--12-310002020455falseQ3Unlimited0002020455us-gaap:FairValueInputsLevel2Member2024-09-300002020455us-gaap:CommonStockMember2024-05-310002020455us-gaap:FairValueInputsLevel1Member2024-09-3000020204552024-09-300002020455eth:GrayscaleEthereumTrustMember2024-07-180002020455us-gaap:CommonStockMember2024-05-312024-05-310002020455eth:InvestmentInEthereumMember2024-09-300002020455eth:SponsorMember2024-05-310002020455eth:SponsorMember2024-07-232024-09-300002020455eth:NonSponsorPaidExpensesMembersrt:MinimumMember2024-07-232024-09-300002020455us-gaap:FairValueInputsLevel3Member2024-09-300002020455eth:CoinbaseIncorporationMembereth:SponsorMember2024-09-3000020204552024-07-230002020455eth:SponsorMember2024-07-162024-07-160002020455eth:SponsorMembereth:FirstSixMonthsMember2024-07-232024-07-230002020455eth:GrayscaleEthereumTrustMember2024-07-230002020455eth:GrayscaleEthereumTrustMember2024-09-300002020455us-gaap:SubsequentEventMember2024-10-2800020204552024-10-280002020455us-gaap:SubsequentEventMember2024-10-282024-10-280002020455srt:MaximumMembereth:SponsorMember2024-07-232024-09-3000020204552024-07-232024-09-300002020455eth:SponsorMember2024-07-232024-07-230002020455eth:InvestmentMember2024-09-300002020455eth:SponsorMember2024-09-300002020455eth:PriorToEndOfSixMonthPeriodMembereth:SponsorMember2024-07-232024-07-230002020455eth:SponsorMember2024-05-312024-05-3100020204552024-07-22eth:Etherxbrli:purexbrli:shareseth:Ethereumeth:Rightiso4217:USD

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2024

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ______ to ______ |

Commission File Number 001-42184

Grayscale Ethereum Mini Trust (ETH)

SPONSORED BY GRAYSCALE INVESTMENTS, LLC

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

Delaware |

99-6447880 |

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

c/o Grayscale Investments, LLC

290 Harbor Drive, 4th Floor

Stamford, Connecticut 06902

(Address of Principal Executive Offices) (Zip Code)

(212) 668-1427

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Grayscale Ethereum Mini Trust (ETH) Shares |

ETH |

NYSE Arca, Inc. |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

|

|

|

|

|

Non-accelerated filer |

☒ |

|

Smaller reporting company |

☒ |

|

|

|

|

|

|

|

|

Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of Shares of the registrant outstanding as of October 28, 2024: 418,788,500

Grayscale® ETHEREUM MINI Trust (ETH)

Table of Contents

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking statements” with respect to the financial conditions, results of operations, plans, objectives, future performance and business of Grayscale Ethereum Mini Trust (ETH) (the “Trust”). Statements preceded by, followed by or that include words such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other than statements of historical fact) included in this Quarterly Report that address activities, events or developments that will or may occur in the future, including such matters as changes in market prices and conditions, the Trust’s operations, the plans of Grayscale Investments, LLC (the “Sponsor”) and references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially from such statements. These statements are based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including, but not limited to, those described in “Risk Factors” of our Registration Statement on Form S-1 (File No. 333-278878), filed with the Securities and Exchange Commission (the “SEC”) on July 18, 2024 (as amended and supplemented from time to time, the “Registration Statement”) and in “Part II, Item 1A. Risk Factors” herein. Forward-looking statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made and neither the Trust nor the Sponsor is under a duty or undertakes an obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, other than as required by applicable laws. Investors are therefore cautioned against relying on forward-looking statements.

Unless otherwise stated or the context otherwise requires, the terms “we,” “our” and “us” in this Quarterly Report refer to the Sponsor acting on behalf of the Trust.

A glossary of industry and other defined terms is included in this Quarterly Report, beginning on page 29.

INDUSTRY AND MARKET DATA

Although we are responsible for all disclosure contained in this Quarterly Report on Form 10-Q, in some cases we have relied on certain market and industry data obtained from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications in conjunction with our assumptions regarding the Ethereum industry and market. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Forward-Looking Statements”, “Risk Factors” in the Registration Statement and “Part II, Item 1A. Risk Factors” in this Quarterly Report on Form 10-Q.

PART I – FINANCIAL INFORMATION:

Item 1. Financial Statements (Unaudited)

GRAYSCALE ETHEREUM MINI TRUST (ETH)

STATEMENT OF ASSETS AND LIABILITIES (UNAUDITED)

(Amounts in thousands, except Share and per Share amounts)

|

|

|

|

|

|

|

September 30, 2024(1) |

|

Assets: |

|

|

|

Investment in Ether, at fair value (cost $1,301,240 as of September 30, 2024) |

|

$ |

1,015,027 |

|

Total assets |

|

$ |

1,015,027 |

|

Liabilities: |

|

|

|

Sponsor’s Fee payable, related party |

|

$ |

- |

|

Total liabilities |

|

|

- |

|

Net assets |

|

$ |

1,015,027 |

|

Shares issued and outstanding, no par value (unlimited Shares authorized) |

|

|

415,188,500 |

|

Principal market net asset value per Share |

|

$ |

2.44 |

|

(1)No comparative financial statements have been provided as the Trust’s operations commenced on July 23, 2024. Prior to the commencement of operations on July 23, 2024, the Sponsor redeemed the initial seed capital of 10,000 shares for $100,000.

See accompanying notes to the unaudited financial statements.

GRAYSCALE ETHEREUM MINI TRUST (ETH)

SCHEDULE OF INVESTMENT (UNAUDITED)

(Amounts in thousands, except quantity of Ether and percentages)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

September 30, 2024(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quantity of

Ether |

|

|

Cost |

|

|

Fair Value |

|

|

% of Net

Assets |

|

Investment in Ether |

|

|

391,232.97302030 |

|

|

$ |

1,301,240 |

|

|

$ |

1,015,027 |

|

|

|

100 |

% |

Total Investment |

|

|

|

|

$ |

1,301,240 |

|

|

$ |

1,015,027 |

|

|

|

100 |

% |

Net assets |

|

|

|

|

$ |

1,301,240 |

|

|

$ |

1,015,027 |

|

|

|

100 |

% |

(1)No comparative financial statements have been provided as the Trust’s operations commenced on July 23, 2024. Prior to the commencement of operations on July 23, 2024, the Sponsor redeemed the initial seed capital of 10,000 shares for $100,000.

See accompanying notes to the unaudited financial statements.

GRAYSCALE ETHEREUM MINI TRUST (ETH)

STATEMENT OF OPERATIONS (UNAUDITED)

(Amounts in thousands)

|

|

|

|

|

|

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024(1) |

|

Investment income: |

|

|

|

Investment income |

|

$ |

- |

|

Expenses: |

|

|

|

Sponsor’s Fee, related party |

|

|

276 |

|

Gross expenses |

|

|

276 |

|

Sponsor’s Fee Waiver, related party |

|

|

(276 |

) |

Net expenses |

|

|

- |

|

Net investment loss |

|

|

- |

|

Net realized and unrealized loss from: |

|

|

|

Net realized loss on investment in Ether sold to pay expenses |

|

|

- |

|

Net realized loss on investment in Ether sold for redemption of Shares |

|

|

(3,536 |

) |

Net change in unrealized depreciation on investment in Ether |

|

|

(286,213 |

) |

Net realized and unrealized loss on investment |

|

|

(289,749 |

) |

Net decrease in net assets resulting from operations |

|

$ |

(289,749 |

) |

(1)No comparative financial statements have been provided as the Trust’s operations commenced on July 23, 2024. Prior to the commencement of operations on July 23, 2024, the Sponsor redeemed the initial seed capital of 10,000 shares for $100,000.

See accompanying notes to the unaudited financial statements.

