UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a)

of

the Securities Exchange Act of 1934

Filed by the Registrant ¨ Filed

by a Party other than the Registrant x

Check the

appropriate box:

| ¨ |

Preliminary Proxy Statement |

| ¨ |

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ |

Definitive Proxy Statement |

| x |

Definitive Additional Materials |

| ¨ |

Soliciting material Pursuant to §240.14a-12 |

Air Products and Chemicals,

Inc.

(Name of Registrant as

Specified In Its Charter)

MANTLE RIDGE LP

EAGLE FUND A1 LTD

EAGLE ADVISOR LLC

PAUL HILAL

ANDREW EVANS

TRACY MCKIBBEN

DENNIS REILLEY

(Name of Person(s) Filing

Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check

the appropriate box):

| x |

No fee required |

| ¨ |

Fee paid previously with preliminary materials |

| ¨ |

Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 |

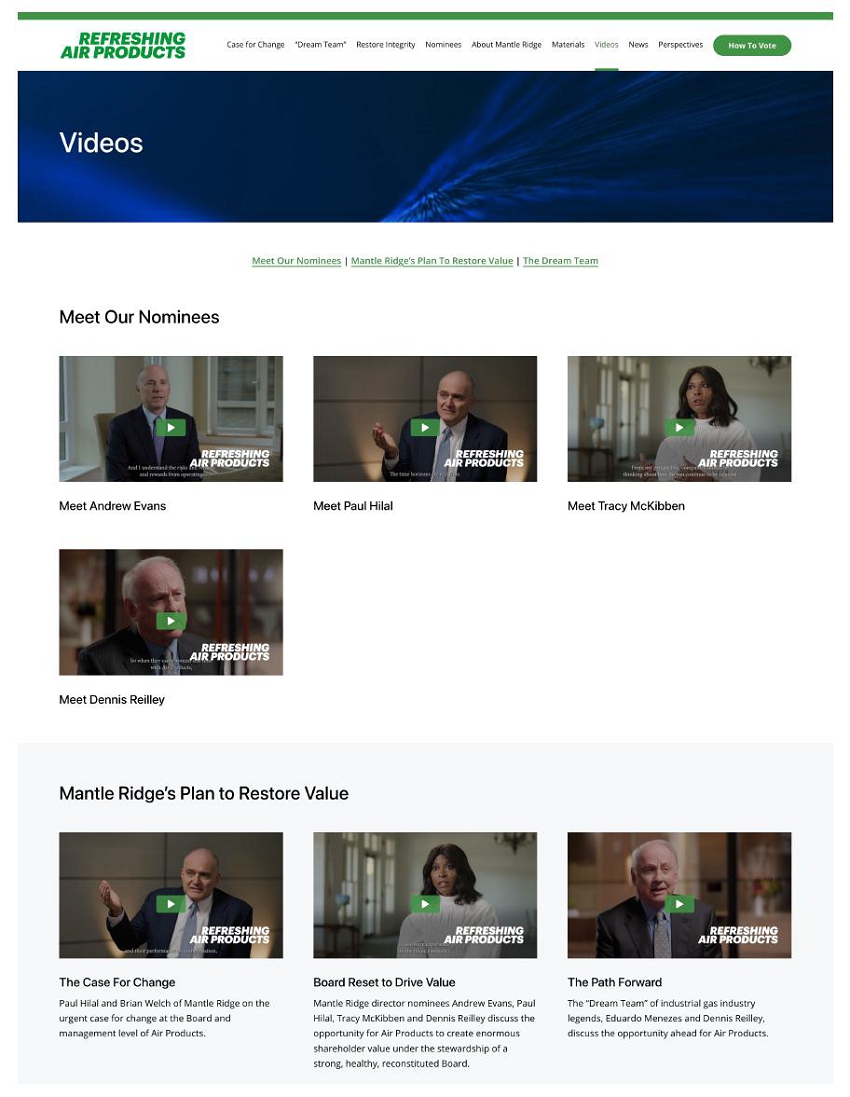

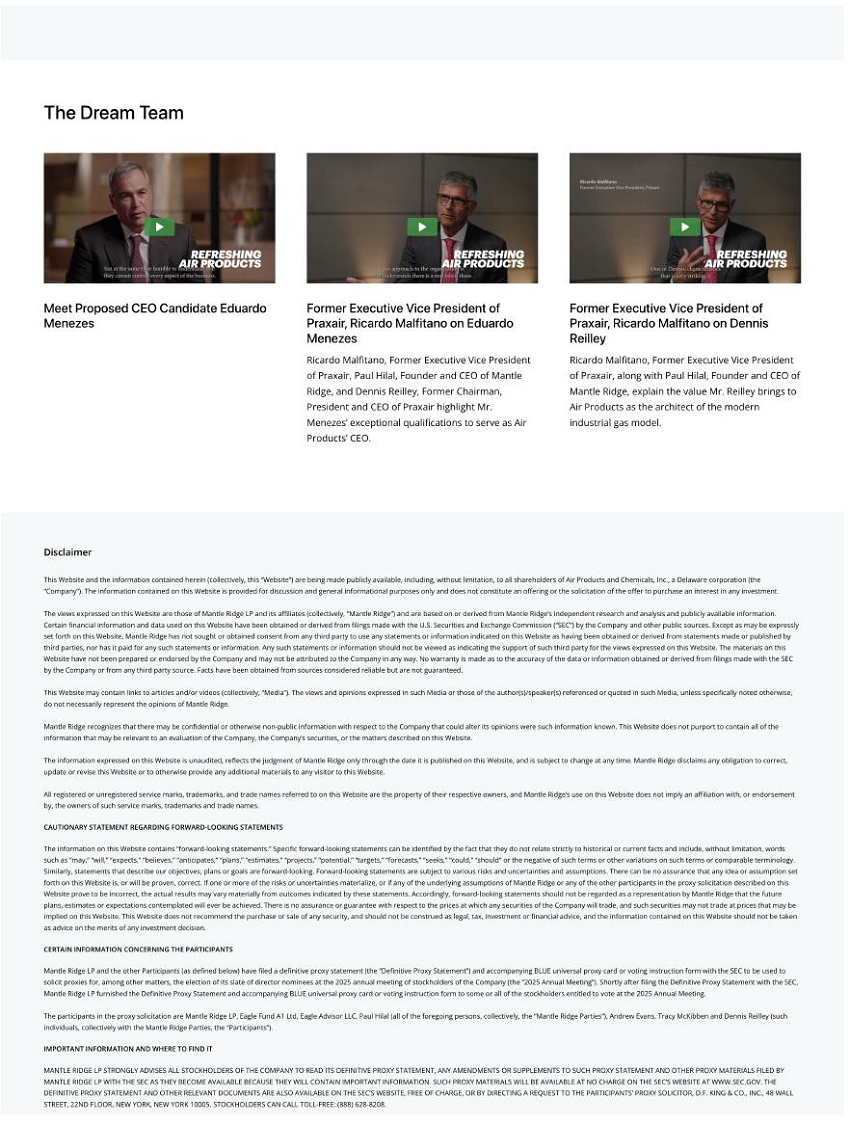

On January 7, 2025, Mantle Ridge LP, which, together

with its affiliates (collectively, “Mantle Ridge”), beneficially owns approximately $1.3 billion of the outstanding common

shares of Air Products and Chemicals, Inc. (NYSE: APD) (“Air Products” or the “Company”), uploaded to its website,

www.RefreshingAirProducts.com (the “Website”), a series of video interviews with its four director candidates seeking election

to Air Products’ Board of Directors at the Company’s 2025 Annual Meeting of Shareholders, as well as with its proposed CEO

candidate Eduardo Menezes. A screenshot of the new “Videos” section of the Website is attached hereto as Exhibit 1.

Transcripts of each video are attached hereto as Exhibits 2 through 11.

Also on January 7, 2025, Mantle Ridge issued the

following press release:

Mantle Ridge Releases Video Series Introducing

Shareholder Nominees and Outlining Solutions for Challenges and Underperformance at Air Products and Chemicals, Inc.

Introduces Four Independent Shareholder Nominees

– Andrew Evans, Paul Hilal, Tracy McKibben, and Dennis Reilley – and Proposed CEO Candidate Eduardo Menezes

Includes Perspectives from Former Praxair EVP

Ricardo Malfitano on Messrs. Menezes and Reilley

Explains Nature and Causes of Air Products’

Underperformance Under Current Leadership,

and the Solution

Urges Shareholders to Vote the BLUE

Proxy Card “FOR” Mantle Ridge’s Four Highly Qualified Director Nominees and “WITHHOLD” on

the Company Nominees Charles Cogut, Lisa A. Davis, Seifollah “Seifi” Ghasemi and Edward L. Monser

View the Videos and Related Materials at www.RefreshingAirProducts.com

New York – January 7, 2025 – Mantle

Ridge LP, which, together with its affiliates (collectively, “Mantle Ridge”), beneficially owns approximately $1.3 billion

of the outstanding common shares of Air Products and Chemicals, Inc. (NYSE: APD) (“Air Products” or the “Company”),

today released a series of video interviews with its four director candidates seeking election to Air Products’ Board of Directors

(the “Board”) at the Company’s 2025 Annual Meeting of Shareholders (the “Annual Meeting”), as well as with

its proposed CEO candidate Eduardo Menezes.

The video content includes the case for change

at Air Products, as well as commentary from Ricardo Malfitano, Former Executive Vice President of Praxair, concerning Mr. Menezes and

Mr. Reilley.

Mantle Ridge encourages all shareholders to review

the videos, which are available here and accessible alongside related materials at www.RefreshingAirProducts.com.

