false

FY

0001156041

P10Y

P10Y

P10Y

P10Y

0001156041

2024-01-01

2024-12-31

0001156041

2024-12-31

0001156041

2025-02-21

0001156041

2023-12-31

0001156041

2023-01-01

2023-12-31

0001156041

us-gaap:CommonStockMember

2022-12-31

0001156041

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001156041

us-gaap:RetainedEarningsMember

2022-12-31

0001156041

2022-12-31

0001156041

us-gaap:CommonStockMember

2023-12-31

0001156041

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001156041

us-gaap:RetainedEarningsMember

2023-12-31

0001156041

us-gaap:CommonStockMember

2023-01-01

2023-12-31

0001156041

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001156041

us-gaap:RetainedEarningsMember

2023-01-01

2023-12-31

0001156041

us-gaap:CommonStockMember

2024-01-01

2024-12-31

0001156041

us-gaap:AdditionalPaidInCapitalMember

2024-01-01

2024-12-31

0001156041

us-gaap:RetainedEarningsMember

2024-01-01

2024-12-31

0001156041

us-gaap:CommonStockMember

2024-12-31

0001156041

us-gaap:AdditionalPaidInCapitalMember

2024-12-31

0001156041

us-gaap:RetainedEarningsMember

2024-12-31

0001156041

us-gaap:OilAndGasMember

2024-01-01

2024-12-31

0001156041

us-gaap:OilAndGasMember

2023-01-01

2023-12-31

0001156041

us-gaap:OfficeEquipmentMember

2020-01-01

0001156041

us-gaap:OfficeEquipmentMember

2024-12-31

0001156041

us-gaap:OfficeEquipmentMember

2023-12-31

0001156041

us-gaap:WarrantMember

2024-01-01

2024-12-31

0001156041

us-gaap:WarrantMember

2023-01-01

2023-12-31

0001156041

us-gaap:EmployeeStockOptionMember

2024-01-01

2024-12-31

0001156041

us-gaap:EmployeeStockOptionMember

2023-01-01

2023-12-31

0001156041

HUSA:OilSalesMember

2024-01-01

2024-12-31

0001156041

HUSA:OilSalesMember

2023-01-01

2023-12-31

0001156041

HUSA:NaturalGasSalesMember

2024-01-01

2024-12-31

0001156041

HUSA:NaturalGasSalesMember

2023-01-01

2023-12-31

0001156041

HUSA:NaturalGasLiquidsSalesMember

2024-01-01

2024-12-31

0001156041

HUSA:NaturalGasLiquidsSalesMember

2023-01-01

2023-12-31

0001156041

country:US

2024-12-31

0001156041

srt:SouthAmericaMember

2024-12-31

0001156041

country:US

2023-12-31

0001156041

srt:SouthAmericaMember

2023-12-31

0001156041

HUSA:TwoThousandAndEightEquityIncentivePlanMember

srt:MaximumMember

2008-12-31

0001156041

HUSA:TwoThousandAndSeventeenEquityIncentivePlanMember

srt:MaximumMember

2017-12-31

0001156041

HUSA:TwoThousandAndTwentyOneEquityIncentivePlanMember

srt:MaximumMember

2021-12-31

0001156041

HUSA:DirectorsMember

2023-06-01

2023-06-30

0001156041

HUSA:DirectorsMember

2023-06-30

0001156041

HUSA:DirectorsMember

2024-06-01

2024-06-30

0001156041

HUSA:DirectorsMember

2024-06-30

0001156041

srt:ChiefExecutiveOfficerMember

2024-11-01

2024-11-30

0001156041

srt:ChiefExecutiveOfficerMember

2024-11-30

0001156041

srt:ChiefExecutiveOfficerMember

2024-12-31

0001156041

srt:ChiefExecutiveOfficerMember

2024-12-01

2024-12-31

0001156041

HUSA:SalesAgreementTwoThousandTwentyTwoATMOfferingMember

HUSA:WestParkCapitalLLCMember

srt:MaximumMember

2022-11-01

2022-11-30

0001156041

HUSA:SalesAgreementTwoThousandTwentyTwoATMOfferingMember

2023-01-01

2023-12-31

0001156041

HUSA:SalesAgreementTwoThousandTwentyTwoATMOfferingMember

2024-01-01

2024-12-31

0001156041

HUSA:TwoThousandTwentyOneATMOfferingMember

2024-01-01

2024-12-31

0001156041

HUSA:BridgeLoanWarrantsMember

2019-09-01

2019-09-30

0001156041

HUSA:BridgeLoanWarrantsMember

2019-09-30

0001156041

srt:MinimumMember

2024-01-01

2024-12-31

0001156041

srt:MaximumMember

2024-01-01

2024-12-31

0001156041

HUSA:OperatingLeaseAgreementMember

2024-01-01

2024-12-31

0001156041

HUSA:OperatingLeaseAgreementMember

2024-12-31

0001156041

us-gaap:GeneralAndAdministrativeExpenseMember

2024-01-01

2024-12-31

0001156041

us-gaap:GeneralAndAdministrativeExpenseMember

2023-01-01

2023-12-31

0001156041

2013-08-01

2013-08-31

0001156041

country:CO

HUSA:CurrentDirectorMember

2024-01-01

2024-12-31

0001156041

srt:NorthAmericaMember

srt:ReportableGeographicalComponentsMember

2024-01-01

2024-12-31

0001156041

srt:NorthAmericaMember

srt:ReportableGeographicalComponentsMember

2024-12-31

0001156041

srt:NorthAmericaMember

srt:ReportableGeographicalComponentsMember

2023-01-01

2023-12-31

0001156041

srt:NorthAmericaMember

srt:ReportableGeographicalComponentsMember

2023-12-31

0001156041

srt:ReportableGeographicalComponentsMember

srt:SouthAmericaMember

2024-01-01

2024-12-31

0001156041

srt:SouthAmericaMember

srt:ReportableGeographicalComponentsMember

2024-12-31

0001156041

srt:ReportableGeographicalComponentsMember

srt:SouthAmericaMember

2023-01-01

2023-12-31

0001156041

srt:SouthAmericaMember

srt:ReportableGeographicalComponentsMember

2023-12-31

0001156041

us-gaap:SubsequentEventMember

HUSA:ShareExchangeAgreementMember

2025-02-20

2025-02-20

0001156041

us-gaap:SubsequentEventMember

HUSA:ShareExchangeAgreementMember

2025-02-20

0001156041

us-gaap:SubsequentEventMember

2025-01-01

2025-01-31

0001156041

srt:ChiefExecutiveOfficerMember

us-gaap:SubsequentEventMember

2025-01-01

2025-01-31

0001156041

HUSA:BoardMember

us-gaap:SubsequentEventMember

2025-01-01

2025-01-31

0001156041

srt:ChiefExecutiveOfficerMember

us-gaap:SubsequentEventMember

2025-02-01

2025-02-28

0001156041

srt:NorthAmericaMember

2024-01-01

2024-12-31

0001156041

srt:NorthAmericaMember

2023-01-01

2023-12-31

0001156041

srt:SouthAmericaMember

2024-01-01

2024-12-31

0001156041

srt:SouthAmericaMember

2023-01-01

2023-12-31

0001156041

country:US

srt:NaturalGasReservesMember

2022-12-31

0001156041

country:US

srt:OilReservesMember

2022-12-31

0001156041

country:US

srt:NaturalGasLiquidsReservesMember

2022-12-31

0001156041

country:US

srt:NaturalGasReservesMember

2023-01-01

2023-12-31

0001156041

country:US

srt:OilReservesMember

2023-01-01

2023-12-31

0001156041

country:US

srt:NaturalGasLiquidsReservesMember

2023-01-01

2023-12-31