GRAYSCALE ETHEREUM MINI TRUST (ETH)

STATEMENT OF CHANGES IN NET ASSETS (UNAUDITED)

(Amounts in thousands, except change in Shares outstanding)

|

|

|

|

|

|

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024(1) |

|

Decrease in net assets from operations: |

|

|

|

Net investment loss |

|

$ |

- |

|

Net realized loss on investment in Ether sold to pay expenses |

|

|

- |

|

Net realized loss on investment in Ether sold for redemption of Shares |

|

|

(3,536 |

) |

Net change in unrealized depreciation on investment in Ether |

|

|

(286,213 |

) |

Net decrease in net assets resulting from operations |

|

|

(289,749 |

) |

Increase in net assets from capital share transactions: |

|

|

|

Shares issued |

|

|

310,876 |

|

Shares issued from Initial Distribution(2) |

|

|

1,010,935 |

|

Shares redeemed |

|

|

(17,035 |

) |

Net increase in net assets resulting from capital share transactions |

|

|

1,304,776 |

|

Total increase in net assets from operations and capital share transactions |

|

|

1,015,027 |

|

Net assets: |

|

|

|

Beginning of period |

|

|

- |

|

End of period |

|

$ |

1,015,027 |

|

Change in Shares outstanding: |

|

|

|

Shares outstanding at beginning of period |

|

|

- |

|

Shares issued |

|

|

111,430,000 |

|

Shares issued from Initial Distribution(2) |

|

|

310,158,500 |

|

Shares redeemed |

|

|

(6,400,000 |

) |

Net increase in Shares |

|

|

415,188,500 |

|

Shares outstanding at end of period |

|

|

415,188,500 |

|

(1)No comparative financial statements have been provided as the Trust’s operations commenced on July 23, 2024. Prior to the commencement of operations on July 23, 2024, the Sponsor redeemed the initial seed capital of 10,000 shares for $100,000.

(2)Represents the impact of the Initial Distribution of 292,262.98913350 Ether, with a value of approximately $1,010.9 million from Grayscale Ethereum Trust (ETH), completed on July 23, 2024, as discussed in Note 4.

See accompanying notes to the unaudited financial statements.

GRAYSCALE ETHEREUM MINI TRUST (ETH)

STATEMENT OF CASH FLOWS (UNAUDITED)

(Amounts in thousands)

|

|

|

|

|

|

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024(1) |

|

Cash used in operating activities |

|

|

|

Net decrease in net assets resulting from operations |

|

$ |

(289,749 |

) |

Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash used in operating activities: |

|

|

|

Purchases of Ether |

|

$ |

(310,876 |

) |

Proceeds from Ether sold to pay redemptions and expenses |

|

|

17,035 |

|

Net realized (gain) loss |

|

|

3,536 |

|

Net change in unrealized depreciation |

|

|

286,213 |

|

Change in operating assets and liabilities: |

|

|

- |

|

Sponsor’s Fee payable |

|

|

- |

|

Net cash used in operating activities |

|

$ |

(293,841 |

) |

|

|

|

|

Cash provided by financing activities |

|

|

|

Proceeds from issuance of capital shares |

|

$ |

310,876 |

|

Payments for capital shares redeemed |

|

|

(17,035 |

) |

Net cash provided by financing activities |

|

$ |

293,841 |

|

|

|

|

|

Cash |

|

|

|

Net increase in cash |

|

$ |

- |

|

Cash, beginning of period |

|

|

- |

|

Cash, end of period |

|

$ |

- |

|

|

|

|

|

Supplemental disclosure of noncash financing activities |

|

|

|

Transfer of Ether from Initial Distribution(2) |

|

$ |

1,010,935 |

|

|

|

|

|

(1)No comparative financial statements have been provided as the Trust’s operations commenced on July 23, 2024. Prior to the commencement of operations on July 23, 2024, the Sponsor redeemed the initial seed capital of 10,000 shares for $100,000.

(2)Represents the impact of the Initial Distribution of 292,262.98913350 Ether, with a value of approximately $1,010.9 million from Grayscale Ethereum Trust (ETH), completed on July 23, 2024, as discussed in Note 4.

See accompanying notes to the unaudited financial statements.

GRAYSCALE ETHEREUM MINI TRUST (ETH)

NOTES TO THE UNAUDITED FINANCIAL STATEMENTS

1. Organization

Grayscale Ethereum Mini Trust (ETH) (the “Trust”) is a Delaware Statutory Trust that was formed on April 23, 2024 and commenced operations on July 23, 2024. In general, the Trust holds Ethereum tokens (“Ether”) and, from time to time, issues common units of fractional undivided beneficial interest (“Shares”) in exchange for Ether. On July 18, 2024, the Securities and Exchange Commission (the “SEC”) approved an application under Rule 19b-4 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) by NYSE Arca, Inc. (“NYSE Arca”) to list the Shares of the Trust, which began trading on NYSE Arca on July 23, 2024, following the effectiveness of the Registration Statement. As of July 23, 2024, the Trust is an SEC reporting company with its Shares registered pursuant to Section 12(b) of the Exchange Act.

On May 31, 2024, Grayscale Investments, LLC (“Grayscale” or the “Sponsor”) purchased 10,000 Shares (the “Seed Shares”) for $100,000 ($10.00 per share). The Sponsor did not receive from the Trust, or any of its affiliates, any fee or other compensation in connection with the initial seed sale. Subsequently, on July 16, 2024, the Sponsor caused the Trust to distribute $100,000 to the Sponsor in redemption of the 10,000 Shares held by the Sponsor.

On July 22, 2024, in connection with the approval of the 19b-4 Application on July 18, 2024 and the effectiveness of the registration statement on Form S-1, as amended, the Sponsor authorized the commencement of a redemption program. Effective July 23, 2024, the Trust creates and redeems Shares at such times and for such periods as determined by the Sponsor, but only in one or more whole “Baskets.” A Basket equals 10,000 Shares. The creation of a Basket requires the delivery to the Trust of the amount of Ether represented by one Share immediately prior to such creation multiplied by 10,000. The redemption of a Basket requires distribution by the Trust of the amount of Ether represented by one Share immediately prior to such redemption multiplied by 10,000. The Trust may from time to time halt creations and redemptions for a variety of reasons, including in connection with forks, airdrops and other similar occurrences.

Prior to July 23, 2024, the Trust had no operations other than matters relating to the sale, issuance and redemption of the Seed Shares.

The Trust’s investment objective is for the value of the Shares (based on Ether per Share) to reflect the value of Ether held by the Trust, less the Trust’s expenses and other liabilities. The Trust may also receive Incidental Rights and/or IR Virtual Currency as a result of the Trust’s investment in Ether, in accordance with the terms of the Trust Agreement.

Incidental Rights are rights to claim, or otherwise establish dominion and control over, any virtual currency or other asset or right, which rights are incident to the Trust’s ownership of Ether and arise without any action of the Trust, or of the Sponsor or Trustee on behalf of the Trust; IR Virtual Currency is any virtual currency tokens, or other asset or right, received by the Trust through the exercise (subject to the applicable provisions of the Trust Agreement) of any Incidental Right. The Sponsor has committed to cause the Trust not to take any Affirmative Action to acquire any Incidental Rights or IR Virtual Currency, thereby irrevocably abandoning any Incidental Rights and IR Virtual Currency to which the Trust may become entitled in the future. Because the Sponsor has now committed to causing the Trust to irrevocably abandon all Incidental Rights and IR Virtual Currency to which the Trust otherwise would become entitled in the future, and causing the Trust not to take any Affirmative Actions, the Trust will not receive any direct or indirect consideration for the Incidental Rights or IR Virtual Currency and thus the value of the Shares will not reflect the value of the Incidental Rights or IR Virtual Currency. In addition, in the event the Sponsor seeks to change the Trust’s policy with respect to Incidental Rights or IR Virtual Currency, an application would need to be filed with the SEC by NYSE Arca seeking approval to amend its listing rules to permit the Trust to distribute the Incidental Rights or IR Virtual Currency in-kind to an agent of the shareholders for resale by such agent.

Grayscale Investments, LLC acts as the Sponsor of the Trust and is a wholly owned subsidiary of Digital Currency Group, Inc. (“DCG”). The Sponsor is responsible for the day-to-day administration of the Trust pursuant to the provisions of the Trust Agreement. Grayscale is responsible for preparing and providing annual and quarterly reports on behalf of the Trust to investors and is also responsible for selecting and monitoring the Trust’s service providers. As partial consideration for the Sponsor’s services, the Trust pays Grayscale a Sponsor’s Fee as discussed in Note 7. The Sponsor also acts as the sponsor and manager of other investment products including Grayscale Aave Trust (AAVE), Grayscale Avalanche Trust (AVAX), Grayscale Basic Attention Token Trust (BAT) (OTCQB: GBAT), Grayscale Bitcoin Trust (BTC) (NYSE Arca: GBTC), Grayscale Bitcoin Cash Trust (BCH) (OTCQX: BCHG), Grayscale Bitcoin Mini Trust (BTC) (NYSE Arca: BTC), Grayscale Bittensor Trust (TAO), Grayscale Chainlink Trust (LINK) (OTCQX: GLNK), Grayscale Decentraland Trust (MANA) (OTCQX: MANA), Grayscale Ethereum Classic Trust (ETC) (OTCQX: ETCG), Grayscale Ethereum Trust (ETH) (NYSE Arca: ETHE), Grayscale Filecoin Trust (FIL) (OTC Markets: FILG), Grayscale Horizen Trust (ZEN) (OTCQX: HZEN), Grayscale Litecoin Trust (LTC) (OTCQX: LTCN), Grayscale Livepeer Trust (LPT) (OTCQX: GLIV), Grayscale MakerDao Trust (MKR), Grayscale NEAR Trust (NEAR), Grayscale Solana Trust (SOL) (OTCQX: GSOL), Grayscale Stacks Trust (STX), Grayscale Stellar Lumens Trust (XLM) (OTCQX: GXLM), Grayscale Sui Trust (SUI), Grayscale XRP Trust, Grayscale Zcash Trust