To Enhance Air Products’ Performance and

Create the Long-Term Value that Shareholders Deserve, Mantle Ridge Urges Shareholders to Vote the BLUE Proxy Card “FOR”

Mantle Ridge’s Four Highly Qualified Director Nominees – Andrew Evans, Paul Hilal, Tracy McKibben, and Dennis Reilley –

and “WITHHOLD” on the Company Nominees Charles Cogut, Lisa A. Davis, Seifollah “Seifi” Ghasemi and Edward L. Monser

Additional information regarding Mantle Ridge’s

highly qualified nominees and other materials related to its proxy campaign, may be found at www.RefreshingAirProducts.com.

***

About Mantle Ridge

Founded in 2016, Mantle Ridge LP is an engaged,

long-term owner-steward that works closely and constructively with company boards to create durable long-term value for all stakeholders.

None of Mantle Ridge’s affiliated entities is a hedge fund or other investment vehicle with a structurally short-term incentive.

Mantle Ridge engages with the expectation of maintaining an ownership position over the very long-term. Mantle Ridge has raised separate,

single-investment, five-year special purpose vehicles to support its previous engagements with companies including CSX Corporation, Aramark,

and Dollar Tree. For more information, visit https://www.mantleridge.com/.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING

STATEMENTS

The information herein contains “forward-looking

statements.” Specific forward-looking statements can be identified by the fact that they do not relate strictly to historical or

current facts and include, without limitation, words such as “may,” “will,” “expects,” “believes,”

“anticipates,” “plans,” “estimates,” “projects,” “potential,” “targets,”

“forecasts,” “seeks,” “could,” “should” or the negative of such terms or other variations

on such terms or comparable terminology. Similarly, statements that describe our objectives, plans or goals are forward-looking. Forward-looking

statements are subject to various risks and uncertainties and assumptions. There can be no assurance that any idea or assumption herein

is, or will be proven, correct. If one or more of the risks or uncertainties materialize, or if any of the underlying assumptions of Mantle

Ridge LP and its affiliates (collectively, “Mantle Ridge”) or any of the other participants in the proxy solicitation described

herein prove to be incorrect, the actual results may vary materially from outcomes indicated by these statements. Accordingly, forward-looking

statements should not be regarded as a representation by Mantle Ridge that the future plans, estimates or expectations contemplated will

ever be achieved.

Certain statements and information included herein

may have been sourced from third parties. Mantle Ridge does not make any representations regarding the accuracy, completeness or timeliness

of such third party statements or information. Except as may be expressly set forth herein, permission to cite such statements or information

has neither been sought nor obtained from such third parties, nor has Mantle Ridge paid for any such statements or information. Any such

statements or information should not be viewed as an indication of support from such third parties for the views expressed herein.

Mantle Ridge disclaims any obligation to update

the information herein or to disclose the results of any revisions that may be made to any projected results or forward-looking statements

herein to reflect events or circumstances after the date of such information, projected results or statements or to reflect the occurrence

of anticipated or unanticipated events.

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

Mantle Ridge LP and the other Participants (as

defined below) have filed a definitive proxy statement (the “Definitive Proxy Statement”) and accompanying BLUE universal

proxy card or voting instruction form with the SEC to be used to solicit proxies for, among other matters, the election of its slate of

director nominees at the 2025 annual meeting of stockholders of the Company (the “2025 Annual Meeting”). Shortly after filing

the Definitive Proxy Statement with the SEC, Mantle Ridge LP furnished the Definitive Proxy Statement and accompanying BLUE universal

proxy card or voting instruction form to some or all of the stockholders entitled to vote at the 2025 Annual Meeting.

The participants in the proxy solicitation are

Mantle Ridge LP, Eagle Fund A1 Ltd, Eagle Advisor LLC, Paul Hilal (all of the foregoing persons, collectively, the “Mantle Ridge

Parties”), Andrew Evans, Tracy McKibben and Dennis Reilley (such individuals, collectively with the Mantle Ridge Parties, the “Participants”).

IMPORTANT INFORMATION AND WHERE TO FIND IT

MANTLE RIDGE LP STRONGLY ADVISES ALL STOCKHOLDERS

OF THE COMPANY TO READ ITS DEFINITIVE PROXY STATEMENT, ANY AMENDMENTS OR SUPPLEMENTS TO SUCH PROXY STATEMENT AND OTHER PROXY MATERIALS

FILED BY MANTLE RIDGE LP WITH THE SEC AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL

BE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT WWW.SEC.GOV. THE DEFINITIVE PROXY STATEMENT AND OTHER RELEVANT DOCUMENTS ARE ALSO

AVAILABLE ON THE SEC’S WEBSITE, FREE OF CHARGE, OR BY DIRECTING A REQUEST TO THE PARTICIPANTS’ PROXY SOLICITOR, D.F. KING

& CO., INC., 48 WALL STREET, 22ND FLOOR, NEW YORK, NEW YORK 10005. STOCKHOLDERS CAN CALL TOLL-FREE: (888) 628-8208.

Information about the Participants and a description

of their direct or indirect interests by security holdings or otherwise can be found in the Definitive Proxy Statement.

Investor Contact

D.F. King & Co., Inc.

Edward McCarthy

Tel: (212) 493-6952

Media Contacts

Jonathan Gasthalter / Nathaniel Garnick

Gasthalter & Co.

Tel: (212) 257-4170

Email: RefreshingAPD@gasthalter.com

Exhibit 1

Exhibit 2

Video #1: “Meet Andrew Evans”

ANDREW EVANS:

00:00:03:05 - 00:00:03:19

Hello.

00:00:03:19 - 00:00:05:17

My name is Drew Evans.

00:00:06:02 - 00:00:09:20

I’m delighted to be considered

for the Board of Air Products.

00:00:09:20 - 00:00:11:22

It's a very interesting business to me.

00:00:11:22 - 00:00:13:17

And very capital intensive,

00:00:13:17 - 00:00:17:01

much like the businesses

I've operated for the last 30 years.

00:00:17:15 - 00:00:20:13

Throughout my career,

I've been a Treasurer, a Chief

00:00:20:13 - 00:00:24:07

Financial Officer, a Chief Operating

Officer and a Chief Executive Officer

00:00:24:16 - 00:00:28:03

in largely capital

intensive public utility businesses.

00:00:28:12 - 00:00:33:02

And I understand the risks and returns

and rewards from operating

00:00:33:02 - 00:00:36:19

in capital intensive businesses

in all types of markets.

00:00:37:01 - 00:00:40:19

I think much like in public utilities,

when you start with a base

00:00:40:19 - 00:00:43:08

where return

is relatively straightforward,

00:00:43:08 - 00:00:47:09

as you start to stretch into businesses

that are more merchant related,

00:00:47:09 - 00:00:51:12

much like hydrogen or much like

independent power production,

00:00:51:18 - 00:00:54:13

there's a much different set

of construction parameters

00:00:54:13 - 00:00:57:17

and risk parameters

associated with these types of projects.

00:00:57:17 - 00:01:01:13

When you move into businesses

like that, a different structure

00:01:01:13 - 00:01:03:14

has to take place

and a different expectation

00:01:03:14 - 00:01:06:18

about how you’ll manage

risks has to be formulated.

00:01:07:08 - 00:01:09:06

You have to really understand

00:01:09:06 - 00:01:13:23

these risk parameters, consolidate them

with your return expectations,

00:01:14:06 - 00:01:16:23

and try to drive towards

something that's more consistent

00:01:16:23 - 00:01:21:03

with what shareholders

acquired this equity in anticipation of.

00:01:21:18 - 00:01:26:03

I have seen shareholder

driven board refreshment from both sides,

00:01:26:03 - 00:01:28:18

and I view that it can be

highly constructive,

00:01:28:18 - 00:01:30:21

particularly in this setting.

00:01:30:21 - 00:01:34:15

One of the reasons I signed up for

this was because I had a chance

00:01:34:15 - 00:01:38:09

to take a look at my fellow nominees,

and I'm very comfortable

00:01:38:09 - 00:01:43:02

that this is a constructive

and productive, group of individuals

00:01:43:02 - 00:01:46:12

who work harmoniously

with an existing board of directors.

00:01:46:16 - 00:01:47:21

I signed up for this because

00:01:47:21 - 00:01:50:17

I think we can find harmony

and success

00:01:50:17 - 00:01:52:22

with a refreshed board

at Air Products.

Exhibit 3

Video #2: “Meet Paul Hilal”

PAUL HILAL:

00:00:07:02 - 00:00:08:12

People ask me why

00:00:08:12 - 00:00:10:17

I enjoy serving on boards.

00:00:11:05 - 00:00:12:05

It's really

00:00:12:05 - 00:00:15:05

the most satisfying thing that I do.

00:00:15:13 - 00:00:19:00

I feel personally that

I have a tremendous amount of experience

00:00:19:11 - 00:00:23:05

dealing with boards that are going through

exactly this kind of moment.

00:00:23:09 - 00:00:26:09

This is what I've been doing

since 2006, 18 years,

00:00:26:23 - 00:00:29:01

is working with boards

through this kind of

00:00:29:01 - 00:00:32:03

shareholder driven

refreshment and reconstitution,

00:00:32:13 - 00:00:35:18

and helping them find harmony

and helping them find a better groove.

00:00:36:09 - 00:00:40:06

But also, the job of being

a Corporate Director today is very hard.

00:00:40:06 - 00:00:42:13

It's much harder than it was 20 years ago.

00:00:42:13 - 00:00:45:08

These companies are far more complex.

00:00:45:08 - 00:00:47:17

Businesses are truly global.

00:00:47:17 - 00:00:50:09

The time horizons are real time.

00:00:50:09 - 00:00:53:15

And the competitors

are much more intense.