0001156041

country:US

srt:NaturalGasReservesMember

2023-12-31

0001156041

country:US

srt:OilReservesMember

2023-12-31

0001156041

country:US

srt:NaturalGasLiquidsReservesMember

2023-12-31

0001156041

country:US

srt:NaturalGasReservesMember

2024-01-01

2024-12-31

0001156041

country:US

srt:OilReservesMember

2024-01-01

2024-12-31

0001156041

country:US

srt:NaturalGasLiquidsReservesMember

2024-01-01

2024-12-31

0001156041

country:US

srt:NaturalGasReservesMember

2024-12-31

0001156041

country:US

srt:OilReservesMember

2024-12-31

0001156041

country:US

srt:NaturalGasLiquidsReservesMember

2024-12-31

0001156041

country:US

2024-01-01

2024-12-31

0001156041

srt:SouthAmericaMember

2022-12-31

0001156041

country:US

2023-01-01

2023-12-31

0001156041

country:US

2022-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

utr:bbl

utr:Mcf

utr:gal

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

☒

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the Fiscal Year Ended December 31, 2024

☐

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the transition period from to

Commission

File No. 1-32955

HOUSTON

AMERICAN ENERGY CORP.

(Exact

name of registrant specified in its charter)

| Delaware |

|

76-0675953 |

(State

or other jurisdiction of

incorporation

or organization) |

|

(I.R.S.

Employer

Identification

No.) |

801

Travis Street, Suite 1425, Houston, Texas 77002

(Address

of principal executive offices)(Zip code)

Issuer’s

telephone number, including area code: (713) 222-6966

Securities

registered pursuant to Section 12(b) of the Act:

Title

of each class

|

|

Trading

Symbol |

|

Name

of each exchange on which registered

|

| Common

Stock, $0.001 par value |

|

HUSA |

|

NYSE

American |

Securities

registered pursuant to Section 12(g) of the Act:

None

(Title

of Class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No

☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No

☒

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging growth company. See definition of “accelerated filer,” “large accelerated filer,” “smaller

reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer |

☐ |

Accelerated

filer |

☐ |

Non-accelerated

filer |

☒ |

| Smaller

reporting company |

☒ |

Emerging

growth company |

☐ |

|

|

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to o § 240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The

aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant on December 31, 2024, based on

the closing sales price of the registrant’s common stock on that date, was $17,666,820. Shares of common stock held by each current

executive officer and director and by each person known by the registrant to own 10% or more of the outstanding common stock have been

excluded from this computation in that such persons may be deemed to be affiliates.

The

number of shares of the registrant’s common stock, $0.001 par value, outstanding as of February 21, 2025 was 15,686,533.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the Company’s Proxy Statement for its 2025 Annual Meeting are incorporated by reference into Part III of this Report.

TABLE

OF CONTENTS

FORWARD-LOOKING

STATEMENTS

This

annual report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws. These forwarding-looking

statements include without limitation statements regarding our expectations and beliefs about the market and industry, our goals, plans,

and expectations regarding our properties and drilling activities and results, our intentions and strategies regarding future acquisitions

and sales of properties, our intentions and strategies regarding the formation of strategic relationships, our beliefs regarding the

future success of our properties, our expectations and beliefs regarding competition, competitors, the basis of competition and our ability

to compete, our beliefs and expectations regarding our ability to hire and retain personnel, our beliefs regarding period to period results

of operations, our expectations regarding revenues, our expectations regarding future growth and financial performance, our beliefs and

expectations regarding the adequacy of our facilities, and our beliefs and expectations regarding our financial position, ability to

finance operations and growth and the amount of financing necessary to support operations. These statements are subject to risks and

uncertainties that could cause actual results and events to differ materially. See “Item 1A. Risk Factors” for a discussion

of certain risk factors. We undertake no obligation to update forward-looking statements to reflect events or circumstances occurring

after the date of this annual report on Form 10-K.

As

used in this annual report on Form 10-K, unless the context otherwise requires, the terms “we,” “us,” “the

Company,” and “Houston American” refer to Houston American Energy Corp., a Delaware corporation.

PART

I

General

Houston

American Energy Corp is an independent oil and gas company focused on the development, exploration, exploitation, acquisition, and production

of natural gas and crude oil properties. Our principal properties, and operations, are in the U.S. Permian Basin and the South American

country of Colombia. Additionally, we have properties in the Louisiana U.S. Gulf Coast region.

We

focus on early identification of, and opportunistic entrance into, existing and emerging resource plays. We do not operate properties

but typically seek to partner with, or invest along-side, larger operators in the development of resources or retain interests, with

or without contribution on our part, in prospects identified, packaged and promoted to larger operators. By entering these plays earlier,

identifying stranded blocks and partnering with, investing along-side or promoting to, larger operators, we believe we can capture larger

resource potential at lower cost and minimize our exposure to drilling risks and costs and ongoing operating costs.