(ZEC) (OTCQX: ZCSH), Grayscale Decentralized AI Fund LLC, Grayscale Decentralized Finance (DeFi) Fund LLC (OTCQB: DEFG), Grayscale Digital Large Cap Fund LLC (OTCQX: GDLC), and Grayscale Smart Contract Platform Ex Ethereum (ETH) Fund LLC, each of which is an affiliate of the Trust. The following investment products sponsored or managed by the Sponsor are SEC reporting companies with their shares registered pursuant to Section 12(g) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”): Grayscale Bitcoin Cash Trust (BCH), Grayscale Ethereum Classic Trust (ETC), Grayscale Horizen Trust (ZEN), Grayscale Litecoin Trust (LTC), Grayscale Stellar Lumens Trust (XLM), Grayscale Zcash Trust (ZEC), and Grayscale Digital Large Cap Fund LLC. The following investment products sponsored by the Sponsor are also SEC reporting companies with their shares registered pursuant to Section 12(b) of the Exchange Act: Grayscale Bitcoin Trust (BTC), Grayscale Ethereum Trust (ETH), and Grayscale Bitcoin Mini Trust (BTC). Grayscale Advisors, LLC, a Registered Investment Advisor and an affiliate of the Sponsor, is the advisor to the Grayscale Future of Finance (NYSE Arca: GFOF) product.

Authorized Participants of the Trust are the only entities who may place orders to create or redeem Baskets. The Sponsor, on behalf of the Trust, and the Transfer Agent entered into Participant Agreements with a number of unaffiliated Authorized Participants in connection with the approval of NYSE Arca’s application under Rule 19b-4 of the Exchange Act, and the Trust has also since engaged other Authorized Participants. Additional Authorized Participants may be added at any time, subject to the discretion of the Sponsor.

Liquidity Providers facilitate the purchase and sale of Ether in connection with cash orders for creations or redemptions of Baskets. The Liquidity Providers with which Grayscale Investments, LLC, acting in its capacity as the “Liquidity Engager,” will engage in Ether transactions are third parties that are not affiliated with the Sponsor or the Trust and are not acting as agents of the Trust, the Sponsor, or any Authorized Participant, and all transactions will be done on an arms-length basis. Except for the contractual relationships between each Liquidity Provider and Grayscale Investments, LLC in its capacity as the Liquidity Engager, there is no contractual relationship between each Liquidity Provider and the Trust, the Sponsor, or any Authorized Participant. The Liquidity Engager may engage additional Liquidity Providers who are unaffiliated with the Trust in the future.

The Trust, the Sponsor and Coinbase, Inc., the prime broker of the Trust (“Coinbase” or the “Prime Broker”), on behalf of itself and as agent for Coinbase Custody Trust Company, LLC (“Coinbase Custody” or the “Custodian”) and Coinbase Credit, Inc. (“Coinbase Credit” and, collectively with Coinbase and Coinbase Custody, the “Coinbase Entities”), entered into the Coinbase Prime Broker Agreement governing the Trust’s and the Sponsor’s use of the Custodial and Prime Broker Services provided by the Custodian and the Prime Broker. The Prime Broker Agreement establishes the rights and responsibilities of the Custodian, the Prime Broker, the Sponsor and the Trust with respect to the Trust’s Ether which is held in accounts maintained and operated by the Custodian, as a fiduciary with respect to the Trust’s assets, and the Prime Broker (together with the Custodian, the “Custodial Entities”) on behalf of the Trust. The Custodian is responsible for safeguarding the Ether held by the Trust, and holding the private key(s) that provide access to the Trust’s digital wallets and vaults.

The transfer agent for the Trust (the “Transfer Agent”) is The Bank of New York Mellon. The responsibilities of the Transfer Agent are to (1) facilitate the issuance and redemption of shares of the Trust; (2) respond to correspondence by Trust shareholders and others relating to its duties; (3) maintain shareholder accounts; and (4) make periodic reports to the Trust.

The administrator for the Trust (the “Administrator”) is BNY Mellon Asset Servicing, a division of The Bank of New York Mellon. BNY Mellon Asset Servicing provides administration and accounting services to the Trust. The Administrator’s fees are paid on behalf of the Trust by the Sponsor.

The marketing agent for the Trust (the “Marketing Agent”) is Foreside Fund Services, LLC. Effective July 22, 2024, the Marketing Agent provides the following services to the Sponsor: (i) assist the Sponsor in facilitating Participation Agreements between and among Authorized Participants, the Sponsor, on behalf of the Trust, and the Transfer Agent; (ii) provide prospectuses to Authorized Participants; (iii) work with the Transfer Agent to review and approve orders placed by the Authorized Participants and transmitted to the Transfer Agent; (iv) review and file applicable marketing materials with FINRA and (v) maintain, reproduce and store applicable books and records.

On July 18, 2024, the SEC approved an application under Rule 19b-4 of the Exchange Act by NYSE Arca to list the Shares of the Trust. Shares of the Trust began trading on NYSE Arca on July 23, 2024, following the effectiveness of the Registration Statement. The Trust’s trading symbol on NYSE Arca is “ETH” and the CUSIP number for its Shares is 38964R104.

2. Summary of Significant Accounting Policies

In the opinion of management of the Sponsor of the Trust, all adjustments (which include normal recurring adjustments) necessary to present fairly the financial position as of September 30, 2024 and results of operations for the period from July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024 have been made. As the Trust had no operations other than matters relating to the sale, issuance and redemption of the Seed Shares prior to July 23, 2024, the results of operations for the period presented are not necessarily indicative of the results of operations expected for the full period. These unaudited financial statements should be read in conjunction with the audited financial statements as of May 31, 2024 included in the Registration Statement.

The following is a summary of significant accounting policies followed by the Trust:

The financial statements have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). The Trust qualifies as an investment company for accounting purposes pursuant to the accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services—Investment Companies. The Trust uses fair value as its method of accounting for Ether in accordance with its classification as an investment company for accounting purposes. The Trust is not a registered investment company under the Investment Company Act of 1940. U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates and these differences could be material.

The Trust conducts its transactions in Ether, including receiving Ether for the creation of Shares and delivering Ether for the redemption of Shares and for the payment of the Sponsor’s Fee.

Cash and Cash Equivalents

Generally, the Trust does not intend to hold cash, except in connection with cash orders for creations or redemptions of Baskets. Cash includes non-interest bearing non-restricted cash with one institution. Cash in a bank deposit account, at times, may exceed U.S. federally insured limits. The Trust has not experienced any losses in such accounts and does not believe it is exposed to any significant credit risk on such bank deposits.

Principal Market and Fair Value Determination

To determine which market is the Trust’s principal market (or in the absence of a principal market, the most advantageous market) for purposes of calculating the Trust’s net asset value in accordance with U.S. GAAP (“Principal Market NAV”), the Trust follows ASC Topic 820-10, Fair Value Measurement, which outlines the application of fair value accounting. ASC 820-10 determines fair value to be the price that would be received for Ether in a current sale, which assumes an orderly transaction between market participants on the measurement date. ASC 820-10 requires the Trust to assume that Ether is sold in its principal market to market participants or, in the absence of a principal market, the most advantageous market. Market participants are defined as buyers and sellers in the principal or most advantageous market that are independent, knowledgeable, and willing and able to transact.

The Trust only receives Ether in connection with a creation order from the Authorized Participant (or a Liquidity Provider) and does not itself transact on any Digital Asset Markets. Therefore, the Trust looks to market-based volume and level of activity for Digital Asset Markets. The Authorized Participant(s), or a Liquidity Provider, may transact in a Brokered Market, a Dealer Market, Principal-to-Principal Markets and Exchange Markets (referred to as “Trading Platform Markets” in this Quarterly Report), each as defined in the FASB ASC Master Glossary (collectively, “Digital Asset Markets”).

In determining which of the eligible Digital Asset Markets is the Trust’s principal market, the Trust reviews these criteria in the following order:

First, the Trust reviews a list of Digital Asset Markets that maintain practices and policies designed to comply with anti-money laundering (“AML”) and know-your-customer (“KYC”) regulations, and non-Digital Asset Trading Platform Markets that the Trust reasonably believes are operating in compliance with applicable law, including federal and state licensing requirements, based upon information and assurances provided to it by each market.