00:00:54:06 - 00:00:56:00

It's very hard to be a Corporate Director.

00:00:56:00 - 00:00:59:05

And when people think about

whether to elect

00:00:59:20 - 00:01:02:11

a Mantle Ridge person

to a Board of Directors,

00:01:02:11 - 00:01:05:04

they should understand

it's not just that one person they get.

00:01:05:04 - 00:01:08:16

They get a whole team of people

who are enormously, personally,

00:01:08:16 - 00:01:10:08

economically invested

00:01:10:08 - 00:01:12:09

in perfect alignment with the board.

00:01:12:15 - 00:01:17:03

And you have deep training

in many different facets

00:01:17:16 - 00:01:21:19

of the financial world

who come with that seat.

00:01:22:09 - 00:01:25:22

We experience ourselves

as the eyes and ears of the shareholder

00:01:25:22 - 00:01:29:05

and also the voice of the shareholder

inside the boardroom.

00:01:29:12 - 00:01:31:23

Air Products is at an historic juncture.

00:01:32:05 - 00:01:35:21

We have these two extraordinary executives

00:01:36:06 - 00:01:38:17

that are available to step in

00:01:38:17 - 00:01:40:13

and help the company

00:01:41:00 - 00:01:44:14

work for the shareholders

as opposed to work for any one individual.

00:01:45:04 - 00:01:49:09

And this is about whether the shareholders

want this company

00:01:49:22 - 00:01:53:07

to continue

running as it is with the same board,

00:01:53:07 - 00:01:58:05

the same performance of the board,

the same continuation of the status quo,

00:01:58:16 - 00:02:02:03

or whether the shareholders think that

there's a better way to run this company.

Exhibit 4

Video #3: “Meet Tracy McKibben”

TRACY MCKIBBEN:

00:00:06:12 - 00:00:08:13

I've been investing in the

00:00:08:13 - 00:00:11:05

energy space now for almost two decades.

00:00:11:05 - 00:00:15:15

I see myself as someone who focuses a lot

on new opportunities,

00:00:16:01 - 00:00:19:05

investing in unchartered territory.

00:00:19:13 - 00:00:23:11

However, using very consistent,

and tried and true,

00:00:23:17 - 00:00:26:23

risk mitigated models.

00:00:27:05 - 00:00:30:05

My background is I'm a lawyer by training.

00:00:30:06 - 00:00:34:20

I began my career at a large,

major international law firm.

00:00:35:03 - 00:00:38:05

I've also served in government,

where I did policy

00:00:38:05 - 00:00:41:07

work at the National Security Council

in the White House.

00:00:41:15 - 00:00:44:04

I also have experience

in the finance industry.

00:00:44:04 - 00:00:48:14

I started the environmental banking

strategy at Citigroup.

00:00:48:15 - 00:00:52:13

And so my experience

and what I bring to the company

00:00:52:13 - 00:00:58:07

that I have today is all of that

legal, policy, finance perspective

00:00:58:15 - 00:01:02:07

that I think helps me see opportunities

that others may not be able to see.

00:01:02:17 - 00:01:05:05

Policies, the regulatory framework

00:01:05:05 - 00:01:08:08

or even deregulation can

have an impact on businesses.

00:01:08:08 - 00:01:12:15

That's not necessarily a reason

not to explore new opportunities,

00:01:12:18 - 00:01:17:20

but it's appreciating that you have a

business that has that regulatory risk.

00:01:18:05 - 00:01:19:15

It is a higher risk.

00:01:19:15 - 00:01:22:22

The return may be higher,

but also with that risk

00:01:22:22 - 00:01:27:00

you've got to have the right mitigation strategy.

You've got to make sure that you've got the right

00:01:27:00 - 00:01:33:05

capabilities, capacities and skill set to be

able to understand and appreciate and address that risk

00:01:33:05 - 00:01:36:19

and still deliver what shareholders

expect you to deliver,

00:01:36:19 - 00:01:40:01

which is performance and

execution on the strategy.

00:01:40:01 - 00:01:43:02

And so I bring that perspective

00:01:43:02 - 00:01:46:14

from having worked in the policy world,

from having worked in government.

00:01:46:14 - 00:01:49:21

I've served on public

and private company boards.

00:01:49:21 - 00:01:53:23

I've served in the capacity as a chair

of committees, both audit and finance.

00:01:54:00 - 00:01:55:23

I've served on compensation committees.

00:01:55:23 - 00:01:58:00

I've served on governance committees.

00:01:58:00 - 00:02:01:13

And again, all understanding that

the role of the board is really to help

00:02:01:13 - 00:02:06:15

management achieve the best performance,

and also protecting shareholder interests.

00:02:06:16 - 00:02:08:15

When you think about, in particular

00:02:08:15 - 00:02:10:04

the energy transition,

00:02:10:04 - 00:02:10:19

like

00:02:10:19 - 00:02:14:04

there's lots of volatility,

there will be lots of challenges.

00:02:14:04 - 00:02:18:12

From my perspective, companies should be

thinking about how do you continue to be relevant

00:02:18:12 - 00:02:23:17

in those future markets? Utilizing your

core competencies and capabilities.

00:02:23:17 - 00:02:27:14

You know, given an opportunity

to serve on this board, I'm excited

00:02:27:14 - 00:02:30:12

So what I try to do is work

collaboratively

00:02:30:12 - 00:02:34:05

with all of the directors to achieve

ultimately what we all want to achieve,

00:02:34:12 - 00:02:38:05

which is to help the company

grow, help the company be sustainable

00:02:38:13 - 00:02:42:12

and also meet shareholder

demands and expectations.

Exhibit 5

Video #4: “Meet Dennis Reilley”

DENNIS REILLEY:

00:00:09:19 - 00:00:12:14

My relationship with Paul Hilal

00:00:13:00 - 00:00:16:16

goes back to 2012, 2013.

00:00:17:00 - 00:00:19:22

He came to my home in Oklahoma, actually,

00:00:19:22 - 00:00:22:21

to talk to me

about the Air Products opportunity.

00:00:22:21 - 00:00:25:05

He showed me a,

00:00:25:05 - 00:00:27:02

as Paul

00:00:27:02 - 00:00:30:12

and his people are very good at,

an enormous deck

00:00:31:02 - 00:00:34:18

of tremendous analytics, analyzing

the company.

00:00:35:03 - 00:00:37:22

And I looked at it, and I was in

00:00:37:22 - 00:00:40:19

complete and total agreement, that

00:00:40:19 - 00:00:43:00

these guys had really

00:00:43:00 - 00:00:46:00

sort of nailed the situation.

00:00:46:01 - 00:00:49:05

And there was enormous opportunity

for improvement,

00:00:49:16 - 00:00:52:16

without too much difficulty.

00:00:53:18 - 00:00:56:11

I told Paul

then that it just wasn't right for me.

00:00:57:01 - 00:01:00:01

I hadn't been retired all that long.

00:01:00:08 - 00:01:03:07

I felt a little pull of the heartstring

00:01:03:07 - 00:01:06:00

about going back and competing

00:01:06:00 - 00:01:08:23

against my former company,

00:01:09:06 - 00:01:13:03

where those people moved

heaven and earth for me for 7 or 8 years.

00:01:13:10 - 00:01:19:07

And then, I remember Paul calling me

maybe three or four weeks later, five weeks,

00:01:19:07 - 00:01:23:03

I don't remember exactly,

and said that he and his partner

00:01:23:03 - 00:01:28:04

wanted to come back in and see me,

and see if they could make another pitch.

00:01:28:16 - 00:01:31:10

They did, equally

00:01:31:10 - 00:01:34:10

as compelling pitch

as the first time around.

00:01:34:12 - 00:01:37:03

But again, for me, at that point in time,

00:01:37:03 - 00:01:40:01

it just didn't feel right.

00:01:40:16 - 00:01:43:14

I was always struck by three things,

really

00:01:43:14 - 00:01:48:18

the integrity of Paul and the people

that he surrounded himself with,

00:01:49:06 - 00:01:53:09

the depth of detail,

work that they would do,

00:01:53:23 - 00:01:57:19

and then I think I just more than anything

else, I appreciated the humanity.

00:01:58:06 - 00:02:01:06

Sort of the understanding of people

00:02:01:12 - 00:02:04:14

and the impact

these kind of things have on the people.

00:02:04:23 - 00:02:07:07

And I always had great respect for that.

00:02:07:07 - 00:02:10:03

So when they came around this time

with Air Products,

00:02:10:03 - 00:02:13:03

they took me through

their point of view.

00:02:13:09 - 00:02:16:04

They showed me an enormous amount of data.

00:02:16:04 - 00:02:20:15

And from looking at it from the outside,

it caught my eye.

00:02:21:01 - 00:02:24:02

And I thought there was ample opportunity

to improve

00:02:24:02 - 00:02:27:02

the business,

for the benefit of the shareholder.

00:02:27:06 - 00:02:28:21

And I think it was the combination

00:02:28:21 - 00:02:31:12

of those things

that attracted me to this opportunity.

00:02:31:22 - 00:02:35:01

I think from the outside looking in,

you often think these things

00:02:35:01 - 00:02:36:00

will be more difficult

00:02:36:00 - 00:02:39:07

than they are in terms of the integrating

of the board of directors.

00:02:39:18 - 00:02:42:18

I've found it in

three cases to be just the opposite.

00:02:42:22 - 00:02:45:18

Does it take a little work? Sure it does.

00:02:45:23 - 00:02:49:03

But things come together

a lot quicker than you think they might.

00:02:50:01 - 00:02:52:03

My biggest regret that I have

00:02:52:03 - 00:02:55:21

relative

to where we are today with Air Products,

00:02:56:04 - 00:02:58:13

is that this went to a proxy battle.