We,

along with our partners, actively manage our resources through opportunistic acquisitions and divestitures where reserves can be identified,

developed, monetized and financial resources redeployed with the objective of growing reserves, production and shareholder value.

Properties

Our

exploration and development projects are focused on existing property interests in the Texas Permian Basin, the South American country

of Colombia and the onshore Louisiana Gulf Coast region.

Each

of our property interests differ in scope and character and consists of one or more types of assets, such as 3-D seismic data, owned

mineral interests, leasehold positions, lease options, working interests in leases, partnership or limited liability company interests,

corporate equity interests or other mineral rights. Our percentage interest in each property represents the portion of the interest in

the property we share with other partners in the property. Because each property consists of a bundle of assets that may or may not include

a working interest in the project, our stated interest in a property simply represents our proportional ownership in the bundle of assets

that constitute the property. Therefore, our interest in a property should not be confused with the working interest that we will own

when a given well is drilled. Each of our exploration and development projects represents a negotiated transaction between the project

partners relating to one or more properties. Our working interest may be higher or lower than our stated interest.

The

following table sets forth information relating to our principal properties as of December 31, 2024:

| | |

| |

| |

| |

| |

2024 Net Production |

| | |

Net

acreage | |

Average

working

interest % | |

Gross

producing

wells | |

Net proved

reserves

(boe)(1) | |

Oil

(bbls)(1) | |

Natural Gas

(mcf)(1) | |

Natural

Gas Liquids (gallons) |

| Texas | |

| 98 | | |

| 6.8 | % | |

| 4 | | |

| 159,875 | | |

| 5,992 | | |

| 53,476 | | |

| 159,680 | |

| Louisiana | |

| 582 | | |

| 23.4 | % | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | |

| Total U.S. | |

| 680 | | |

| 15.1 | % | |

| 4 | | |

| 159,875 | | |

| 5,992 | | |

| 53,476 | | |

| 159,680 | |

| Colombia(2) | |

| 572 | | |

| 16 | % | |

| 4 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Total | |

| 1,252 | | |

| 16 | % | |

| 8 | | |

| 159,875 | | |

| 5,992 | | |

| 53,476 | | |

| 159,680 | |

| |

(1) |

All reserve and production information excludes wells operated

by Hupecol Meta in Colombia. |

| |

|

|

| |

(2) |

Net acreage and average working interest in Colombia are held

through our investment in Hupecol Meta, and are subject to pending approvals of (i) the proposed relinquishment of a portion of the acreage

within the Venus Exploration Area of the CPO-11 block; and (ii) the acquisition of the remaining 50% interest in the balance of the CPO-11

block previously farmed out to Parex Resources. See “Colombian Properties – CPO-11” below. |

-

United States Properties:

In

the United States, our principal properties and operations are located in the on-shore Permian Basin and Gulf Coast region of Louisiana.

Texas

Properties – Permian Basin

Reeves

County. We hold a 18.1% average working interest in 320 gross acres in Reeves County, Texas, consisting of (1) the 160 gross acre

Johnson Lease, in which we hold a 25% working interest, subject to a proportionate 5% back-in after payout, and (2) the 160 gross acre

O’Brien Lease, in which we hold an average 11.2% working interest. Our Reeves County acreage lies within the Delaware sub-basin

of the Permian Basin, with resource potential in the Wolfcamp, Bone Spring and Avalon formations. During 2017, we drilled and completed

our initial wells on both lease blocks, the Johnson State #1H well and the O’Brien #3H well, both horizontally drilled and hydraulically

fractured wells in the Wolfcamp A formation. The Johnson #1H well and O’Brien #3H well were both placed on gas lift during 2021

and were producing at December 31, 2024. For the year ended December 31, 2024, our production in Reeves County totaled 3,468 barrels

of oil and 53,476 mcf of natural gas.

In

June 2024, we participated in the drilling of six wells in the State Finkle Unit on the O’Brien Lease. All six wells are expected

to commence production in March, 2025

As

of December 31, 2024, no additional development or drilling operations are planned with respect to our Reeves County acreage.

Yoakum

County. We hold a 15.9% average working interest, subject to a proportionate 10% back-in after payout, in an approximately 360 gross

acre block in Yoakum County, Texas. Our Yoakum County acreage lies within the Midland sub-basin of the Permian Basin.

During

2019, we drilled the Frost #1H well, the first well on our Yoakum County acreage. The well was horizontally drilled, hydraulically fractured

in the San Andres Formation and completed and commenced production in mid-2019. A second well on our Yoakum County acreage, the Frost

#2H well, was horizontally drilled, hydraulically fractured in the San Andres Formation and completed and commenced production during

the third quarter of 2020. For the year ended December 31, 2024, our production in Yoakum County totaled 2,524 barrels of oil.

As

of December 31, 2024, no additional development or drilling operations are planned with respect to our Yoakum County acreage.

Louisiana

Properties

Our

sole property in Louisiana consists of a 23.4% mineral interest in 2,485 gross acres in East Baton Rouge Parish.

There

are no present wells, or plans to conduct drilling operations, on our Louisiana acreage.

-

Colombian Properties:

At

December 31, 2024, we held interests in a single block, through our equity investment in Hupecol Meta, LLC, operated by Hupecol Operating

and affiliates, in Colombia covering 639,405 gross acres. We identify our Colombian prospect as the Venus Exploration Area within the

CPO-11 block and remainder of the CPO-11 block.

The

following table sets forth information relating to our interests in prospects in Colombia at December 31, 2024:

Property

| |

Operator

| | |

Ownership

Interest

| | |

Total

Gross Acres

| | |

Total

Gross Developed Acres

| | |

Gross

Productive Wells

| |

| CPO-11 – Venus Exploration Area | |

Hupecol | | |

| 16.0 | % | |

| 3,573 | | |

| 1,332 | | |

| 4 | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

| Total | |

| | |

| | | |

| 3,573 | | |

| 1,332 | | |

| 4 | |

The

CPO-11 concession, including the Venus Exploration Area, is located in the Llanos Basin and is owned and operated by Hupecol Meta.