Second, the Trust sorts these Digital Asset Markets from high to low by market-based volume and level of activity of Ether traded on each Digital Asset Market in the trailing twelve months.

Third, the Trust then reviews pricing fluctuations and the degree of variances in price on Digital Asset Markets to identify any material notable variances that may impact the volume or price information of a particular Digital Asset Market.

Fourth, the Trust then selects a Digital Asset Market as its principal market based on the highest market-based volume, level of activity and price stability in comparison to the other Digital Asset Markets on the list. Based on information reasonably available to the Trust, Trading Platform Markets have the greatest volume and level of activity for the asset. The Trust therefore looks to accessible Trading Platform Markets as opposed to the Brokered Market, Dealer Market and Principal-to-Principal Markets to determine its principal market. As a result of the aforementioned analysis, a Trading Platform Market has been selected as the Trust’s principal market.

The Trust determines its principal market (or in the absence of a principal market the most advantageous market) annually and conducts a quarterly analysis to determine (i) if there have been recent changes to each Digital Asset Market’s trading volume and level of activity in the trailing twelve months, (ii) if any Digital Asset Markets have developed that the Trust has access to, or (iii) if recent changes to each Digital Asset Market’s price stability have occurred that would materially impact the selection of the principal market and necessitate a change in the Trust’s determination of its principal market.

The cost basis of Ether received in connection with a creation order is recorded by the Trust at the fair value of Ether at 4:00 p.m., New York time, on the creation date for financial reporting purposes. The cost basis recorded by the Trust may differ from proceeds collected by the Authorized Participant from the sale of the corresponding Shares to investors.

Investment Transactions and Revenue Recognition

The Trust considers investment transactions to be the receipt of Ether for Share creations and the delivery of Ether for Share redemptions, or for payment of expenses in Ether. The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as net change in unrealized appreciation or depreciation on investments. Realized gains and losses are calculated using the specific identification method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Sponsor’s Fee in Ether.

Fair Value Measurement

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., the ‘exit price’) in an orderly transaction between market participants at the measurement date.

U.S. GAAP utilizes a fair value hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are those that market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Trust. Unobservable inputs reflect the Trust’s assumptions about the inputs market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The fair value hierarchy is categorized into three levels based on the inputs as follows:

•Level 1 – Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Trust has the ability to access. Since valuations are based on quoted prices that are readily and regularly available in an active market, these valuations do not entail a significant degree of judgment.

•Level 2 – Valuations based on quoted prices in markets that are not active or for which significant inputs are observable, either directly or indirectly.

•Level 3 – Valuations based on inputs that are unobservable and significant to the overall fair value measurement.

The availability of valuation techniques and observable inputs can vary by investment. To the extent that valuations are based on sources that are less observable or unobservable in the market, the determination of fair value requires more judgment. Fair value estimates do not necessarily represent the amounts that may be ultimately realized by the Trust.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fair Value Measurement Using |

|

(Amounts in thousands) |

|

Amount at

Fair Value |

|

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

September 30, 2024 |

|

|

|

|

|

|

|

|

|

|

|

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

Investment in Ether |

|

$ |

1,015,027 |

|

|

$ |

1,015,027 |

|

|

$ |

- |

|

|

$ |

- |

|

Recently Issued Accounting Pronouncements

In December 2023, the FASB issued Accounting Standards Update (“ASU”) 2023-08, Intangibles—Goodwill and Other—Crypto Assets (Subtopic 350-60): Accounting for and Disclosure of Crypto Assets (“ASU 2023-08”). ASU 2023-08 is intended to improve the accounting for certain crypto assets by requiring an entity to measure those crypto assets at fair value each reporting period with changes in fair value recognized in net income. The amendments also improve the information provided to investors about an entity’s crypto asset holdings by requiring disclosure about significant holdings, contractual sale restrictions, and changes during the reporting period. ASU 2023-08 is effective for annual and interim reporting periods beginning after December 15, 2024. Early adoption is permitted for both interim and annual financial statements that have not yet been issued. The Sponsor of the Trust is evaluating this new guidance as of September 30, 2024. If the Sponsor elects to adopt in a subsequent interim period prior to the effective date, such adoption would be reflected retroactive to the beginning of the fiscal year. The Sponsor does not anticipate any material impact on its financial statements and disclosures as the Trust historically used fair value as its method of accounting for Ether in accordance with its classification as an investment company for accounting purposes.

3. Fair Value of Ether

Ether is held by the Custodian on behalf of the Trust and is carried at fair value. As of September 30, 2024, the Trust held 391,232.97302030 Ether. The Trust determined the fair value per Ether to be $2,594.43 on September 30, 2024, using the price provided at 4:00 p.m., New York time, by the Digital Asset Trading Platform Market considered to be the Trust’s principal market (Coinbase).

The following represents the changes in quantity of Ether and the respective fair value:

|

|

|

|

|

|

|

|

|

(Amounts in thousands, except Ether amounts) |

|

Quantity |

|

|

Fair Value |

|

Balance at July 23, 2024 (the commencement of the Trust’s operations) |

|

|

- |

|

|

$ |

- |

|

Ether contributed |

|

|

105,000.71697910 |

|

|

|

310,876 |

|

Ether contributed from Initial Distribution(1) |

|

|

292,262.98913350 |

|

|

|

1,010,935 |

|

Ether redeemed |

|

|

(6,030.73309230 |

) |

|

|

(17,035 |

) |

Ether distributed for Sponsor’s Fee, related party |

|

|

- |

|

|

|

- |

|

Net change in unrealized depreciation on investment in Ether |

|

|

- |

|

|

|

(286,213 |

) |

Net realized gain on investment in Ether sold to pay expenses |

|

|

- |

|

|

|

- |

|

Net realized loss on investment in Ether sold for redemption of Shares |

|

|

- |

|

|

|

(3,536 |

) |

Balance at September 30, 2024 |

|

|

391,232.97302030 |

|

|

$ |

1,015,027 |

|

(1)Represents the impact of the Initial Distribution of 292,262.98913350 Ether, with a value of approximately $1,010.9 million from Grayscale Ethereum Trust (ETH), completed on July 23, 2024, as discussed in Note 4.

4. The Initial Distribution from the Grayscale Ethereum Trust (ETH)

On July 8, 2024, the Sponsor of the Trust issued a press release announcing that its board of directors declared a pro rata distribution on the Shares of the Trust, pursuant to which each holder of Grayscale Ethereum Trust (ETH) (“ETHE”) shares as of 4:00 PM ET on July 18, 2024 (the “Record Date,” and such holders, the “ETHE Record Holders”) was entitled to receive Shares of the Trust, in connection with its previously announced initial creation and distribution of Shares of the Trust (such transactions collectively, the “Initial Distribution”), as described in a definitive information statement on Schedule 14C filed with the Securities and Exchange Commission on July 18, 2024 by ETHE.

In the Initial Distribution, ETHE contributed approximately 10% of the Ether that it held as of 4:00 PM ET on the Record Date to the Trust, and each ETHE Record Holder was entitled to receive Shares pro rata based on a 1:1 ratio, such that for each one (1) ETHE share held by an ETHE Record Holder, such ETHE Record Holder was entitled to receive one (1) Share on the Distribution Date.

In connection therewith, on July 23, 2024, ETHE completed its previously announced pro rata distribution of 310,158,500 Shares of the Trust to shareholders of ETHE as of 4:00 PM ET on the Record Date and contributed to the Trust an amount of Ether equal to approximately 10% of the total Ether held by ETHE as of the Record Date, equal to 292,262.98913350 Ether, with a value of $1,010,934,757, as consideration and in exchange for the issuance of 310,158,500 Shares of the Trust at $3.26 per Share.

It is expected that neither the ETHE Trust nor any beneficial owner of the ETHE shares will recognize any gain or loss for U.S. federal income tax purposes as a result of the Initial Distribution.

5. Creations and Redemptions of Shares

At September 30, 2024, there were an unlimited number of Shares authorized by the Trust. The Trust creates and redeems Shares from time to time, but only in one or more Baskets. The creation and redemption of Baskets on behalf of investors are made by the Authorized Participant in exchange for the delivery of Ether to the Trust or the distribution of Ether by the Trust. The amount of Ether required for each Creation Basket or Redemption Basket is determined by dividing (x) the amount of Ether owned by the Trust at 4:00 p.m., New York time, on such trade date of a creation or redemption order, after deducting the amount of Ether representing the U.S. dollar value of accrued but unpaid fees and expenses of the Trust, by (y) the number of Shares outstanding at such time and multiplying the quotient obtained by 10,000. Each Share represented approximately 0.0009 of one Ether at September 30, 2024.