00:02:58:13 - 00:03:02:12

For that part, from an employee

point of view at Air Products, I feel

00:03:02:12 - 00:03:06:05

very sorry that we are in the position

where we are today.

00:03:07:02 - 00:03:09:10

I think we've done our best

00:03:09:10 - 00:03:14:03

to try to figure out how to negotiate

a reasonable outcome here,

00:03:14:10 - 00:03:17:10

but sometimes it just isn't possible.

00:03:17:13 - 00:03:21:11

So ultimately, the shareholders

will make the decision as they should.

00:03:22:03 - 00:03:25:14

I think today when I look at

the Air Products

00:03:25:14 - 00:03:29:22

opportunity,

you know, I think of three things:

00:03:30:00 - 00:03:32:19

I think we need to think about leadership.

00:03:32:19 - 00:03:37:04

We need to think about strategy,

and we need to think about execution.

00:03:37:18 - 00:03:40:17

And I think those are the keys

00:03:40:17 - 00:03:44:07

to allowing Air Products

to compete better

00:03:44:21 - 00:03:48:00

in the industrial gas businesses

than it does today.

00:03:48:17 - 00:03:52:02

I do know this,

that it's in the interest of the company

00:03:52:15 - 00:03:55:15

that those projects

be as successful as possible.

00:03:56:02 - 00:03:59:02

So should I get the opportunity

to serve on the board,

00:03:59:11 - 00:04:01:20

should the shareholders want that,

00:04:01:20 - 00:04:05:04

my view would be singular focused.

That is to make

00:04:05:04 - 00:04:09:00

the very best we possibly can

out of those three projects.

00:04:10:07 - 00:04:12:11

I grew up in engineering companies.

00:04:12:11 - 00:04:14:17

I was trained in engineering companies.

00:04:14:17 - 00:04:18:23

I've done a lot of major projects

around the world. So I would hope

00:04:18:23 - 00:04:21:23

I can bring something to the table

that will be positive

00:04:22:06 - 00:04:26:05

relative to all that,

because it is very important that

00:04:27:07 - 00:04:33:10

whoever is responsible makes the very most

they possibly can out of those projects.

Exhibit 6

Video #5: “The Case for Change”

PAUL HILAL:

00:00:02:10 - 00:00:05:13

Generally,

the solution is some combination

00:00:05:13 - 00:00:08:09

of board refreshment

and leadership change.

00:00:13:03 - 00:00:17:01

Mantle Ridge is a group of people

that look for opportunities

00:00:17:01 - 00:00:20:19

to help publicly traded companies

that have lost their way

00:00:20:20 - 00:00:22:09

get back on track.

00:00:22:09 - 00:00:26:07

And we typically do that

by working on a consultative basis

00:00:26:07 - 00:00:31:07

with a board to examine and understand

what's happened, what the situation is,

00:00:31:17 - 00:00:35:02

and to take a fresh look at what

the right path forward might be.

00:00:35:20 - 00:00:39:13

We think of ourselves as establishing

a permanent ownership position

00:00:39:23 - 00:00:41:06

in these companies.

00:00:41:06 - 00:00:44:18

And if honored with the opportunity

to serve the shareholders

00:00:44:18 - 00:00:47:18

on the board of directors,

that's what they can expect of us.

00:00:48:03 - 00:00:53:17

This model of bringing a deeply resourced,

closely aligned,

00:00:54:03 - 00:00:59:02

heavily invested shareholder onto a board

to help inform the board

00:00:59:02 - 00:01:01:11

decision making works very well.

00:01:01:11 - 00:01:04:19

The outperformance of the companies

we've worked with has ranged

00:01:04:19 - 00:01:08:08

between 40% and over 100% versus

their peer group.

BRIAN WELCH:

00:01:12:14 - 00:01:16:04

When we got involved in Air Products,

we saw an extraordinary opportunity,

00:01:16:04 - 00:01:17:20

which we kind of called chapter one.

00:01:18:06 - 00:01:19:23

Which was the basic corporate

00:01:19:23 - 00:01:24:01

kind of cost efficiency initiatives,

that we had identified in our diligence.

00:01:24:01 - 00:01:28:05

The company at the time had

operating margins in the mid-teens.

00:01:28:16 - 00:01:33:14

Its well-run peer, a company called Praxair

at the time had margins in the low 20s.

00:01:34:02 - 00:01:37:10

The primary issue with the company

was really a corporate bloat issue.

00:01:38:05 - 00:01:40:18

The company had been run

with a matrix structure, run

00:01:40:18 - 00:01:43:18

both by geography and by functional type.

00:01:44:06 - 00:01:47:03

And the company had a tremendous

opportunity, relatively low

00:01:47:03 - 00:01:51:13

risk and attractive,

to go after that, issue, and to clean up

00:01:51:13 - 00:01:55:07

the corporate efficiency issues

and deliver material margin expansion.

00:01:55:21 - 00:01:57:07

That was chapter one.

00:02:00:09 - 00:02:02:06

Chapter two was the longer term

playbook

00:02:02:06 - 00:02:05:17

of properly operating and optimizing

an industrial gas business.

00:02:05:18 - 00:02:06:11

And in our minds,

00:02:06:11 - 00:02:10:00

that really meant being very diligent

about the capital allocation.

00:02:10:07 - 00:02:14:04

This is a uniquely attractive business

model that has tremendous opportunity

00:02:14:04 - 00:02:18:05

to allocate capital

in a very high-return and low-risk manner.

00:02:18:21 - 00:02:22:22

And the second thing was really

a continuous improvement operating culture

00:02:23:07 - 00:02:27:19

that could deliver continuous margin

expansion and performance year after year.

PAUL HILAL:

00:02:28:05 - 00:02:32:00

So the shareholders who are excited

for holding this company

00:02:32:00 - 00:02:35:01

because of the very predictable,

no surprises,

00:02:35:09 - 00:02:38:09

low-risk cash flows of the core business,

00:02:38:13 - 00:02:42:08

they're not really excited

about adulterating that pure cash

00:02:42:08 - 00:02:46:02

flow stream with cash flow streams

with a different profile.

00:02:46:17 - 00:02:48:15

It just makes it less attractive.

00:02:48:15 - 00:02:52:00

so we hoped the board would be able

00:02:52:00 - 00:02:55:00

to find the right person

for that second chapter.

00:02:55:00 - 00:02:58:14

And as it turned out,

a lot of things went awry

00:02:59:08 - 00:03:02:08

and the board really didn't perform

the way it should.

00:03:02:10 - 00:03:05:03

Its composition deteriorated,

00:03:05:03 - 00:03:09:21

its internal processes, deteriorated.

00:03:10:13 - 00:03:12:11

Its structure became inappropriate,

00:03:13:15 - 00:03:16:05

and their performance on compensation,

00:03:16:05 - 00:03:19:14

on strategy and capital allocation,

all kind of went the wrong way.

BRIAN WELCH:

00:03:23:17 - 00:03:26:12

So the company in recent years has lost

its way a bit.

00:03:26:12 - 00:03:29:03

If you look at the five year

total shareholder return

00:03:29:03 - 00:03:32:03

in an industry of three,

the company is last.

00:03:32:03 - 00:03:35:03

It's delivered

about half of the second peer,

00:03:35:03 - 00:03:39:23

and it's delivered less than a third

of the well-run, best-in-class peer Linde.

00:03:40:03 - 00:03:43:03

And we think that's really due

to a couple principal reasons.

00:03:43:07 - 00:03:45:07

The first is succession.

00:03:45:07 - 00:03:48:23

The company has had

no clear path to a credible succession

00:03:48:23 - 00:03:51:23

plan for years,

and that's been a concern for investors.

00:03:52:12 - 00:03:55:17

The second primary issue has been capital

allocation.

00:03:56:03 - 00:03:59:08

The company's been allocating capital

in ways that are inconsistent

00:03:59:08 - 00:04:02:13

with the core business model.

With respect to the risk,

00:04:03:01 - 00:04:06:01

and that low risk, high return,

00:04:07:03 - 00:04:10:21

model, which is really the core foundation

of industrial gases.

00:04:11:08 - 00:04:14:22

The third issue is really the operating

efficiency of the core business.

00:04:14:22 - 00:04:18:18

And we think there's tremendous

opportunity with the right leadership to

00:04:18:18 - 00:04:22:12

maximize the efficiency of the business

and deliver better value for shareholders.

00:04:22:22 - 00:04:26:09

We think that properly benchmarked

the company has tremendous opportunity

00:04:26:09 - 00:04:28:01

relative to peers.

00:04:28:01 - 00:04:30:11

Its margins trail the best in class peer

00:04:30:11 - 00:04:33:11

Linde by over 450 basis points.

00:04:34:06 - 00:04:38:01

More importantly, its return on capital

is last in the industry of three

00:04:38:12 - 00:04:41:17

and is roughly half of the best in class

player, Linde.

00:04:41:17 - 00:04:45:05

So over the recent years,

by our estimates, the company has deployed

00:04:45:05 - 00:04:48:14

about $14 billion of capital

that has come onstream.

00:04:49:09 - 00:04:52:17

That capital, we believe, has delivered

just an 8% return,

00:04:53:13 - 00:04:56:04

less than the company's

stated hurdle rate.

00:04:56:04 - 00:05:00:04

And what makes industrial gases

so uniquely attractive is the high returns

00:05:00:04 - 00:05:03:04

and the low risk of the capital deployed.

00:05:03:08 - 00:05:07:15

And that comes with contracted customers,

that comes with basically

00:05:07:15 - 00:05:11:07

the absence of any macro uncertainty

or regulatory uncertainty.