CPO-11

During

2019, we acquired a two percent ownership interest in Hupecol Meta, LLC (“Hupecol Meta”). Hupecol Meta owns the 639,405 gross

acre CPO-11 block in the Llanos Basin in Colombia. The CPO-11 block is comprised of the 69,128 acre Venus Exploration area and 570,277

acres which was 50% farmed out by Hupecol to Parex Resources. In 2021, Hupecol Meta increased its ownership interest in the CPO-11 block

and we agreed to contribute $99,716. In 2022, we acquired additional interests in Hupecol Meta for an aggregate of $657,638. As a result

of our acquisition of additional interests in 2021 and 2022, our ownership interest in Hupecol Meta was approximately 18% at December

31, 2024. Through our ownership interest in Hupecol Meta, at December 31, 2024, we hold an approximately 16% interest in the Venus Exploration

Area and an approximately 8% interest in the remainder of the CPO-11 block.

The

CPO-11 block covers almost 1,000 square miles. During 2023, in the Venus Exploration Area, Hupecol Meta drilled and completed the Venus

1-H horizontal well and the Venus 2-H ST1 well. At December 31, 2024, the Saturno ST1 and Venus 2A wells, both vertical wells, and the

Venus 1-H and Venus 2-H ST1 wells, both horizontal wells, were on production in the Venus Exploration Area of the CPO-11 block.

Hupecol

Meta has (i) proposed to relinquish approximately 62,139 gross acres within the Venus Exploration Area, decreasing its holding within

that area to approximately 7,157 gross, and 1,145 net, acres; and (ii) agreed to acquire the 50% interest in the CPO-11 block farmed

out to Parex Resources, which would increase Hupecol Meta’s net acreage position in the block to 91,244 acres. The relinquishment

of such acreage and acquisition of the Parex interest are both subject to approval of the Colombian hydrocarbons agency, or ANH.

Our

equity investment in Hupecol Meta is accounted for at cost and, accordingly, this report does not include any reserves, production and

operating results of Hupecol Meta.

In

late 2023, Hupecol advised that it intends to evaluate potential monetization of its assets in Colombia, including the interest in the

CPO-11 block held by Hupecol Meta. Pending the outcome of Hupecol’s evaluation of, and potential efforts regarding, monetization

of the CPO-11 block, we have no planned drilling operations, or other planned operations, in Colombia. There is no assurance as to the

timing or outcome of Hupecol’s potential monetization of assets.

As

of December 31, 2024, the Company determined it was necessary to take an impairment charge for our investment in Hupecol Meta due to indications

that its earnings performance has deteriorated, and the investment is no longer viewed as viable. We determined that we are unlikely to

receive any substantial amount of proceeds upon the sale of Hupecol Meta, rendering the value of the investment fully impaired.

Drilling

Activity

The

following table summarizes the number of wells drilled through Hupecol Meta, during 2024, 2023 and 2022, excluding any wells drilled

under farmout agreements, royalty interest ownership, or any other wells in which we do not have a working interest (direct or indirect).

| | |

Year Ended December 31, | |

| | |

2024 | | |

2023 | | |

2022 | |

| | |

Gross

| | |

Net

| | |

Gross

| | |

Net

| | |

Gross

| | |

Net

| |

| Development wells, completed as: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Productive | |

| — | | |

| — | | |

| 2 | | |

| 0.32 | | |

| — | | |

| — | |

| Non-productive | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | |

| Total development wells | |

| — | | |

| — | | |

| 2 | | |

| 0.32 | | |

| — | | |

| — | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Exploratory wells, completed as: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Productive | |

| — | | |

| — | | |

| — | | |

| — | | |

| 1 | | |

| 0.16 | |

| Non-productive | |

| 1 | | |

| 0.16 | | |

| — | | |

| — | | |

| 1 | | |

| 0.16 | |

| Total exploratory wells | |

| — | | |

| — | | |

| | | |

| | | |

| 2 | | |

| 0.32 | |

Productive

wells are wells that are found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of the

production exceed production expenses and taxes. During 2024, the operator of the O’Brien Lease, EOG, decided to drill six new

wells on the Finkle State Unit. We decided to participate in the drilling of those wells. We anticipate production from those wells to

begin in March, 2025. .

Hupecol

Meta drilled a well in 2024 which turned out to be non-productive. Through our investment in Hupecol Meta, we own approximately 16%

of the block on which the well was drilled.

Productive

Wells

Productive

wells consist of producing wells and wells capable of production, including shut-in wells. A well bore with multiple completions is counted

as only one well. As of December 31, 2024, we owned interests in 14 gross wells (including indirect interests in wells in Colombia through

our equity interest in Hupecol Meta). As of December 31, 2024, we had interests in productive wells, categorized by geographic area,

as follows:

| | |

Oil Wells | | |

Gas Wells | |

| United States | |

| | | |

| | |

| Gross | |

| 10 | | |

| — | |

| Net | |

| 0.7022 | | |

| — | |

| Colombia | |

| | | |

| | |

| Gross | |

| 4 | | |

| — | |

| Net | |

| 0.64 | | |

| — | |

| Total | |

| | | |

| | |

| Gross | |

| 14 | | |

| — | |

| Net | |

| 1.3422 | | |

| — | |

Volume,

Prices and Production Costs

The

following table sets forth certain information regarding the production volumes, average prices received and average production costs

associated with our sales of gas and oil, categorized by geographic area (excluding our production, prices and costs attributable to

wells operated by Hupecol Meta), for each of the three years ended December 31, 2024, 2023, and 2022:

| | |

Year Ended December 31, | |

| | |

2024 | | |

2023 | | |

2022 | |

| Net Production: | |

| | | |

| | | |

| | |

| Gas (Mcf): | |

| | | |

| | | |

| | |

| United States | |

| 53,476 | | |

| 57,360 | | |

| 73,635 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| Total | |

| 53,476 | | |

| 57,360 | | |

| 73,635 | |

| | |

| | | |

| | | |

| | |

| Natural Gas Liquids (Gallons) | |

| | | |

| | | |

| | |

| United States | |

| 159,680 | | |

| 179,506 | | |

| 248,506 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| Total | |

| 159,680 | | |

| 179,506 | | |

| 248,506 | |

| | |

| | | |

| | | |

| | |

| Oil (Bbls): | |

| | | |

| | | |

| | |

| United States | |

| 5,992 | | |

| 7,971 | | |

| 10,688 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| Total | |

| 5,992 | | |

| 7,971 | | |

| 10,688 | |

| | |

| | | |

| | | |

| | |

| Average sales price: | |

| | | |

| | | |

| | |

| Gas ($ per Mcf) | |

| | | |

| | | |

| | |

| United States | |

$ | 0.17 | | |

$ | 1.38 | | |

$ | 5.13 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| Total | |

$ | 0.17 | | |

$ | 1.38 | | |

$ | 5.13 | |

| | |

| | | |

| | | |

| | |

| Natural Gas Liquids ($ per Gallon) | |

| | | |

| | | |

| | |

| United States | |

$ | 0.71 | | |

$ | 0.69 | | |

$ | 1.07 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| Total | |

$ | 0.71 | | |

$ | 0.69 | | |

$ | 1.07 | |

| | |

| | | |

| | | |

| | |

| Oil ($ per Bbl) | |

| | | |

| | | |

| | |

| United States | |

| 73.08 | | |

$ | 74.08 | | |

$ | 93.10 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| | |

| | | |

| | | |

| | |

| Total | |

| 73.08 | | |

$ | 74.08 | | |

$ | 93.10 | |

| | |

| | | |

| | | |

| | |

| Average production costs ($ per BOE): | |

| | | |

| | | |

| | |

| United States | |

| 42.85 | | |

$ | 27.03 | | |

$ | 27.48 | |

| Colombia | |

| — | | |

| — | | |

| — | |

| | |

| | | |

| | | |

| | |

| Total | |

| 42.85 | | |

$ | 27.03 | | |

$ | 27.48 | |

Average production costs per BOE in 2024 increased to $42.85 per BOE from

$27.03 in 2023 due to inflation-related increases in expenses and workover costs incurred in early 2024 related to two of our US wells.

Natural

Gas and Oil Reserves

Reserve

Estimates

The

following tables set forth, by country and as of December 31, 2024, our estimated net proved oil and natural gas reserves, and the estimated

present value (discounted at an annual rate of 10%) of estimated future net revenues before future income taxes (“PV-10”)

and after future income taxes (“Standardized Measure”) of our proved reserves, each prepared in accordance with assumptions

prescribed by the Securities and Exchange Commission (“SEC”). The below table excludes reserve and other information pertaining

to assets operated by Hupecol Meta.

The

PV-10 value is a widely used measure of value of oil and natural gas assets and represents a pre-tax present value of estimated cash

flows discounted at ten percent. PV-10 is considered a non-GAAP financial measure as defined by the SEC. We believe that our PV-10 presentation

is relevant and useful to our investors because it presents the discounted future net cash flows attributable to our proved reserves

before taking into account the related future income taxes, as such taxes may differ among various companies because of differences in

the amounts and timing of deductible basis, net operating loss carry forwards and other factors. We believe investors and creditors use

our PV-10 as a basis for comparison of the relative size and value of our proved reserves to the reserve estimates of other companies.

PV-10 is not a measure of financial or operating performance under GAAP and is not intended to represent the current market value of

our estimated oil and natural gas reserves. PV-10 should not be considered in isolation or as a substitute for the standardized measure

of discounted future net cash flows as defined under GAAP.

These

calculations were prepared using standard geological and engineering methods generally accepted by the petroleum industry and in accordance

with SEC financial accounting and reporting standards.