The cost basis of investments in Ether recorded by the Trust is the fair value of Ether, as determined by the Trust, at 4:00 p.m., New York time, on the date of transfer to the Trust by the Authorized Participant, or Liquidity Provider, based on the Creation Baskets. The cost basis recorded by the Trust may differ from proceeds collected by the Authorized Participant from the sale of each Share to investors. The Authorized Participant or Liquidity Provider may realize significant profits buying, selling, creating, and redeeming Shares as a result of changes in the value of Shares or Ether.

On May 21, 2024, NYSE Arca filed an application with the SEC pursuant to Rule 19b-4 under the Exchange Act to list the Shares of the Trust on NYSE Arca. On April 23, 2024, the Sponsor filed with the SEC a registration statement on Form S-1, as amended through July 18, 2024, to register the Shares of the Trust under the Securities Act of 1933. On July 17, 2024, the SEC approved NYSE Arca’s 19b-4 application to list the Shares of the Trust on NYSE Arca as an exchange-traded product and on July 22, 2024, the Sponsor authorized the commencement of a redemption program once the registration statement on Form S-1, as amended, was declared effective.

|

|

|

|

|

|

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024 |

|

Activity in Number of Shares Issued and Redeemed: |

|

|

|

Shares issued |

|

|

111,430,000 |

|

Shares issued from Initial Distribution(1) |

|

|

310,158,500 |

|

Shares redeemed |

|

|

(6,400,000 |

) |

Net Change in Number of Shares Issued and Redeemed |

|

|

415,188,500 |

|

|

|

|

|

|

(Amounts in thousands) |

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024 |

|

Activity in Value of Shares Issued and Redeemed: |

|

|

|

Shares issued |

|

$ |

310,876 |

|

Shares issued from Initial Distribution(1) |

|

|

1,010,935 |

|

Shares redeemed |

|

|

(17,035 |

) |

Net Change in Value of Shares Issued and Redeemed |

|

$ |

1,304,776 |

|

(1)Represents the impact of the Initial Distribution of 292,262.98913350 Ether, with a value of approximately $1,010.9 million from Grayscale Ethereum Trust (ETH), completed on July 23, 2024, as discussed in Note 4.

Ether receivable represents the value of Ether covered by contractually binding orders for the creation of Shares where the Ether has not yet been transferred to the Trust’s account. Generally, ownership of the Ether is transferred within no more than two business days of the trade date.

|

|

|

|

|

|

|

|

|

(Amounts in thousands) |

|

As of September 30, 2024 |

|

Ether receivable |

|

$ |

- |

|

Ether payable represents the value of Ether covered by contractually binding orders for the redemption of Shares where the Ether has not yet been transferred out of the Trust’s account. Generally, ownership of the Ether is transferred within no more than two business days of the trade date.

|

|

|

|

|

|

|

|

|

(Amounts in thousands) |

|

As of September 30, 2024 |

|

Ether payable |

|

$ |

- |

|

6. Income Taxes

The Sponsor takes the position that the Trust is properly treated as a grantor trust for U.S. federal income tax purposes. Assuming that the Trust is a grantor trust, the Trust will not be subject to U.S. federal income tax. Rather, if the Trust is a grantor trust, each beneficial owner of Shares will be treated as directly owning its pro rata Share of the Trust’s assets and a pro rata portion of the Trust’s income, gain, losses and deductions will “flow through” to each beneficial owner of Shares. If the Trust were not properly classified as a grantor trust, the Trust might be classified as a partnership for U.S. federal income tax purposes. However, due to the uncertain treatment of digital assets, including forks, airdrops and similar occurrences for U.S. federal income tax purposes, there can be no assurance in this regard. If the Trust were classified as a partnership for U.S. federal income tax purposes, the tax consequences of owning Shares generally would not be materially different from the tax consequences described herein, although there might be certain differences, including with respect to timing. In addition, tax information reports provided to beneficial owners of Shares would be made in a different form. If the Trust were not classified as either a grantor trust or a partnership for U.S. federal income tax purposes, it would be classified as a corporation for such purposes. In that event, the Trust would be subject to entity-level U.S. federal income tax (currently at the rate of 21%) on its net taxable income and certain distributions made by the Trust to shareholders would be treated as taxable dividends to the extent of the Trust’s current and accumulated earnings and profits.

In accordance with U.S. GAAP, the Trust has defined the threshold for recognizing the benefits of tax return positions in the financial statements as “more-likely-than-not” to be sustained by the applicable taxing authority and requires measurement of a tax position meeting the “more-likely-than-not” threshold, based on the largest benefit that is more than 50% likely to be realized. Tax positions not deemed to meet the “more-likely-than-not” threshold are recorded as a tax benefit or expense in the current period. As of, and during the period from July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024, the Trust did not have a liability for any unrecognized tax amounts. However, the Sponsor’s conclusions concerning its determination of “more-likely-than-not” tax positions may be subject to review and adjustment at a later date based on factors including, but not limited to, further implementation guidance, and ongoing analyses of and changes to tax laws, regulations and interpretations thereof.

The Sponsor of the Trust has evaluated whether or not there are uncertain tax positions that require financial statement recognition and has determined that no reserves for uncertain tax positions related to federal, state and local income taxes existed as of September 30, 2024.

7. Related Parties

The Trust considered the following entities, their directors, and certain employees to be related parties of the Trust as of September 30, 2024: DCG, Grayscale, and Grayscale Securities, LLC. As of September 30, 2024, 23,058 Shares of the Trust were held by related parties of the Trust.

Genesis Global Trading, Inc. filed a certificate of dissolution during the three months ended September 30, 2024, and has therefore been removed from the list of related parties.

The Sponsor’s indirect parent, an affiliate of the Trust, holds a minority interest in Coinbase, Inc., the parent company of the Custodian, that represents less than 1.0% of Coinbase, Inc.’s ownership.

In accordance with the Trust Agreement governing the Trust, the Trust pays a fee to the Sponsor, calculated as 0.15% of the aggregate value of the Trust’s assets, less its liabilities (which include any accrued but unpaid expenses up to, but excluding, the date of calculation),

as calculated and published by the Sponsor or its delegates in the manner set forth in the Trust Agreement (the “Sponsor’s Fee”). The Sponsor’s Fee accrues daily in U.S. dollars and is payable in Ether, daily in arrears. The amount of Ether payable in respect of each daily U.S. dollar accrual will be determined by reference to the same U.S. dollar value of Ether used to determine such accrual. For purposes of these financial statements, the U.S. dollar value of Ether is determined by reference to the Digital Asset Trading Platform Market that the Trust considers its principal market as of 4:00 p.m., New York time, on each valuation date. The Trust held no Incidental Rights or IR Virtual Currency as of September 30, 2024. No Incidental Rights or IR Virtual Currencies have been distributed in payment of the Sponsor’s Fee during the period from July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024.

As partial consideration for receipt of the Sponsor’s Fee, the Sponsor is obligated under the Trust Agreement to assume and pay all fees and other expenses incurred by the Trust in the ordinary course of its affairs, excluding taxes, but including marketing fees; administrator fees, if any; custodian fees; transfer agent fees; trustee fees; the fees and expenses related to the listing, quotation or trading of the Shares on any secondary market (including customary legal, marketing and audit fees and expenses) in an amount up to $600,000 in any given fiscal year; ordinary course legal fees and expenses; audit fees; regulatory fees, including, if applicable, any fees relating to the registration of the Shares under the Securities Act or the Exchange Act; printing and mailing costs; the costs of maintaining the Trust’s website and applicable license fees (together, the “Sponsor-paid Expenses”), provided that any expense that qualifies as an Additional Trust Expense will be deemed to be an Additional Trust Expense and not a Sponsor-paid Expense.

The Trust may incur certain extraordinary, non-recurring expenses that are not Sponsor-paid Expenses, including, but not limited to, taxes and governmental charges, expenses and costs of any extraordinary services performed by the Sponsor (or any other service provider) on behalf of the Trust to protect the Trust or the interests of shareholders, any indemnification of the Custodian or other agents, service providers or counterparties of the Trust, the fees and expenses related to the listing, quotation or trading of the Shares on any secondary market (including legal, marketing and audit fees and expenses) to the extent exceeding $600,000 in any given fiscal year and extraordinary legal fees and expenses, including any legal fees and expenses incurred in connection with litigation, regulatory enforcement or investigation matters (collectively “Additional Trust Expenses”). In such circumstances, the Sponsor or its delegate (i) will instruct the Custodian to withdraw from the Vault Balance Ether in such quantity as may be necessary to permit payment of such Additional Trust Expenses and (ii) may either (x) cause the Trust (or its delegate) to convert such Ether into U.S. dollars or other fiat currencies at the Actual Exchange Rate or (y) when the Sponsor incurs such expenses on behalf of the Trust, cause the Trust (or its delegate) to deliver such Ether in kind to the Sponsor, in each case in such quantity as may be necessary to permit payment of such Additional Trust Expenses.