00:05:11:20 - 00:05:15:09

Effectively, the gas companies contract

with other third parties

00:05:15:17 - 00:05:18:17

that help to basically fund

and underwrite the project,

00:05:18:17 - 00:05:22:02

and the responsibility of the gas company

is really just to build the plant

00:05:22:02 - 00:05:25:02

on time, on schedule and on budget.

00:05:25:04 - 00:05:29:05

And that allows them to deliver these

very exceptional returns with low risk.

00:05:29:17 - 00:05:32:23

Many of the company's recent projects

have been very large in magnitude,

00:05:33:10 - 00:05:36:09

and the characteristics of those projects

really haven't been aligned

00:05:36:09 - 00:05:40:14

with the core business,

meaning that the risks were outsized

00:05:40:14 - 00:05:43:05

relative to the core

industrial gas business.

00:05:43:05 - 00:05:46:20

Many of the recent projects have been done

in a much more speculative nature.

00:05:47:07 - 00:05:50:04

In other words, without customers

or perhaps doing activities

00:05:50:04 - 00:05:53:03

that are new to the company

and often of lesser quality.

00:05:53:10 - 00:05:56:06

Those have led to significant cost

and time

00:05:56:06 - 00:06:00:01

delays and issues

with the execution of the project.

00:06:00:08 - 00:06:03:08

And there remains

a lot of commercial uncertainty

00:06:03:08 - 00:06:06:20

about where the output of these projects

will ultimately be sold

00:06:06:23 - 00:06:09:21

and what returns will be delivered

to investors.

00:06:09:21 - 00:06:13:10

As challenges have arisen from

some of the company's recent projects,

00:06:13:19 - 00:06:16:08

the company's disclosures

have actually gotten worse,

00:06:16:08 - 00:06:20:01

and it's made it very challenging

for investors to properly analyze

00:06:20:11 - 00:06:23:13

and hold accountable

the management for their performance.

PAUL HILAL:

00:06:29:07 - 00:06:33:03

So a typical board of directors studies

the company and asks

00:06:33:03 - 00:06:37:09

what strategy is best for the company

to be most successful.

00:06:37:16 - 00:06:41:06

What strategy would enable the company

to drive the greatest appreciation

00:06:41:16 - 00:06:43:15

in the share value.

00:06:43:15 - 00:06:46:10

And then once you've figured out

that strategy, then typically

00:06:46:10 - 00:06:49:14

a board looks for the best

CEO to execute on that strategy.

00:06:50:15 - 00:06:54:08

And then the final step is constructing

a compensation system

00:06:54:21 - 00:06:57:21

that rewards the executive

and the executive team

00:06:58:13 - 00:07:00:22

for their performance

against that strategy.

00:07:00:22 - 00:07:04:07

So in this case,

what the company needs for

00:07:04:07 - 00:07:08:00

this second chapter is not the cost

cutting and the streamlining.

00:07:08:08 - 00:07:12:22

The company needs an executive

that can empower and develop the team

00:07:13:08 - 00:07:16:21

and create a deep, strong,

empowered bench of executives.

00:07:17:02 - 00:07:19:06

That's number one.

00:07:19:06 - 00:07:22:00

And then can help those executives

00:07:22:00 - 00:07:26:05

most successfully pursue

the optimal strategy for the company.

00:07:26:12 - 00:07:31:09

And it's clear that the optimal strategy

for this company is most fully

00:07:31:09 - 00:07:36:04

developing and mining the opportunities

in this very protected world

00:07:36:09 - 00:07:39:22

that only three companies in the world

can participate in, this very protected

00:07:40:05 - 00:07:43:05

set of low-risk, high-risk

adjusted returns.

00:07:43:23 - 00:07:47:08

There is no better strategy for a company

that's so privileged

00:07:47:08 - 00:07:49:11

that they can access

this very special pool

00:07:49:11 - 00:07:51:02

than to fully monetize it.

00:07:51:02 - 00:07:53:21

And then they need leadership

that has the skills,

00:07:54:05 - 00:07:57:05

the knowledge, the judgment

and the temperament

00:07:57:15 - 00:08:01:23

to properly underwrite,

you know, those opportunities.

00:08:01:23 - 00:08:06:20

And you also need a leader who has the skills and experience

and judgment to execute on them.

00:08:06:23 - 00:08:10:01

And then we want an incentive system

that's aligned for that executive,

00:08:10:01 - 00:08:14:12

and inevitably that would require, return

on invested capital of some measure.

00:08:14:22 - 00:08:17:07

So the board has gotten it backward

00:08:17:07 - 00:08:21:16

and it's all centered around,

keeping the CEO,

00:08:21:16 - 00:08:24:10

and what strategy is this

person able to execute,

00:08:24:10 - 00:08:25:20

and how do we compensate them

00:08:25:20 - 00:08:27:17

in a way that that person who get paid,

00:08:27:17 - 00:08:30:07

even if it's not what's

in the best interest of the shareholders.

00:08:30:07 - 00:08:32:08

And we think that

that should be revisited.

BRIAN WELCH:

00:08:33:00 - 00:08:37:06

We believe that today the company

can be worth more than $400 a share.

00:08:38:00 - 00:08:40:10

This will come from improved

operating efficiency

00:08:40:10 - 00:08:43:10

in the core business where we think

there's tremendous opportunity.

00:08:43:16 - 00:08:47:09

Properly benchmarked,

the company is trailing its well-run peer,

00:08:47:20 - 00:08:51:11

and we believe that new leadership

utilizing that exact playbook from that

00:08:51:11 - 00:08:55:05

best in class peer, can deliver

tremendous value to Air Products

00:08:55:05 - 00:08:56:21

over the short, medium and long term.

00:08:57:20 - 00:09:00:10

In addition, new leadership

00:09:00:10 - 00:09:04:07

can allocate capital in a way

that is consistent with the core business

00:09:04:16 - 00:09:05:07

and deliver

00:09:05:07 - 00:09:09:18

exceptional compounding for the business

over the years ahead with very low risk.

00:09:10:14 - 00:09:13:08

This will be reflected in the valuation

00:09:13:08 - 00:09:15:03

that the business would deserve to trade at,

00:09:15:03 - 00:09:17:01

and there's tremendous opportunity

00:09:17:01 - 00:09:20:06

to trade more in line

with the best in class peer, Linde.

00:09:20:15 - 00:09:23:01

These have been

some of the best performing companies

00:09:23:01 - 00:09:24:16

in all of industrials,

00:09:24:16 - 00:09:26:08

with respect to long term performance.

PAUL HILAL:

00:09:32:00 - 00:09:35:00

The clear best answer

for leading the company,

00:09:35:07 - 00:09:38:10

we think, is an executive that comes

00:09:38:15 - 00:09:41:04

with extensive training

and proven performance

00:09:41:12 - 00:09:45:21

in the gold standard industrial gas model,

the model that Dennis authored

00:09:46:04 - 00:09:49:19

at Praxair and that’s been practiced

at such a high level by Eduardo

00:09:49:19 - 00:09:51:07

and others at Praxair.

00:09:51:07 - 00:09:53:01

So if you like that strategy

00:09:53:01 - 00:09:55:21

and you think that's what's going

to make us successful,

00:09:55:21 - 00:09:59:23

then you want the executive leadership

to come from the best practitioner

00:09:59:23 - 00:10:01:00

of that strategy.

00:10:01:01 - 00:10:04:01

So I think that's what

the question is for the shareholders:

00:10:04:01 - 00:10:05:13

What do they want for the long term?

00:10:06:12 - 00:10:08:16

And then the secondary question is:

00:10:08:16 - 00:10:10:03

What does the near term look like?

00:10:10:11 - 00:10:13:11

And we think that causing this change now,

00:10:13:22 - 00:10:18:04

will reduce the uncertainty

among the executive ranks in the company.

00:10:18:12 - 00:10:20:21

It'll stem the hemorrhaging of talent.

00:10:20:21 - 00:10:23:20

And it will be

a beautiful rallying moment.

00:10:24:02 - 00:10:26:00

And we have seen this over and over again.

00:10:26:15 - 00:10:29:14

When you bring Michael Jordan

00:10:29:17 - 00:10:33:16

and Scottie Pippen to a basketball team

that's been floundering,

00:10:34:01 - 00:10:35:21

morale goes up pretty quickly.

00:10:36:01 - 00:10:37:09

At this moment in history,

00:10:38:00 - 00:10:41:03

when the company’s dealing with challenged

projects that need to be optimized,

00:10:41:14 - 00:10:44:19

and when the company's trying to face

its future, we're incredibly fortunate

00:10:45:05 - 00:10:47:20

that we have Dennis and Eduardo

at this moment in time.

00:10:47:20 - 00:10:49:07

that we have Dennis and Eduardo

at this moment in time.

00:10:50:00 - 00:10:53:07

They're available

and excited about engaging

00:10:53:07 - 00:10:56:07

with the company

and helping it get back on track.

00:10:56:17 - 00:10:57:19

We also have two other

00:10:57:19 - 00:11:01:01

very strong executives, that have nice

complementary perspectives.

00:11:01:04 - 00:11:05:07

Tracy and Drew bring enormously relevant

experiences,

00:11:05:17 - 00:11:08:16

diverse experiences

that we think are very complimentary

00:11:09:00 - 00:11:11:16

to the people

who would be ongoing on the board.

00:11:11:16 - 00:11:15:07

We offer the shareholders and the company

00:11:16:00 - 00:11:20:21

an opportunity

to have a fresh start at the board level.

00:11:21:22 - 00:11:25:08

Replacing these four directors with

00:11:25:08 - 00:11:27:11

the four that we propose,

00:11:27:11 - 00:11:31:20

we think will enable a page

to turn and a new chapter to begin.