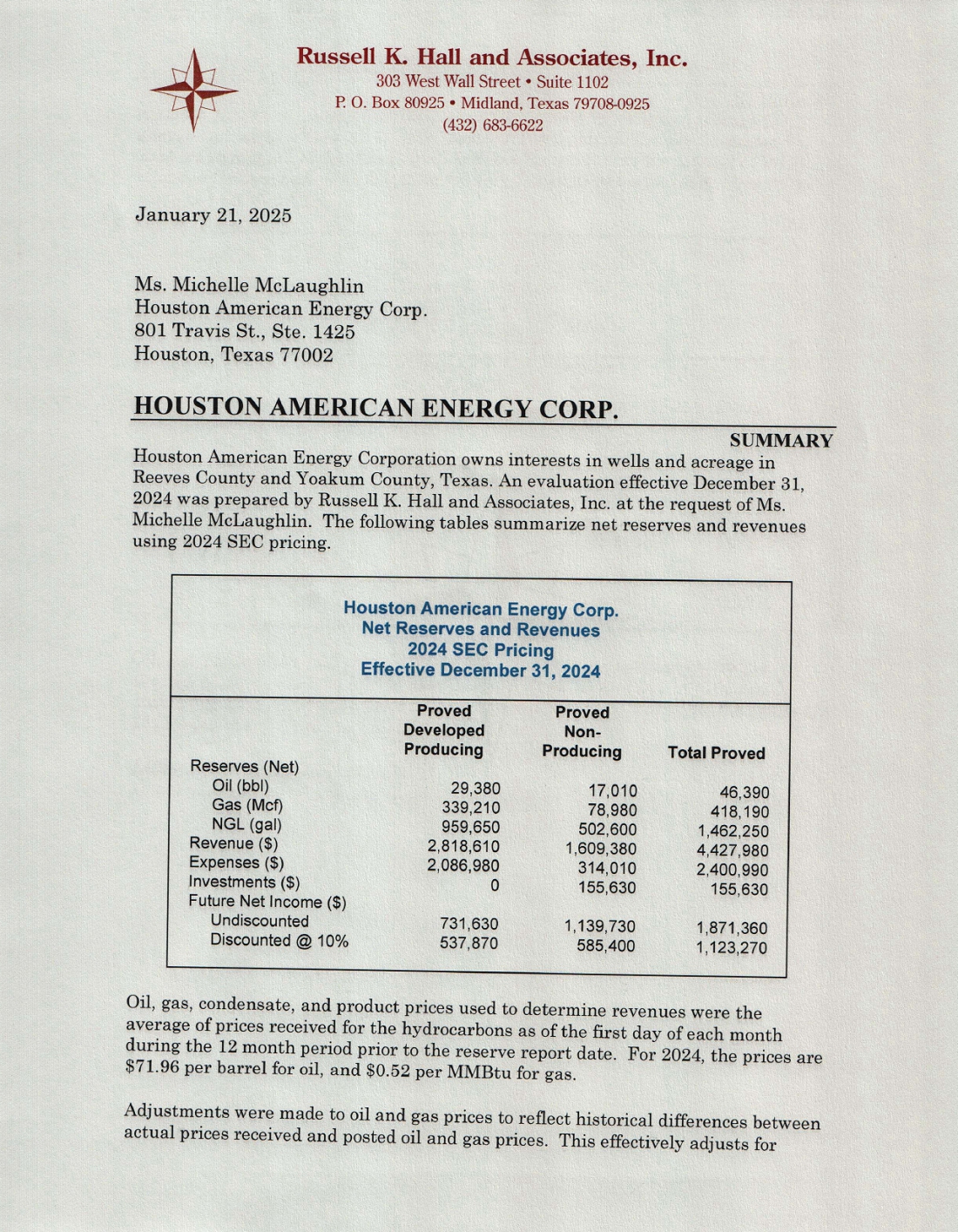

| | |

| | |

Reserves (1) | |

| | |

Oil | | |

Natural Gas | | |

Natural Gas Liquids | | |

Total (2) | |

| | |

(bbls) | | |

(mcf) | | |

(gal) | | |

(boe) | |

| Reserve category | |

| | | |

| | | |

| | | |

| | |

| Proved Developed Producing | |

| | | |

| | | |

| | | |

| | |

| United States | |

| 29,380 | | |

| 339,210 | | |

| 959,650 | | |

| 108,764 | |

| Colombia(3) | |

| — | | |

| — | | |

| — | | |

| — | |

| Total Proved Developed Producing Reserves | |

| 29,380 | | |

| 339,210 | | |

| 959,650 | | |

| 108,764 | |

| Proved Non-Producing | |

| | | |

| | | |

| | | |

| | |

| United States | |

| 17,010 | | |

| 78,980 | | |

| 502,600 | | |

| 42,140 | |

| Colombia(3) | |

| — | | |

| — | | |

| — | | |

| — | |

| Total Proved Non-Producing Reserves | |

| 17,010 | | |

| 78,980 | | |

| 502,600 | | |

| 42,140 | |

| Total Proved Reserves | |

| 46,390 | | |

| 418,190 | | |

| 1,462,250 | | |

| 150,904 | |

| | |

Proved Developed | | |

Proved Non-Producing | | |

Total Proved | |

| PV-10 (1) | |

$ | 537,870 | | |

$ | 585,400 | | |

$ | 1,123,270 | |

| Standardized measure (4) | |

$ | 537,870 | | |

$ | 585,400 | | |

$ | 1,123,270 | |

| |

(1) |

In accordance with

applicable financial accounting and reporting standards of the SEC, the estimates of our proved reserves and the PV-10 set forth

herein reflect estimated future gross revenue to be generated from the production of proved reserves, net of estimated production

and future development costs, using prices and costs under existing economic conditions at December 31, 2024. For purposes of

determining prices, we used the unweighted arithmetical average of the prices on the first day of each month within the 12-month

period ended December 31, 2024. The average prices utilized for purposes of estimating our proved reserves were $71.96 per barrel of

oil, $0.52 per MMBTu of natural gas, and $0.71 per gallon of natural gas liquids for our US properties, adjusted by property for

energy content, quality, transportation fees and regional price differentials. The prices should not be interpreted as a prediction

of future prices. The amounts shown do not give effect to non-property related expenses, such as corporate general administrative

expenses and debt service, future income taxes or to depreciation, depletion and amortization. |

| |

|

|

| |

(2) |

Natural gas is converted on the basis of six Mcf of gas per

one barrel of oil equivalent. |

| |

|

|

| |

(3) |

As an equity investment accounted for at cost, we do not report

any reserves attributable to our investment in Hupecol Meta. |

| |

|

|

| |

(4) |

The Standard Measure differs from PV-10 only in that the Standard

Measure reflects estimated future income taxes. |

Due

to the inherent uncertainties and the limited nature of reservoir data, proved reserves are subject to change as additional information

becomes available. The estimates of reserves, future cash flows and present value are based on various assumptions, including those prescribed

by the SEC, and are inherently imprecise. Although we believe these estimates are reasonable, actual future production, cash flows, taxes,

development expenditures, operating expenses and quantities of recoverable oil and natural gas reserves may vary substantially from these

estimates.

Reserve

Estimation Process, Controls and Technologies

The

reserve estimates, including PV-10 and Standard Measure estimates, set forth above were prepared by Russell K. Hall & Associates,

Inc. for our Permian Basin, Texas reserves.

The reserves as of December 31, 2024 were determined in accordance with

standard industry practices and SEC regulations by the licensed independent petroleum engineering firm. The calculations were prepared

using standard geological and engineering methods generally accepted by the petroleum industry.

Our

year-end reserve reports are prepared by reserve engineering firms based upon a review of property interests being appraised, production

from such properties, current costs of operation and development, current prices for production, agreements relating to current and future

operations and sale of production, geosciences and engineering data, and other information provided to them by our management team. Upon

analysis and evaluation of data provided, the reserve engineering firms issue a preliminary appraisal report of our reserves. The preliminary

appraisal report and changes in our reserves are reviewed by our President and board for reasonableness of the results obtained. Once

any questions have been addressed, the reserve engineering firms issue final appraisal reports, reflecting their conclusions.

Russell

K. Hall & Associates is an independent Midland, Texas based professional engineering firm providing reserve evaluation services to

the oil and gas industry. Their report was prepared under the direction of Russell K. Hall, founder and President of Russell K. Hall

& Associates. Mr. Hall holds a BS in Mechanical Engineering from the University of Oklahoma, is a registered professional engineer

and a member of the Society of Petroleum Engineers, the Society of Independent Professional Earth Scientists and the West Texas Geological

Society. Mr. Hall has more than 30 years of experience in reserve evaluation for the oil and gas industry and the oil and gas finance

industry. Russell K. Hall & Associates, and its employees, have no interest in our company or our properties and were objective in

determining our reserves.