The Sponsor, from time to time, may temporarily waive all or a portion of the Sponsor’s Fee of the Trust in its discretion for stated periods of time. Effective July 23, 2024, the Sponsor has determined to waive a portion of the Sponsor’s Fee for the first six months, so that the fee will be 0% of the NAV of the Trust for the first $2.0 billion of the Trust’s assets. If the Trust’s assets exceed $2.0 billion prior to the end of the six-month period, the Sponsor’s Fee charged on assets over $2.0 billion will be 0.15%. All investors will incur the same Sponsor’s Fee, which is the weighted average of those fee rates. After the six-month waiver period is over, the Sponsor’s Fee will be 0.15%. As of the date of this Quarterly Report, the Trust’s assets did not exceed $2.0 billion and no Sponsor’s Fee has been incurred.

On May 31, 2024, the Sponsor purchased 10,000 Shares for $100,000 ($10.00 per share). The Sponsor did not receive from the Trust, or any of its affiliates, any fee or other compensation in connection with the initial seed sale. Subsequently, on July 16, 2024, the Sponsor caused the Trust to distribute $100,000 to the Sponsor in redemption of the 10,000 Shares held by the Sponsor.

As previously described in Note 4, on July 23, 2024, ETHE completed its previously announced pro rata distribution of 310,158,500 Shares of the Trust to shareholders of ETHE as of 4:00 PM ET on the Record Date and contributed to the Trust an amount of Ether equal to approximately 10% of the total Ether held by ETHE as of the Record Date, equal to 292,262.98913350 Ether, as consideration and in exchange for the issuance of Shares of the Trust.

8. Risks and Uncertainties

The Trust is subject to various risks including market risk, liquidity risk, and other risks related to its concentration in a single asset, Ether. Investing in Ether is currently highly speculative and volatile.

The Principal Market NAV of the Trust, calculated by reference to the principal market price in accordance with U.S. GAAP, relates primarily to the value of Ether held by the Trust, and fluctuations in the price of Ether could materially and adversely affect an investment in the Shares of the Trust. The price of Ether has a limited history. During such history, Ether prices have been volatile and subject to influence by many factors, including the levels of liquidity. If the Digital Asset Markets continue to experience significant price fluctuations, the Trust may experience losses. Several factors may affect the price of Ether, including, but not limited to, global Ether supply and demand, theft of Ether from global trading platforms or vaults, competition from other forms of digital currency or payment services, global or regional political, economic or financial conditions, and other unforeseen events and situations.

The Ether held by the Trust are commingled, and the Trust’s shareholders have no specific rights to any specific Ether. In the event of the insolvency of the Trust, its assets may be inadequate to satisfy a claim by its shareholders.

There is currently no clearing house for Ether, nor is there a central or major depository for the custody of Ether. There is a risk that some or all of the Trust’s Ether could be lost or stolen. There can be no assurance that the Custodian will maintain adequate insurance or that such coverage will cover losses with respect to the Trust’s Ether. Further, transactions in Ether are irrevocable. Stolen or incorrectly transferred Ether may be irretrievable. As a result, any incorrectly executed Ether transactions could adversely affect an investment in the Shares.

The SEC has stated that certain digital assets may be considered “securities” under the federal securities laws. The test for determining whether a particular digital asset is a “security” is complex and difficult to apply, and the outcome is difficult to predict. Public, though non-binding, statements by senior officials at the SEC have indicated that the SEC did not consider Bitcoin or Ether to be securities, and does not currently consider Bitcoin to be a security. In addition, the SEC appears to have implicitly accepted that Ether is not a security (i) by not objecting to Ether futures trading on Commodity Futures Trading Commission-regulated markets under rules designed for futures on non-security commodity underliers and (ii) by approving the listing and trading of exchange-traded products (“ETPs”) that invest in Ether (i.e., approving the redemption of shares of the Trust) under the rules for commodity-based trust shares, without requiring these ETPs to be registered as investment companies. Likewise, in various courts filings and arguments the SEC has distinguished Ether from assets that it claimed were securities, and in judicial opinions, courts have accepted or even assumed that Ether is not a security. Moreover, in a recent settlement with another market participant relating to allegations that it acted as an unregistered broker-dealer for facilitating trading in certain digital assets, the SEC highlighted that the firm would cease trading in all digital assets other than Bitcoin, Bitcoin Cash and Ether—activity that, if the SEC believed Ether was presently a security—would continue to constitute unregistered brokerage activity. The SEC staff has also provided informal assurances via no-action letter to a handful of promoters that their digital assets are not securities. On the other hand, the SEC has brought enforcement actions against the issuers and promoters of several other digital assets on the basis that the digital assets in question are securities and has not formally or explicitly confirmed that it does not deem Ether to be a security.

If Ether is determined to be a “security” under federal or state securities laws by the SEC or any other agency, or in a proceeding in a court of law or otherwise, it may have material adverse consequences for Ether. For example, it may become more difficult for Ether to be traded, cleared and custodied as compared to other digital assets that are not considered to be securities, which could, in turn, negatively affect the liquidity and general acceptance of Ether and cause users to migrate to other digital assets. As such, any determination that Ether is a security under federal or state securities laws may adversely affect the value of Ether and, as a result, an investment in the Shares.

In addition, if Ether is in fact a security, the Trust could be considered an unregistered “investment company” under the Investment Company Act of 1940, which could necessitate the Trust’s liquidation. In this case, the Trust and the Sponsor may be deemed to have participated in an illegal offering of securities and there is no guarantee that the Sponsor will be able to register the Trust under the Investment Company Act of 1940 at such time or take such other actions as may be necessary to ensure the Trust’s activities comply with applicable law, which could force the Sponsor to liquidate the Trust.

To the extent a private key required to access an address on the Ethereum Network holding Ether is lost, destroyed or otherwise compromised and no backup of the private keys are accessible, the Trust may be unable to access the Ether controlled by the private key and the private key will not be capable of being restored by the Ethereum Network. The processes by which Ether transactions are settled are dependent on the Ethereum peer-to-peer network, and as such, the Trust is subject to operational risk. A risk also exists with respect to previously unknown technical vulnerabilities, which may adversely affect the value of Ether.

The Trust relies on third-party service providers to perform certain functions essential to its operations. Any disruptions to the Trust’s service providers’ business operations resulting from business failures, financial instability, security failures, government mandated regulation or operational problems could have an adverse impact on the Trust’s ability to access critical services and be disruptive to the operations of the Trust.

The Sponsor and the Trust may be subject to various litigation, regulatory investigations, and other legal proceedings that arise in the ordinary course of its business.

9. Financial Highlights Per Share Performance

|

|

|

|

|

|

|

July 23, 2024 (the commencement of the Trust’s operations) to September 30, 2024 |

|

Per Share Data: |

|

|

|

Principal market net asset value, initial creation |

|

$ |

3.26 |

|

Net increase in net assets from investment operations: |

|

|

|

Net investment loss |

|

|

- |

|

Net realized and unrealized loss |

|

|

(0.82 |

) |

Net decrease in net assets resulting from operations |

|

|

(0.82 |

) |

Principal market net asset value, end of period |

|

$ |

2.44 |

|

Total return |

|

|

-25.15 |

% |

Ratios to average net assets: |

|

|

|

Net investment loss |

|

|

0.00 |

% |

Gross expenses |

|

|

-0.15 |

% |

Net expenses |

|

|

0.00 |

% |

Ratios of net investment loss and expenses to average net assets have been annualized.

An individual shareholder’s return, ratios, and per Share performance may vary from those presented above based on the timing of Share transactions. The amount shown for a Share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the number of Shares issued in Creations occurring at an operational value derived from an operating metric as defined in the Trust Agreement.

Total return is calculated assuming an initial investment made at the Principal Market NAV at the beginning of the period and assuming redemption on the last day of the period and has not been annualized.

10. Indemnifications

In the normal course of business, the Trust enters into certain contracts that provide a variety of indemnities, including contracts with the Sponsor and affiliates of the Sponsor, DCG and its officers, directors, employees, subsidiaries and affiliates, and the Custodian as well as others relating to services provided to the Trust. The Trust’s maximum exposure under these and its other indemnities is unknown. However, no liabilities have arisen under these indemnities in the past and, while there can be no assurances in this regard, there is no expectation that any will occur in the future. Therefore, the Sponsor does not consider it necessary to record a liability in this regard.

11. Subsequent Events

As of the close of business on October 28, 2024, the fair value of Ether determined in accordance with the Trust’s accounting policy was $2,505.39 per Ether.

