1 |

1,211.1 |

2,169.2 |

3,380.3 |

| |

|

|

|

|

|

|

| Cash and Cash Equivalents less Bank Overdrafts |

- |

- |

16,059.0 |

- |

- |

19,784.4 |

| Current Investment Securities |

- |

- |

277.2 |

- |

- |

1,154.7 |

| |

|

|

|

|

|

|

| Net debt/(cash) |

|

|

(12,835.1) |

|

|

(17,558.8) |

PROVISION

FOR INCOME TAX & SOCIAL CONTRIBUTION

The table below demonstrates the income tax and social contribution provision.

| Income tax and social contribution |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| R$ million |

| |

|

|

|

|

| Profit before tax |

4,059.7 |

4,669.6 |

10,309.3 |

12,576.7 |

| |

|

|

|

|

| Adjustment on taxable basis |

|

|

|

|

| Non-taxable other income |

(131.5) |

(122.5) |

(622.4) |

(376.4) |

| Government grants related to sales taxes |

(769.2) |

(27.8) |

(2,173.4) |

(27.8) |

| Share of results of joint ventures |

(1.4) |

(36.8) |

15.2 |

(1.8) |

| Expenses not deductible |

11.9 |

15.1 |

31.5 |

49.9 |

| Worldwide taxation |

161.9 |

36.0 |

422.6 |

(30.1) |

| Total |

3,331.4 |

4,533.6 |

7,982.8 |

12,190.5 |

| Aggregated weighted nominal tax rate |

29.6% |

27.2% |

29.0% |

28.6% |

| Taxes – nominal rate |

(987.7) |

(1,233.9) |

(2,312.4) |

(3,483.1) |

| |

|

|

|

|

| Adjustment on tax expense |

|

|

|

|

| Income tax incentive |

29.6 |

75.3 |

77.3 |

399.5 |

| Tax benefit - interest on shareholders' equity |

1,082.2 |

363.7 |

2,758.9 |

874.7 |

| Tax benefit - amortization on tax books |

4.3 |

0.9 |

12.9 |

2.7 |

| Withholding income tax |

(122.1) |

(155.0) |

(222.8) |

(564.9) |

| Argentina's hyperinflation effect |

(152.4) |

(0.3) |

(410.0) |

57.2 |

| Recognition/(write-off) of deferred charges on tax losses |

123.5 |

(73.8) |

29.1 |

(105.2) |

| Other tax adjustments |

(22.1) |

(80.2) |

189.8 |

64.7 |

| |

|

|

|

|

| Income tax and social contribution expense |

(44.7) |

(1,103.3) |

122.7 |

(2,754.4) |

| Effective tax rate |

1.1% |

23.6% |

-1.2% |

21.9% |

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 14 | |

| | |

SHAREHOLDING

STRUCTURE

The table below summarizes Ambev S.A.’s shareholding structure

as of September 30, 2024.

| Ambev S.A.'s shareholding structure |

| |

ON |

% |

| Anheuser-Busch InBev |

9,729,336,918 |

61.9% |

| FAHZ |

1,609,987,301 |

10.2% |

| Market |

4,388,851,573 |

27.9% |

| Outstanding |

15,728,175,792 |

100.0% |

| Treasury |

29,481,544 |

|

| TOTAL |

15,757,657,336 |

|

| Free float B3 |

2,904,907,973 |

18.5% |

| Free float NYSE |

1,483,943,600 |

9.4% |

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 15 | |

| | |

FINANCIAL

REPORTING IN HYPERINFLATIONARY ECONOMIES - ARGENTINA

Following the categorization of Argentina as a country with a three-year

cumulative inflation rate greater than 100%, the country is considered highly inflationary in accordance with IFRS.

Consequently, starting from 3Q18, we have been reporting the operations

of our Argentinean affiliates applying Hyperinflation Accounting. The IFRS and CPC rules (IAS 29/CPC 42) require the results of our operations

in hyperinflationary economies to be reported restating the year-to-date results adjusting for the change in the general purchasing power

of the local currency, using official indices, before converting the local amounts at the closing rate of the period (i.e., September

30, 2024 closing rate for 3Q24 and YTD24 results).

The YTD24 Hyperinflation Accounting adjustment results from the

combined effect of (i) the indexation to reflect changes in purchasing power on the YTD24 results against a dedicated line in the finance

results; and (ii) the difference between the translation of the YTD24 results at the closing exchange rate of September 30, 2024, and

the translation using the average year to date rate on the reported period, as applicable to non-inflationary economies.