00:11:32:08 - 00:11:35:22

This is about whether the shareholders

want this company

00:11:36:11 - 00:11:39:20

to continue

running as it is with the same board,

00:11:39:20 - 00:11:44:18

the same performance of the board,

the same a continuation of the status quo,

00:11:45:07 - 00:11:46:07

or whether the shareholders

00:11:46:07 - 00:11:48:23

think that there's a better way

to run this company.

00:11:48:23 - 00:11:51:23

They have examples of that better way

that they can look to,

00:11:52:06 - 00:11:53:13

and whether they want

00:11:53:13 - 00:11:54:15

someone who can help lead

00:11:54:15 - 00:11:59:01

the company with very low risk immediately

in that direction.

Exhibit 7

Video #6: “Board Reset to Drive Value”

PAUL HILAL:

00:00:04:22 - 00:00:07:17

We offer the shareholders

00:00:07:17 - 00:00:10:16

and the company an opportunity

00:00:10:16 - 00:00:14:03

to have a fresh start at the board level.

00:00:14:14 - 00:00:17:06

Replacing these four directors

with the

00:00:17:06 - 00:00:19:09

four that we propose,

00:00:19:09 - 00:00:23:18

we think will enable a page

to turn and a new chapter to begin.

00:00:24:08 - 00:00:28:14

we bring people

with outstanding and relevant expertise.

00:00:29:08 - 00:00:31:14

We bring one executive in particular, Mr.

00:00:31:14 - 00:00:36:09

Reilley who is exceptionally well-suited

to help guide,

00:00:36:21 - 00:00:39:19

the board in its discussions

and its deliberations

00:00:39:19 - 00:00:43:19

and also is exceptionally suited to coach

and advise the CEO.

00:00:44:11 - 00:00:45:20

So we have Dennis.

00:00:45:20 - 00:00:47:09

We have a shareholder.

00:00:47:09 - 00:00:50:16

We think that it's extraordinarily

valuable for a company

00:00:51:05 - 00:00:55:19

to have a deeply invested

shareholder with very aligned incentives,

00:00:56:05 - 00:01:00:12

who will be there for a very, very,

very long time, aligned

00:01:00:22 - 00:01:05:05

with their interests

that can see things through a shareholder’s prism.

00:01:05:05 - 00:01:07:22

And then, Tracy and Drew

00:01:08:06 - 00:01:12:23

bring enormously relevant experiences,

diverse experiences that we think

00:01:12:23 - 00:01:16:20

are very complementary to the people

who would be ongoing on the board.

00:01:17:04 - 00:01:20:04

And to the rest, we think it makes for

a very complete picture.

00:01:20:05 - 00:01:24:09

Among the most important things,

though, is the fact that the people

00:01:24:09 - 00:01:28:19

who are coming on are not being brought on

by the existing board.

00:01:29:03 - 00:01:31:12

This is not an extension

00:01:31:12 - 00:01:34:20

that makes it much easier

to have this fresh start with fresh eyes.

TRACY MCKIBBEN:

00:01:48:04 - 00:01:49:16

And when I join a board,

00:01:49:16 - 00:01:53:12

I think about what's the value

that I can bring to that board.

00:01:53:23 - 00:01:58:01

And I see that value being the

unique experience that I have. I've been

00:01:58:01 - 00:02:02:19

investing in the renewable energy, clean

technology, alternative energy space,

00:02:02:19 - 00:02:04:17

now for almost two decades.

00:02:04:17 - 00:02:09:04

I see myself as someone who focuses a lot

on new opportunities,

00:02:09:14 - 00:02:12:18

investing in unchartered territory.

00:02:13:02 - 00:02:17:00

However, using very consistent,

and tried and true,

00:02:17:06 - 00:02:22:16

risk-mitigated models

for how we invest in our companies.

00:02:23:01 - 00:02:26:01

My background is I'm a lawyer by training.

00:02:26:03 - 00:02:30:17

I began my career at a large,

major international law firm.

00:02:31:00 - 00:02:34:08

I've also served in government,

where I did policy

00:02:34:08 - 00:02:37:10

work at the National Security Council

in the White House.

00:02:37:17 - 00:02:40:07

I also have experience

in the finance industry.

00:02:40:07 - 00:02:43:00

I started the environmental

banking strategy

00:02:43:00 - 00:02:44:06

at Citigroup.

00:02:44:17 - 00:02:48:18

And so my experience

and what I bring to the company

00:02:48:18 - 00:02:52:19

is all of that

legal policy, finance perspective,

00:02:53:03 - 00:02:56:18

that I think helps me see opportunities

that others may not be able to see.

ANDREW EVANS:

00:02:57:00 - 00:03:01:04

I’m delighted to be considered

for the Board of Air Products.

00:03:01:04 - 00:03:03:06

It's a very interesting business to me.

00:03:03:06 - 00:03:05:01

And very capital intensive,

00:03:05:01 - 00:03:08:09

much like the businesses

I've operated for the last 30 years.

00:03:08:18 - 00:03:11:16

Throughout my career,

I've been a Treasurer, a Chief

00:03:11:16 - 00:03:15:10

Financial Officer, a Chief Operating

Officer and a Chief Executive Officer

00:03:16:00 - 00:03:19:21

in largely capital

intensive public utility businesses.

00:03:19:21 - 00:03:26:20

I've overseen construction from everything from underground salt dome

storage caverns to nuclear power plants,

00:03:27:01 - 00:03:31:20

and I understand the risks and returns

and rewards from operating

00:03:31:20 - 00:03:36:02

in capital intensive businesses

in all types of markets.

00:03:36:02 - 00:03:39:20

I think much like in public utilities,

when you start with a base

00:03:39:20 - 00:03:42:09

where return

is relatively straightforward,

00:03:42:09 - 00:03:47:04

where risk-adjusted returns

are known and measurable,

00:03:47:04 - 00:03:51:05

as you start to stretch into businesses

that are more merchant related,

00:03:51:05 - 00:03:55:08

much like hydrogen, or much like

independent power production.

00:03:55:14 - 00:03:58:09

There's a much different set

of construction parameters

00:03:58:09 - 00:04:01:13

and risk parameters

associated with these types of projects

00:04:01:13 - 00:04:06:07

much different than what the base

expectation was out of a core utility

00:04:06:07 - 00:04:10:22

or core elemental product like Air Products works within.

00:04:11:17 - 00:04:15:13

When you move into businesses

like that, a different structure

00:04:15:13 - 00:04:17:14

has to take place

and a different expectation

00:04:17:14 - 00:04:20:18

about how you’ll manage

risks has to be formulated.

PAUL HILAL:

00:04:21:09 - 00:04:24:09

Dennis's value here is multi-dimensional.

00:04:24:09 - 00:04:26:09

First,

he knows the gas business incredibly well.

00:04:26:09 - 00:04:28:20

He was the author of what many consider

00:04:28:20 - 00:04:30:07

the gold standard operating model

00:04:30:07 - 00:04:31:20

for the industrial gas industry.

00:04:32:08 - 00:04:33:14

And it's clear that it works.

00:04:33:14 - 00:04:38:05

It's a combination of culture

and various kinds of internal processes,

00:04:38:14 - 00:04:42:13

and frameworks

for analyzing things, etc..

00:04:42:19 - 00:04:45:10

So he's the author of it

and a great practitioner of it,

00:04:45:22 - 00:04:47:21

that is a very tremendous asset.

00:04:47:21 - 00:04:52:16

But also the diversity of his

background, is very relevant.

00:04:53:00 - 00:04:54:00

His work in the commodity

00:04:54:00 - 00:04:57:07

chemical area, as a customer

of an industrial gas company is a plus.

00:04:57:20 - 00:05:00:08

His work in the energy sector

as a director

00:05:00:08 - 00:05:03:08

of great consequence, is a big plus.

00:05:03:13 - 00:05:09:19

He's also an incredibly impressive

and effective board operator.

DENNIS REILLEY:

00:05:10:10 - 00:05:14:03

One of the atmospherics

of every board I've ever been

00:05:14:03 - 00:05:18:17

on, and I've served on 7

or 8 boards in my life,

00:05:19:17 - 00:05:22:16

there's a tendency for management

to come in and sell,

00:05:23:12 - 00:05:25:06

and I've always been opposed to that.

00:05:25:06 - 00:05:29:02

In fact,

I've often told my my own organizations

00:05:29:23 - 00:05:32:23

don't come to the board

meeting to sell anything.

00:05:33:12 - 00:05:36:12

Save your sales skills for the outside

00:05:36:23 - 00:05:39:12

where they belong.

00:05:39:12 - 00:05:41:01

You come to the board

00:05:41:01 - 00:05:44:01

to convey information and facts,

00:05:44:17 - 00:05:46:21

and you do that

00:05:46:21 - 00:05:50:09

by talking about the

good, the bad, and the ugly.

00:05:51:02 - 00:05:55:01

And I think if you can create a culture

like that in the boardroom

00:05:55:20 - 00:05:58:11

where board members are encouraged

00:05:58:11 - 00:06:02:21

and they are elicited to probe

and ask questions,

00:06:03:15 - 00:06:05:23

And if you combine

that kind of environment

00:06:07:04 - 00:06:09:04

with management coming in

00:06:09:04 - 00:06:12:22

not to sell,

but to convey facts and information,

00:06:13:11 - 00:06:18:10

you can have an extremely,

positive meetings

00:06:18:10 - 00:06:21:21

that lead to a lot of excellent decisions

being made.

PAUL HILAL:

00:06:22:08 - 00:06:25:06

Mantle Ridge is a team.

It's not one person.