The

SEC’s rules with respect to technologies that a company can use to establish reserves allows use of techniques that have been proved

effective by actual production from projects in the same reservoir or an analogous reservoir or by other evidence using reliable technology

that establishes reasonable certainty. Reliable technology is a grouping of one or more technologies (including computational methods)

that have been field tested and have been demonstrated to provide reasonably certain results with consistency and repeatability in the

formation being evaluated or in an analogous formation.

Our

reserve engineering firm used a combination of production and pressure performance, simulation studies, offset analogies, seismic data

and interpretation, geophysical logs and core data to calculate our reserves estimates.

Proved

Undeveloped Reserves

We

had no proved undeveloped reserves at either December 31, 2023 or December 31, 2024.

Developed

and Non-Producing Acreage

The

following table sets forth the gross and net developed and non-producing acreage (including both leases and concessions, but

excluding acreage in which we hold a royalty interest but no working interest), categorized by geographical area, which we held as of

December 31, 2024:

| | |

Developed | | |

Non-Producing | |

| | |

Gross

| | |

Net

| | |

Gross

| | |

Net

| |

| United States | |

| 3,040 | | |

| 98 | | |

| 2,485 | | |

| 582 | |

| Colombia | |

| 1,332 | | |

| 213 | | |

| 2,241 | | |

| 359 | |

| Total | |

| 4,372 | | |

| 311 | | |

| 4,726 | | |

| 941 | |

Developed

acreage is comprised of leased acres that are within an area spaced by or assignable to a productive well and acreage in which we hold

a direct or indirect mineral interest with no potential development related lease expirations. Non-producing acreage is comprised

of leased acres that are within an areas assigned to a well which is not yet producing, in which we hold a direct or indirect mineral

interest.

As

is customary in the oil and natural gas industry, we can generally retain our interest in undeveloped acreage by drilling activity that

establishes commercial production sufficient to maintain the leases or by paying delay rentals during the remaining primary term of leases.

The oil and natural gas leases in which we have an interest are for varying primary terms and, if production under a lease continues

from our developed lease acreage beyond the primary term, we are entitled to hold the lease for as long as oil or natural gas is produced.

Title

to Properties

Title

to properties is subject to royalty, overriding royalty, carried working, net profits, working and other similar interests and contractual

arrangements customary in the gas and oil industry, liens for current taxes not yet due and other encumbrances. As is customary in the

industry in the case of undeveloped properties, little investigation of record title is made at the time of acquisition (other than preliminary

review of local records).

Investigation,

including a title opinion of local counsel, generally is made before commencement of drilling operations.

Marketing

At

December 31, 2024, we had no contractual agreements to sell our gas and oil production and all production was sold on spot markets.

Human

Capital

As

of December 31, 2024, we had 2 full-time employees and no part-time employees. The employees are not covered by a collective bargaining

agreement, and we do not anticipate that any of our future employees will be covered by such agreements.

Competition

We

encounter intense competition from other oil and gas companies in all areas of our operations, including the acquisition of producing

properties and undeveloped acreage. Our competitors include major integrated oil and gas companies, numerous independent oil and gas

companies and individuals. Many of our competitors are large, well-established companies with substantially larger operating staffs and

greater capital resources and have been engaged in the oil and gas business for a much longer time than our Company. These companies

may be able to pay more for productive oil and gas properties, exploratory prospects and to define, evaluate, bid for and purchase a

greater number of properties and prospects than our financial or human resources permit. Our ability to acquire additional properties

and to discover reserves in the future will be dependent upon our ability to evaluate and select suitable properties and to consummate

transactions in this highly competitive environment.

Regulatory

Matters

Regulation

of Oil and Gas Production, Sales and Transportation

The

oil and gas industry is subject to regulation by numerous national, state and local governmental agencies and departments. Compliance

with these regulations is often difficult and costly and noncompliance could result in substantial penalties and risks. Most jurisdictions

in which we operate also have statutes, rules, regulations or guidelines governing the conservation of natural resources, including the

unitization or pooling of oil and gas properties, minimum well spacing, plugging and abandonment of wells and the establishment of maximum

rates of production from oil and gas wells. Some jurisdictions also require the filing of drilling and operating permits, bonds and reports.

The failure to comply with these statutes, rules and regulations could result in the imposition of fines and penalties and the suspension

or cessation of operations in affected areas.

Environmental

Regulation

Various

federal, state and local laws and regulations relating to the protection of the environment, including the discharge of materials into

the environment, may affect our exploration, development and production operations and the costs of those operations. These laws and

regulations, among other things, govern the amounts and types of substances that may be released into the environment, the issuance of

permits to conduct exploration, drilling and production operations, the discharge and disposition of generated waste materials and waste

management, the reclamation and abandonment of wells, sites and facilities, financial assurance and the remediation of contaminated sites.

These laws and regulations may impose substantial liabilities for noncompliance and for any contamination resulting from our operations

and may require the suspension or cessation of operations in affected areas.

The

environmental laws and regulations applicable to our U.S. operations include, among others, the following United States federal laws

and regulations:

| |

● |

Clean Air Act, and its amendments, which govern air emissions; |

| |

|

|

| |

● |

Clean Water Act, which governs discharges into waters of the

United States; |

| |

|

|

| |

● |

Comprehensive Environmental Response, Compensation and Liability

Act, which imposes liability where hazardous releases have occurred or are threatened to occur (commonly known as “Superfund”); |

| |

|

|

| |

● |

Resource Conservation and Recovery Act, which governs the management

of solid waste; |

| |

|

|

| |

● |

Oil Pollution Act of 1990, which imposes liabilities resulting

from discharges of oil into navigable waters of the United States; |

| |

|

|

| |

● |

Emergency Planning and Community Right-to-Know Act, which requires

reporting of toxic chemical inventories; |

| |

|

|

| |

● |

Safe Drinking Water Act, which governs the underground injection

and disposal of wastewater; and |

| |

|

|

| |

● |

U.S. Department of Interior regulations, which impose liability

for pollution cleanup and damages. |

Colombia

has similar laws and regulations designed to protect the environment.

We

routinely obtain permits for our facilities and operations in accordance with these applicable laws and regulations on an ongoing basis.