The impacts in 3Q23, YTD23, 3Q24 and YTD24 on Net Revenue and

Normalized EBITDA were as follows:

| Impact of Hyperinflation Accounting (IAS 29/CPC42) |

|

|

|

|

| Revenue |

|

|

|

|

| R$ million |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| Indexation(1) |

1,101.4 |

525.7 |

2,031.1 |

1,344.1 |

| Currency(2) |

(1,021.2) |

(379.2) |

(2,161.6) |

(199.0) |

| Total Impact |

80.3 |

146.5 |

(130.5) |

1,145.0 |

| Normalized EBITDA |

|

|

|

|

| R$ million |

3Q23 |

3Q24 |

YTD23 |

YTD24 |

| Indexation(1) |

359.6 |

68.9 |

642.0 |

238.7 |

| Currency(2) |

(345.1) |

(61.4) |

(775.6) |

(30.0) |

| Total Impact |

14.5 |

7.5 |

(133.6) |

208.7 |

| |

|

|

|

|

| ARS/BRL average rate |

- |

- |

49.1730 |

172.0448 |

| ARS/BRL closing rate |

69.8873 |

178.1149 |

69.8873 |

178.1149 |

| (1) | Indexation calculated at each period’s closing exchange rate. |

| (2) | Currency impact calculated as the difference between converting the

Argentinean Peso (ARS) reported amounts at the closing exchange rate compared to the average exchange rate of each period. |

Furthermore, IAS 29 requires adjusting non-monetary assets and

liabilities on the balance sheet of our operations in hyperinflationary economies for cumulative inflation. The resulting effect from

the adjustment until December 31, 2017 was reported in Equity and, the effect from the adjustment from this date on, in a dedicated account

in the finance results, reporting deferred taxes on such adjustments, when applicable.

In 3Q24, the transition to Hyperinflation Accounting in accordance

with the IFRS rules resulted in (i) a negative adjustment of R$99.4 million reported in the finance results, (ii) a negative impact on

the Profit of R$ 322.7 million, (iii) a negative impact on the Normalized Profit of R$ 322.7 million, and (iv) a negative impact of R$

0.02 on EPS, as well as on Normalized EPS.

In YTD24, the consequences of the transition were (i) a negative

adjustment of R$ 243.6 million reported in the finance results, (ii) a negative impact on Profit of R$ 1,060.0 million, (iii) a negative

impact on Normalized Profit of R$ 1,059.6 million, and (iv) a negative impact of R$ 0.06 on EPS, as well as on Normalized EPS.

The Q3 results are calculated by deducting from the YTD results

the HY results as published. Consequently, LAS and consolidated 3Q24, 3Q23, YTD24 and YTD23 results are impacted by the adjustment of

HY results for the cumulative inflation between reporting periods, as well as by the translation of HY results at the YTD closing exchange

rate, of September 30, as follows:

| | |

ambev.com.br | Press Release – October 31st, 2024 |

Page | 16 | |

| | |

| LAS - 6M As Reported |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% Organic |

| Net revenue |

12,295.9 |

13,292.7 |

(10,801.2) |

467.0 |

12,392.4 |

3.8% |

| COGS |

(6,021.6) |

(8,479.4) |

6,385.5 |

(161.5) |

(6,775.8) |

2.7% |

| COGS excl. deprec. & amort. |

(5,398.7) |

(7,743.3) |

5,728.6 |

(39.1) |

(6,122.1) |

0.7% |

| Gross profit |

6,274.3 |

4,813.3 |

(4,415.7) |

305.4 |

5,616.6 |

4.9% |

| SG&A excl. deprec. & amort. |

(2,986.8) |

(4,081.1) |

3,139.9 |

(130.7) |

(3,277.7) |

4.4% |

| SG&A deprec. & amort. |

(290.9) |

(391.8) |

327.4 |

(42.1) |

(319.9) |

14.5% |

| SG&A total |

(3,277.7) |

(4,472.9) |

3,467.3 |

(172.8) |

(3,597.6) |

5.3% |

| Other operating income/(expenses) |

31.9 |

(42.6) |

(12.1) |

32.8 |

18.8 |

102.8% |

| Normalized Operating Profit |

3,028.5 |

297.9 |

(960.6) |

165.4 |

2,037.8 |

5.5% |

| Normalized EBITDA |

3,942.3 |

1,425.8 |

(1,944.8) |

330.0 |

3,011.4 |

8.4% |

| LAS - 6M Recalculated at YTD Exchange Rates |

YTD23 |

Scope |

Currency Translation |

Organic Growth |

YTD24 |

% Organic |

| Net revenue |

12,434.0 |

11,147.3 |

(8,601.4) |

467.0 |

12,584.9 |

- |

| COGS |

(6,079.7) |

(7,339.8) |

5,200.2 |

(161.5) |

(6,879.6) |

- |

| COGS excl. deprec. & amort. |

(5,449.5) |

(6,730.8) |

4,674.7 |

(39.1) |

(6,214.3) |

- |

| Gross profit |

6,354.3 |

3,807.5 |

(3,401.2) |

305.4 |

5,705.3 |

- |

| SG&A excl. deprec. & amort. |

(3,021.5) |

(3,475.3) |

2,514.0 |

(130.7) |

(3,332.4) |

- |

| SG&A deprec. & amort. |

(294.2) |

(330.4) |

263.7 |

(42.1) |

(325.5) |

- |

| SG&A total |

(3,315.7) |

(3,805.6) |

2,777.7 |

(172.8) |

(3,657.9) |

- |