00:06:25:06 - 00:06:28:06

And so one Mantle

Ridge person is on a board,

00:06:28:13 - 00:06:33:03

one gets the benefit of the resources

of a very deep team.

00:06:33:03 - 00:06:36:03

And those of you who have seen

the quality of our work

00:06:36:03 - 00:06:39:23

in our projects in the past,

those of you who have visited the deck,

00:06:40:05 - 00:06:42:20

you can imagine the amount of work and

understanding

00:06:42:20 - 00:06:48:04

that we've put into this

and the level of information

00:06:48:12 - 00:06:51:06

we can inject into board deliberations

00:06:51:06 - 00:06:54:01

to enable the directors

to make more informed choices.

DENNIS REILLEY:

00:06:54:01 - 00:06:57:04

I think from the outside looking in,

you often think these things

00:06:57:04 - 00:06:58:03

will be more difficult

00:06:58:03 - 00:07:01:10

than they are in terms of the integrating

of the board of directors.

00:07:01:21 - 00:07:04:21

I've found it in

three cases to be just the opposite.

00:07:05:01 - 00:07:08:01

Does it take a little work? Sure it does.

00:07:08:02 - 00:07:11:03

But things come together

a lot quicker than you think they might.

TRACY MCKIBBEN:

00:07:12:01 - 00:07:14:21

So what

I try to do is work collaboratively

00:07:14:21 - 00:07:18:14

with all of the directors to achieve

ultimately what we all want to achieve,

00:07:18:21 - 00:07:22:14

which is to help the company

grow, help the company be sustainable

00:07:22:22 - 00:07:26:16

and also meet shareholder

demands and expectations.

ANDREW EVANS:

00:07:27:03 - 00:07:31:06

I have seen shareholder

driven board refreshment from both sides.

00:07:31:06 - 00:07:33:21

And I view that it can be

highly constructive,

00:07:33:21 - 00:07:36:00

particularly in this setting.

00:07:36:00 - 00:07:39:18

One of the reasons I signed up for

this was because I had a chance

00:07:39:18 - 00:07:43:11

to take a look at my fellow nominees,

and I'm very comfortable

00:07:43:11 - 00:07:48:04

that this is a constructive

and productive group of individuals

00:07:48:04 - 00:07:51:13

who will work harmoniously

within an existing board of directors.

PAUL HILAL:

00:07:51:21 - 00:07:56:08

We feel that the proposed,

board refreshment

00:07:56:16 - 00:08:00:00

with four strong independent nominees,

including a shareholder,

00:08:00:14 - 00:08:03:09

and including a person who authored

00:08:03:09 - 00:08:07:13

what many consider the gold standard model

for industrial gases and two other

00:08:07:13 - 00:08:10:19

very strong executives

that have nice complementary perspectives.

00:08:11:10 - 00:08:15:11

We feel that a board refreshment

of putting those executives on the board

00:08:15:20 - 00:08:17:00

and also retiring

00:08:17:00 - 00:08:20:09

the ones that have been specified,

we believe that that will be sufficient

00:08:20:22 - 00:08:23:18

to send the message to the board

00:08:23:18 - 00:08:26:18

that the shareholders want things to go

in a different direction,

00:08:26:18 - 00:08:30:03

and based on past experience,

if that message is sent,

00:08:31:01 - 00:08:34:11

the board will continue,

you know, harmoniously, quite quickly

00:08:34:23 - 00:08:37:09

and do the work that they're there to do,

00:08:37:09 - 00:08:38:12

which is to create value

00:08:38:12 - 00:08:40:02

for the shareholders

and protect the company.

Exhibit 8

Video #7: “The Path Forward”

DENNIS REILLEY:

00:00:38:06 - 00:00:41:06

The industrial gases industry

00:00:41:21 - 00:00:44:14

is in many ways a gifted industry.

00:00:44:14 - 00:00:47:15

It has some strengths about it

that just aren't

00:00:47:15 - 00:00:50:15

evident in a lot of industries.

00:00:50:20 - 00:00:53:15

And if run correctly,

00:00:53:15 - 00:00:57:21

they can be quite rewarding enterprises

for their shareholders.

00:00:58:12 - 00:00:59:03

There is a

00:00:59:03 - 00:01:04:03

uniqueness in the industrial gases

business that it's really

00:01:04:03 - 00:01:09:10

a specialty business,

much more than it is a commodity business.

00:01:10:04 - 00:01:13:08

And it's understanding

that, it's understanding

00:01:13:08 - 00:01:16:13

the value of the take-or-pay business model.

00:01:17:10 - 00:01:20:09

It's also understanding

one of the unique things

00:01:20:09 - 00:01:25:03

about the industrial gases business

is the product does not move well.

00:01:26:06 - 00:01:29:11

That's a great advantage for the industry,

quite frankly.

00:01:29:22 - 00:01:34:20

When you think about the pipeline aspects

of the business, there aren't too many

00:01:35:10 - 00:01:38:14

industrial gases pipelines

that run more than a few hundred

00:01:38:14 - 00:01:41:14

miles one direction or the other.

00:01:41:15 - 00:01:45:02

And a great deal of the business

is just on-site business.

00:01:45:10 - 00:01:49:08

When the industry builds a plant

on the site of one of its customers

00:01:49:14 - 00:01:54:05

and serves its customers uniquely. So,

it is a different structure,

00:01:54:22 - 00:01:58:09

but the beauty of it,

it gives you the ability to organize

00:01:58:09 - 00:02:03:10

your industrial gas business

around a lot of local markets.

00:02:04:09 - 00:02:07:08

You can almost think about it as

00:02:07:11 - 00:02:10:09

a series of concentric circles,

00:02:10:09 - 00:02:13:15

with a 250 to 300 mile radius.

00:02:14:01 - 00:02:19:03

If you organize correctly,

you can do it in a way where

00:02:19:09 - 00:02:22:18

each one of those pockets

can have their own income statement,

00:02:23:13 - 00:02:25:21

their own balance sheet,

00:02:25:21 - 00:02:28:21

and can run them very, very tightly.

00:02:29:10 - 00:02:32:06

They can have their own return on capital

goals.

00:02:32:06 - 00:02:34:11

They can have their own margin goals.

00:02:34:11 - 00:02:37:13

And it gives you a great ability

to run this business

00:02:38:06 - 00:02:40:03

in a much tighter way.

EDUARDO MENEZES:

00:02:45:17 - 00:02:48:08

I'd like to say that

there are three pillars of that,

00:02:48:08 - 00:02:51:13

you need to think about organization,

processes and people.

00:02:51:23 - 00:02:57:05

So in terms of organization,

we like to break down the business

00:02:57:05 - 00:03:02:23

into small manageable units

that you can have full control

00:03:02:23 - 00:03:05:23

of your financial statements

and balance sheet.

00:03:06:01 - 00:03:10:13

So we want the business owners

to really own that,

00:03:10:13 - 00:03:12:17

that profit and loss or P&L.

00:03:12:17 - 00:03:15:17

From that organization,

00:03:15:17 - 00:03:18:15

then you need to think about the processes

you're going to use to,

00:03:18:15 - 00:03:20:21

to manage that on the day to day.

00:03:20:21 - 00:03:25:09

So I would say that you need to

have people that can

00:03:25:16 - 00:03:30:11

understand the details of the business,

that can explain the numbers every month

00:03:30:11 - 00:03:34:13

and then can

explain the gaps for the plan

00:03:34:13 - 00:03:37:17

and how they will close any gap

00:03:37:17 - 00:03:40:17

they have to the plan that they established

at the beginning of the year.

00:03:40:19 - 00:03:43:19

So this is for the financial performance

of the business.

00:03:44:03 - 00:03:46:06

For CapEx it’s not different from that.

00:03:46:06 - 00:03:47:09

You need to

00:03:47:09 - 00:03:51:22

make sure that the business unit

owns the project from crib to cradle.

00:03:52:02 - 00:03:55:00

So they, you know,

they are completely in charge

00:03:55:00 - 00:03:58:15

of all the assumptions that you put

in the business model to justify

00:03:58:15 - 00:04:02:16

that investment, that they follow

the construction of the plant and they,

00:04:03:00 - 00:04:06:09

you know, ensure that the plant is built

on time and on budget.

00:04:06:16 - 00:04:10:15

And when you go to operations that,

you know, the sales and profitability

00:04:10:15 - 00:04:14:03

that you have in the business

model are really achieved

00:04:14:10 - 00:04:15:22

once you start the plant.

00:04:43:03 - 00:04:47:04

You need to have the right people at the right places and

00:04:47:04 - 00:04:49:23

that's a work that never ends. You are always

00:04:49:23 - 00:04:52:22

trying to identify the best people you can

00:04:53:05 - 00:04:56:19

to occupy these management functions of these

00:04:56:19 - 00:04:58:21

regional P&Ls that you have.

00:04:59:03 - 00:05:02:02

And I would say that we expect people to be

00:05:02:02 - 00:05:04:19

to have attention to details, to know the numbers,

00:05:04:19 - 00:05:07:15

to have operational discipline,

00:05:07:15 - 00:05:14:12

not only to be able to report their numbers,

but also to cascade this process into their own organization.

00:05:14:12 - 00:05:21:11

I expect them to be ambitious, but at the same time

humble, to understand that they cannot control

00:05:21:11 - 00:05:23:17

every aspect of the business,

00:05:23:17 - 00:05:27:20

and that they are curious and they

try to learn something new every day.

00:05:27:20 - 00:05:31:06

I think if you have that kind of profile,

you will do well in a

00:05:31:06 - 00:05:34:14

first-class organization in industrial gases.

DENNIS REILLEY:

00:05:34:14 - 00:05:37:13

First of all,

you have to be able to understand

00:05:38:00 - 00:05:41:12

that getting bigger

doesn't always make you better.