On October 24, 2024, the Sponsor of the Trust announced its intention to change the name of the Trust to Grayscale Ethereum Mini Trust ETF, effective November 4, 2024. In connection with the name change the Sponsor plans to amend the Amended and Restated Declaration of Trust and Trust Agreement, as amended, to reflect the name change, also effective November 4, 2024. Trading under the new name is expected to begin on November 4, 2024. Following effectiveness of the name change, Shares of the Trust will continue to trade on NYSE Arca under the trading symbol “ETH.”

There are no known events that have occurred that require disclosure other than that which has already been disclosed in these notes to the financial statements.

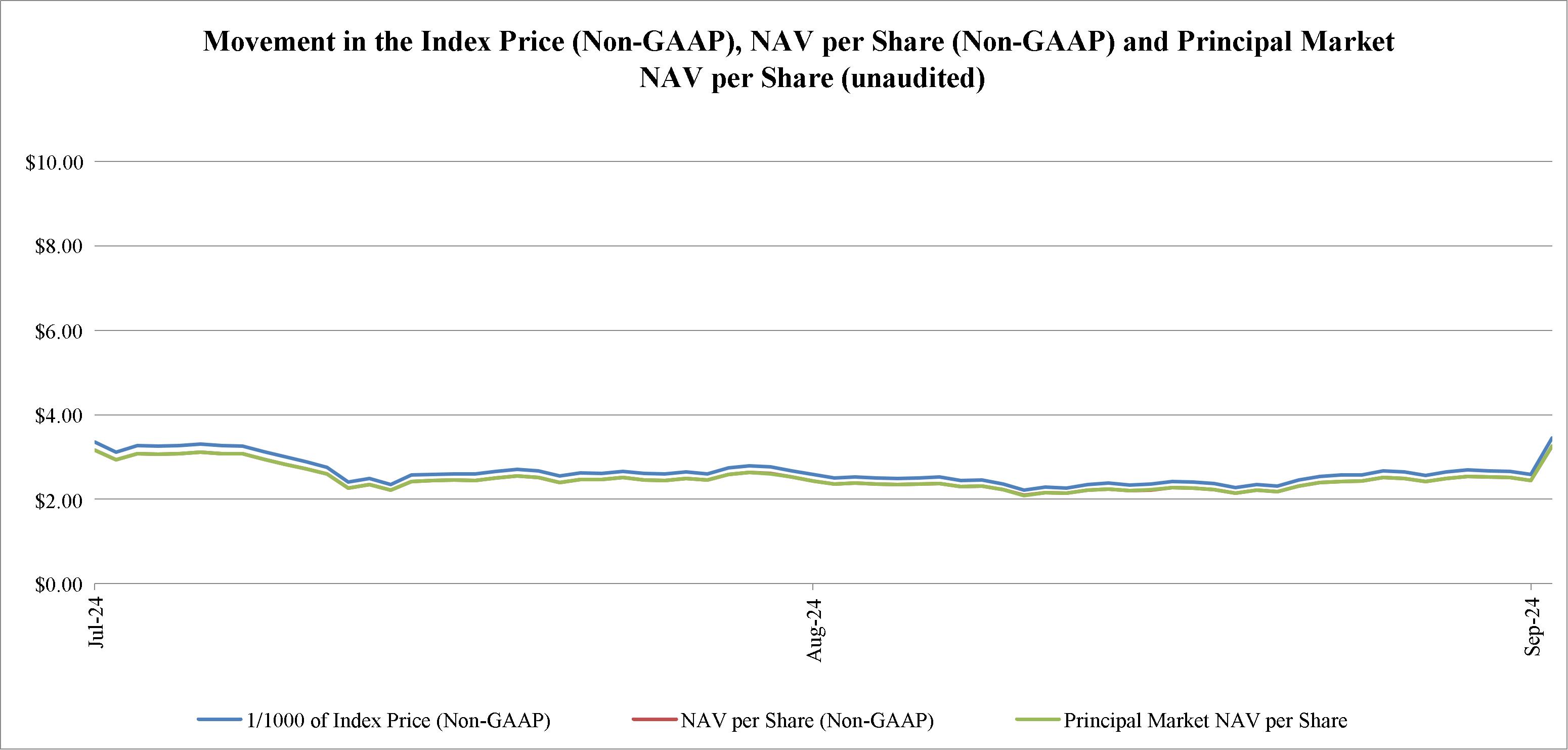

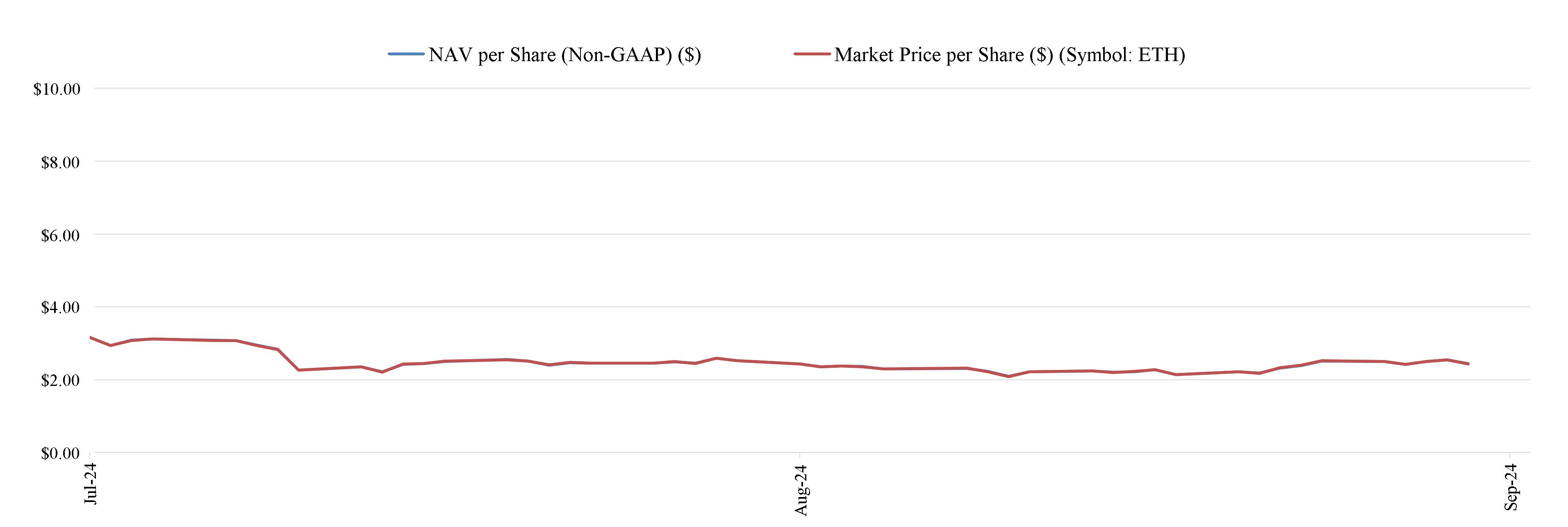

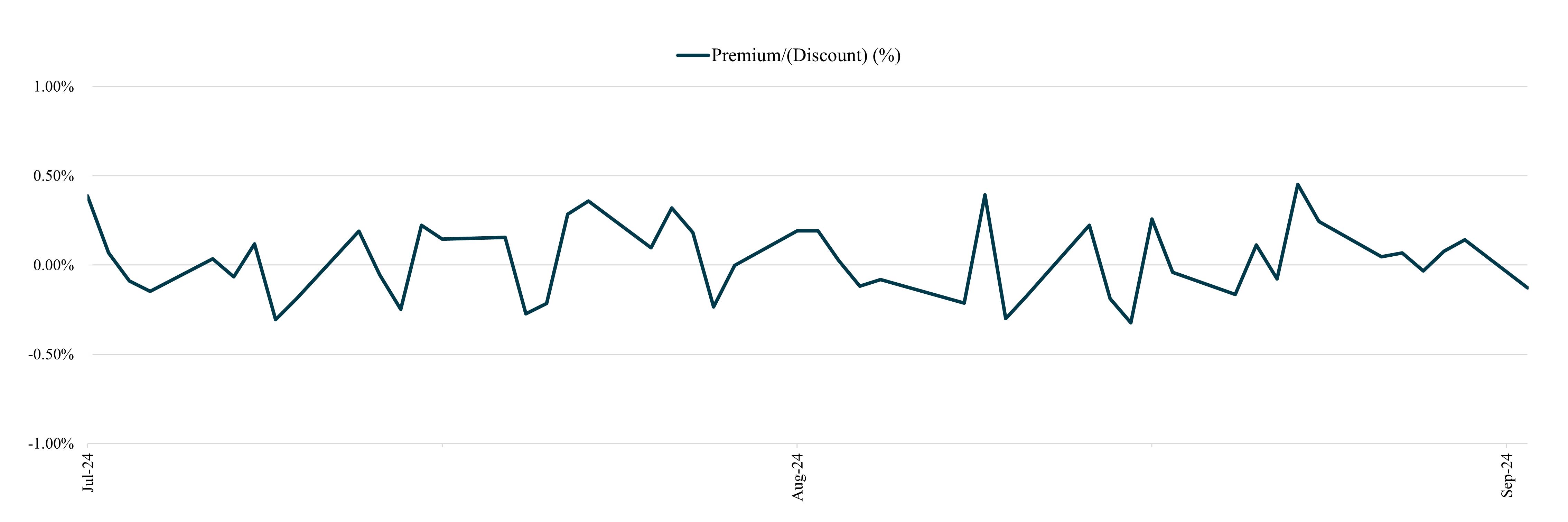

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read together with, and is qualified in its entirety by reference to, our unaudited financial statements and related notes included elsewhere in this Quarterly Report, which have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). The following discussion may contain forward-looking statements based on assumptions we believe to be reasonable. Our actual results could differ materially from those discussed in these forward-looking statements. Factors that could cause or contribute to these differences include, but are not limited to, those set forth under “Part II, Item 1A. Risk Factors” in this Quarterly Report or in “Risk Factors” and “Forward-Looking Statements” or other sections of our Registration Statement.

Trust Overview

The Trust is a passive entity that is managed and administered by the Sponsor and does not have any officers, directors or employees. The Trust holds Ether and, from time to time on a periodic basis, issues Creation Baskets in exchange for deposits of Ether. On July 22, 2024, in connection with the approval of application under Rule 19b-4 of the Securities Exchange Act of 1934 on July 18, 2024 and the effectiveness of the registration statement on Form S-1, as amended (File No. 333-278878), the Sponsor authorized the commencement of a redemption program. Shares of the Trust began trading on NYSE Arca on July 23, 2024, following the effectiveness of the Registration Statement. The Trust issues Shares only in one or more blocks of 10,000 Shares (a block of 10,000 Shares is called a “Basket”) to certain Authorized Participants from time to time. Baskets are offered in exchange for Ether. Through its redemption program, the Trust redeems Shares from Authorized Participants on an ongoing basis. As a passive investment vehicle, the Trust’s investment objective is for the value of the Shares (based on Ether per Share) to reflect the value of Ether held by the Trust, determined by reference to the Index Price, less the Trust’s expenses and other liabilities. While an investment in the Shares is not a direct investment in Ether, the Shares are designed to provide investors with a cost-effective and convenient way to gain investment exposure to Ether. The Trust will not utilize leverage, derivatives or any similar arrangements in seeking to meet its investment objective.

The Trust is not managed like a business corporation or an active investment vehicle.

The Initial Distribution

On July 23, 2024, the Grayscale Ethereum Trust (ETH) (“ETHE”) completed its previously announced pro rata distribution of 310,158,500 Shares of the Trust to shareholders of ETHE as of July 18, 2024 (the “Record Date”), as described in ETHE’s definitive information statement on Schedule 14C, filed with the SEC on July 18, 2024 (referred to as the “Initial Distribution”). In connection therewith, on July 23, 2024, ETHE contributed to the Trust an amount of Ether equal to 10% of the total Ether held by ETHE as of the Record Date, equal to 292,262.98913350 Ether, as consideration and in exchange for the issuance of Shares of the Trust.

Subject to the limitations and qualifications set forth in ETHE’s definitive information statement on Schedule 14C, filed with the SEC on July 18, 2024 (including with respect to the qualification of both ETHE and the Trust as grantor trusts for U.S. federal income tax purposes and the proper allocation of existing tax basis between ETHE shares and Shares of the Trust), it is expected that neither ETHE nor any beneficial owner of ETHE shares will recognize any gain or loss for U.S. federal income tax purposes as a result of the Initial Distribution. Accordingly, it is expected that neither ETHE’s contribution of Ether to the Trust nor ETHE’s distribution of Shares in the Trust to shareholders as of 4:00 PM ET on the Record Date will be reported to any beneficial owner of ETHE shares (or to any intermediary holding ETHE shares) as giving rise to income, gain, loss, deduction, credit or proceeds. Any beneficial owner of ETHE shares who received Shares of the Trust in the Initial Distribution, and any intermediary holding ETHE shares or Shares of the Trust, should consult their own tax advisor regarding the U.S. federal income tax consequences of the Initial Distribution, including the proper allocation of existing tax basis between ETHE shares and Shares of the Trust. Please refer to ETHE’s definitive information statement on Schedule 14C, filed with the SEC on July 18, 2024, for more information, including other U.S. federal income tax considerations relating to the Initial Distribution and ownership of Shares of the Trust.