00:05:43:03 - 00:05:44:20

That's a trap

00:05:44:20 - 00:05:47:20

that a lot of businesses and fall into,

00:05:48:19 - 00:05:50:21

and it generally rears

00:05:50:21 - 00:05:53:21

its ugly head

when you measure return on capital

00:05:54:16 - 00:05:59:02

because you could spend money, you can buy

earnings, you can buy earnings,

00:05:59:13 - 00:06:01:06

but you have to always be careful

00:06:01:06 - 00:06:04:14

you're not buying them

at a declining return.

00:06:05:03 - 00:06:09:04

So that's one of the first things

I hold very near and dear to my heart.

00:06:09:14 - 00:06:12:09

There's always ways to grow in the core.

00:06:12:09 - 00:06:13:18

You have to be quick enough.

00:06:13:18 - 00:06:15:05

You've got to be thoughtful enough.

00:06:15:05 - 00:06:18:19

You've got to be creative enough

to figure out how to do that.

00:06:19:11 - 00:06:21:00

Now, is there

00:06:21:00 - 00:06:24:08

a situation where you might do something

that's a little outside the core?

00:06:24:13 - 00:06:26:16

You can, you can.

00:06:26:16 - 00:06:29:05

You never completely

take that off the table.

00:06:29:05 - 00:06:33:02

But be very careful

what you're asking your organization to do

00:06:33:17 - 00:06:36:05

when it's brand new,

00:06:36:05 - 00:06:39:23

when they don't have the experience of it

and whatever you do,

00:06:40:16 - 00:06:44:13

don't give up the business

model that has made you

00:06:45:14 - 00:06:48:02

and your industry successful,

00:06:48:02 - 00:06:50:17

which in the cases of industrial gas

00:06:50:17 - 00:06:53:08

is the take-or-pay business model.

00:06:53:08 - 00:06:55:22

It's a very unique model

00:06:55:22 - 00:06:58:15

and when run correctly

00:06:58:15 - 00:07:01:06

it can do great things

for your shareholders.

Exhibit 9

Video #8: “Meet Proposed CEO Candidate Eduardo Menezes”

EDUARDO MENEZES:

00:00:07:21 - 00:00:10:21

My name is Eduardo Menezes. I'm 61.

00:00:11:04 - 00:00:13:18

I have been working in industrial gases

00:00:13:18 - 00:00:16:12

since I got out of school,

chemical engineering school.

00:00:17:02 - 00:00:20:17

I love the fact

that one day you may be talking about,

00:00:21:05 - 00:00:25:17

you know, a small transaction in cylinder

gases or hard goods,

00:00:25:17 - 00:00:28:11

and the next day you’re

talking about a very large agreement

00:00:28:11 - 00:00:33:15

with a steel mill, or semiconductor

plant or chemical customer.

00:00:34:02 - 00:00:37:15

And this allows me to learn something

00:00:37:15 - 00:00:39:13

new every day,

which is very important for me.

00:00:39:13 - 00:00:42:16

Being able to build

00:00:42:16 - 00:00:46:13

new businesses, to bring the people that

00:00:46:13 - 00:00:48:17

work with you to work as a team

00:00:48:17 - 00:00:50:07

to accomplish the results

00:00:50:15 - 00:00:54:02

they have to accomplish.

I think is very rewarding for you.

00:00:54:02 - 00:00:55:05

I think it's,

00:00:55:05 - 00:00:58:18

you know, I have the opportunity

of doing that in many different countries.

00:00:58:18 - 00:01:02:13

I worked in Mexico, in Spain, in Germany,

00:01:02:13 - 00:01:04:11

in seven, eight different cities in the U.S.,

00:01:04:11 - 00:01:06:02

and in Brazil.

00:01:06:02 - 00:01:09:16

I’m very proud that I made a lot of friends

during these years

00:01:09:16 - 00:01:13:00

and I was able to contribute

for a lot of these businesses to grow.

00:01:13:00 - 00:01:17:02

You need to have the right people at

the right places, and

00:01:17:02 - 00:01:23:17

that's a work that never ends. You are always

trying to identify the best people you can.

00:01:23:17 - 00:01:29:10

to occupy the management functions

of these regional P&Ls that you have.

00:01:29:10 - 00:01:33:19

And I would say that we expect people

to have attention to details,

00:01:33:19 - 00:01:37:19

to know the numbers,

to have operational discipline.

00:01:37:19 - 00:01:44:17

Not only to be able to report their numbers, but also to cascade this

process into their own organization.

00:01:44:17 - 00:01:48:02

I expect them to be ambitious,

00:01:48:02 - 00:01:53:14

but at the same time humble to understand that

they cannot control every aspect of the business.

00:01:54:00 - 00:01:56:02

First thing you have to do

is to be humble,

00:01:56:02 - 00:01:58:13

you need to listen,

you need to understand.

00:01:58:13 - 00:02:01:15

And once you do that,

then you are able to

00:02:02:00 - 00:02:04:20

propose some changes

and try to guide the organization

00:02:04:20 - 00:02:08:19

through to,

you know, work in a way that you think

00:02:08:19 - 00:02:11:19

it's going to be more profitable

for the company.

00:02:12:03 - 00:02:15:10

You know, the leading by example

is much more important than the words

00:02:15:10 - 00:02:16:16

you can tell people.

00:02:16:16 - 00:02:19:02

Discipline,

00:02:19:02 - 00:02:22:19

being humble, listen to people,

00:02:22:19 - 00:02:26:10

try to have empathy for the situation,

for everyone is important.

00:02:26:21 - 00:02:30:00

And at the same time, you know,

keeping the targets that you have

00:02:30:00 - 00:02:33:12

with the shareholders, the owners

of the company, it's also critical.

00:02:33:12 - 00:02:35:17

So you need to balance

all of these things.

00:02:35:17 - 00:02:38:23

You need to look forward and

my objective here

00:02:39:04 - 00:02:40:08

if I get this opportunity

00:02:40:08 - 00:02:44:02

by the board of Air Products

is to dedicate myself to this business

00:02:44:02 - 00:02:48:13

and to accomplish,

you know, even better things in the future.

00:02:48:17 - 00:02:50:14

There is always opportunity.

00:02:50:14 - 00:02:53:18

If you cannot find it, it’s because you're not looking hard enough.

Exhibit 10

Video #9: “Former Executive Vice President of Praxair, Ricardo

Malfitano on Eduardo Menezes”

PAUL HILAL:

00:00:00:00 - 00:00:03:13

If you have an opportunity to work

with someone like Eduardo Menezes

00:00:03:13 - 00:00:04:20

you don't think twice.

00:00:07:07 - 00:00:10:15

Eduardo, he enhances performance.

00:00:10:21 - 00:00:13:04

He's not a risk

creating disrupter.

00:00:13:06 - 00:00:14:17

He's an accelerator.

RICARDO MALFITANO:

00:00:14:23 - 00:00:22:02

I met Eduardo in 1986. We were assigned to work together,

00:00:22:02 - 00:00:25:20

in the same group, which we call on-site business,

00:00:25:20 - 00:00:29:02

which are our largest customers.

00:00:29:10 - 00:00:30:18

I’ll tell you what

00:00:30:20 - 00:00:34:00

that inspired me myself, it’s his knowledge.

00:00:34:11 - 00:00:37:02

I don't know how somebody can process

00:00:37:02 - 00:00:39:04

as much information as Eduardo.

00:00:39:04 - 00:00:40:12

I think the best

00:00:41:15 - 00:00:44:04

example of how Eduardo works

00:00:44:04 - 00:00:47:09

with a group of people that

00:00:47:09 - 00:00:50:16

either he's new to or they are new to him,

00:00:50:23 - 00:00:54:18

is when Linde and Praxair merged,

00:00:55:12 - 00:00:58:12

they have a very challenging

00:00:58:20 - 00:01:01:12

synergy plan.

00:01:01:12 - 00:01:05:18

Where to capture synergies,

where to generate this value

00:01:06:08 - 00:01:09:21

that will make economically,

the merger make sense, you know,

00:01:10:17 - 00:01:12:23

and Eduardo at that point was assigned

00:01:12:23 - 00:01:16:12

to run the European business,

which was the largest business

00:01:16:12 - 00:01:18:19

in the merger of companies.

00:01:18:19 - 00:01:21:01

If I'm not wrong, it's about €8 billion.

00:01:21:01 - 00:01:26:09

And in over three years

with the organization he had there,

00:01:26:22 - 00:01:29:22

he was able to generate the synergies,

00:01:30:06 - 00:01:32:14

affect both the plan level

00:01:32:14 - 00:01:35:13

synergies for the company.

00:01:35:23 - 00:01:39:04

And not only that, the improvement

of the operating profit

00:01:39:04 - 00:01:41:16

margin of the business was way beyond

00:01:41:16 - 00:01:45:10

what the plans for the merger

would consider at that time.

00:01:45:10 - 00:01:50:10

So, you know, he can work with

different organizations really well.

00:01:50:10 - 00:01:52:13

Well accepted, well respected

00:01:53:00 - 00:01:57:19

and most important in my mind,

the way he conducts himself, the maturity,

00:01:58:11 - 00:02:02:08

you know, the willingness to

to listen, to adapt,

00:02:02:18 - 00:02:06:22

that's what creates trust, and engages

people to work with him.

DENNIS REILLEY:

00:02:07:12 - 00:02:11:05

Probably among the quickest studies

00:02:12:04 - 00:02:14:23

of any individual I've ever been around.

00:02:14:23 - 00:02:17:23

His ability to, glean information,

00:02:18:17 - 00:02:22:10

absorb information,