Critical Accounting Policies and Estimates

Investment Transactions and Revenue Recognition

The Trust considers investment transactions to be the receipt of Ether for Share creations and the delivery of Ether for Share redemptions or for payment of expenses in Ether. The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as net change in unrealized appreciation or depreciation on investments. Realized gains and losses are calculated using the specific identification method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Sponsor’s Fee in Ether.

Principal Market and Fair Value Determination

To determine which market is the Trust’s principal market (or in the absence of a principal market, the most advantageous market) for purposes of calculating the Trust’s net asset value in accordance with U.S. GAAP (“Principal Market NAV”), the Trust follows Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820-10, Fair Value Measurement, which outlines the application of fair value accounting. ASC 820-10 determines fair value to be the price that would be received for Ether in a current sale, which assumes an orderly transaction between market participants on the measurement date. ASC 820-10 requires the Trust to assume that Ether is sold in its principal market to market participants or, in the absence of a principal market, the most advantageous market. Market participants are defined as buyers and sellers in the principal or most advantageous market that are independent, knowledgeable, and willing and able to transact.

The Trust only receives Ether in connection with a creation order from the Authorized Participant (or a Liquidity Provider) and does not itself transact on any Digital Asset Markets. Therefore, the Trust looks to market-based volume and level of activity for Digital Asset Markets. The Authorized Participant(s), or a Liquidity Provider, may transact in a Brokered Market, a Dealer Market, Principal-to-Principal Markets and Exchange Markets (referred to as “Trading Platform Markets” in this Quarterly Report), each as defined in the FASB ASC Master Glossary (collectively, “Digital Asset Markets”). In determining which of the eligible Digital Asset Markets is the Trust’s principal market, the Trust reviews these criteria in the following order:

•First, the Trust reviews a list of Digital Asset Markets that maintain practices and policies designed to comply with anti-money laundering (“AML”) and know-your-customer (“KYC”) regulations, and non-Digital Asset Trading Platform Markets that the Trust reasonably believes are operating in compliance with applicable law, including federal and state licensing requirements, based upon information and assurances provided to it by each market.

•Second, the Trust sorts these Digital Asset Markets from high to low by market-based volume and level of activity of Ether traded on each Digital Asset Market in the trailing twelve months.

•Third, the Trust then reviews pricing fluctuations and the degree of variances in price on Digital Asset Markets to identify any material notable variances that may impact the volume or price information of a particular Digital Asset Market.

•Fourth, the Trust then selects a Digital Asset Market as its principal market based on the highest market-based volume, level of activity and price stability in comparison to the other Digital Asset Markets on the list. Based on information reasonably available to the Trust, Trading Platform Markets have the greatest volume and level of activity for the asset. The Trust therefore looks to accessible Trading Platform Markets as opposed to the Brokered Market, Dealer Market and Principal-to-Principal Markets to determine its principal market. As a result of the aforementioned analysis, a Trading Platform Market has been selected as the Trust’s principal market.

The Trust determines its principal market(or in the absence of a principal market the most advantageous market) annually and conducts a quarterly analysis to determine (i) if there have been recent changes to each Digital Asset Market’s trading volume and level of activity in the trailing twelve months, (ii) if any Digital Asset Markets have developed that the Trust has access to, or (iii) if recent changes to each Digital Asset Market’s price stability have occurred that would materially impact the selection of the principal market and necessitate a change in the Trust’s determination of its principal market.

The cost basis of Ether received in connection with a creation order is recorded by the Trust at the fair value of Ether at 4:00 p.m., New York time, on the creation date for financial reporting purposes. The cost basis recorded by the Trust may differ from proceeds collected by the Authorized Participant from the sale of the corresponding Shares to investors.

Investment Company Considerations

The Trust is an investment company for U.S. GAAP purposes and follows accounting and reporting guidance in accordance with the FASB ASC Topic 946, Financial Services—Investment Companies. The Trust uses fair value as its method of accounting for Ether in accordance with its classification as an investment company for accounting purposes. The Trust is not a registered investment

company under the Investment Company Act of 1940. U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates and these differences could be material.

Review of Financial Results (unaudited)