There are no known issues that have a significant adverse effect on the permitting process or permit compliance status of any of our

facilities or operations.

The

ultimate financial impact of these environmental laws and regulations is neither clearly known nor easily determined as new standards

are enacted and new interpretations of existing standards are rendered. Environmental laws and regulations are expected to have an increasing

impact on our operations. In addition, any non-compliance with such laws could subject us to material administrative, civil or criminal

penalties, or other liabilities. Potential permitting costs are variable and directly associated with the type of facility and its geographic

location. Costs, for example, may be incurred for air emission permits, spill contingency requirements, and discharge or injection permits.

These costs are considered a normal, recurring cost of our ongoing operations and not an extraordinary cost of compliance with government

regulations.

Although

we do not operate the properties in which we hold interests, noncompliance with applicable environmental laws and regulations by the

operators of our oil and gas properties could expose us, and our properties, to potential costs and liabilities associated with such

environmental laws. While we exercise no oversight with respect to any of our operators, we believe that each of our operators is committed

to environmental protection and compliance. However, since environmental costs and liabilities are inherent in our operations and in

the operations of companies engaged in similar businesses and since regulatory requirements frequently change and may become more stringent,

there can be no assurance that material costs and liabilities will not be incurred in the future. Such costs may result in increased

costs of operations and acquisitions and decreased production.

Hydraulic

Fracturing Regulation

Hydraulic

fracturing, or “fracking”, is a common practice used to stimulate production of oil and natural gas from tight formations,

including shales. Fracking involves the injection of fluids—usually consisting mostly of water but typically including small amounts

of chemical additives—as well as sand into a well under high pressure in order to create fractures in the rock that allow oil or

gas to flow more freely to the wellbore.

Except

as applies to federal lands, fracking generally is exempt from regulation under many federal environmental rules and is generally regulated

at the state level.

For

example, in Texas, the Texas Railroad Commission administers regulations related to oil and gas operations, including regulations pertaining

to protection of water resources in connection with those operations. The Texas Legislature adopted new legislation requiring oil and

gas operators to publicly disclose the chemicals used in the hydraulic fracturing process, effective as of September 1, 2011. The Texas

Railroad Commission has adopted rules and regulations implementing this legislation that apply to all wells for which the Railroad Commission

issues an initial drilling permit after February 1, 2012. This law requires that the well operator disclose the list of chemical ingredients

subject to the requirements of the federal Occupational Safety and Health Act (“OSHA”) for disclosure on an internet website

and also file the list of chemicals with the Texas Railroad Commission with the well completion report. The total volume of water used

to hydraulically fracture a well must also be disclosed to the public and filed with the Texas Railroad Commission.

There

is public controversy regarding fracking with regard to the use of fracking fluids, impacts on drinking water supplies, use of water

and the potential for impacts to surface water, groundwater and the environment generally. Lawsuits and enforcement actions have been

initiated across the country implicating hydraulic fracturing practices. If new laws or regulations restricting hydraulic fracturing

are adopted, such laws could make it more difficult or costly to perform fracturing to stimulate production from tight formations as

well as make it easier to initiate legal proceedings based on allegations that specific chemicals used in the fracturing process could

adversely affect groundwater. In addition, if hydraulic fracturing is further regulated at the federal or state level, fracturing activities

could become subject to additional permitting and financial assurance requirements, more stringent construction specifications, increased

monitoring, reporting and recordkeeping obligations, plugging and abandonment requirements and also to attendant permitting delays and

potential increases in costs. Such legislative changes could cause operators to incur substantial compliance costs, and compliance or

the consequences of any failure to comply could have a material adverse effect on well operations and economics.

We

do not operate wells but contract well operations to third party operators. Operators of our wells may perform fracking operations, or

contract third parties to perform such operations, on wells in which we participate. Many newer wells would not be economical without

the use of fracking to stimulate production from the well. At this time, it is not possible to estimate the impact on our business of

newly enacted or potential federal or state legislation governing hydraulic fracturing.

Climate

Change Legislation and Greenhouse Gas Regulation

Federal,

state and local laws and regulations are increasingly being enacted to address concerns about the effects the emission of “greenhouse

gases” may have on the environment and climate. These effects are widely referred to as “climate change.” Since its

December 2009 endangerment finding regarding the emission of greenhouse gases, the Environmental Protection Agency (the “EPA”)

has begun regulating sources of greenhouse gas emissions under the federal Clean Air Act. Among several regulations requiring reporting

or permitting for greenhouse gas sources, the EPA finalized its “tailoring rule” in May 2010 that determines which stationary

sources of greenhouse gases are required to obtain permits to construct, modify or operate on account of, and to implement the best available

control technology for, their greenhouse gases. The EPA’s final greenhouse gas reporting requirements pertain to certain oil and

gas production facilities.

Moreover,

the U.S. Congress has considered establishing a cap-and-trade program to reduce U.S. emissions of greenhouse gases. Under past proposals,

the EPA would issue or sell a capped and steadily declining number of tradable emissions allowances to certain major sources of greenhouse

gas emissions so that such sources could continue to emit greenhouse gases into the atmosphere. These allowances would be expected to

escalate significantly in cost over time. The net effect of such legislation, if ever adopted, would be to impose increasing costs on

the combustion of carbon-based fuels such as crude oil, refined petroleum products, and natural gas. In addition, while the prospect

for such cap-and-trade legislation by the U.S. Congress remains uncertain, several states have adopted, or are in the process of adopting,

similar cap-and-trade programs.

As

a crude oil and natural gas company, the debate on climate change is relevant to our operations because the regulatory response is designed

to reduce demand for, and use of, our products, oil and gas, in favor of alternative forms of energy. We cannot presently predict the

ultimate impact of existing or future climate change initiatives on our company or our industry although we do anticipate that, at a

minimum, we will incur additional operating and other costs to respond to such initiatives.

Web

Site Access to Reports

Our

Web site address is www.houstonamerican.com. We make available, free of charge on our Web site, our annual report on Form 10-K,

quarterly reports on Form 10-Q and current reports on Form 8-K, and all amendments to these reports as soon as reasonably practicable

after such material is electronically filed with, or furnished to, the United States Securities and Exchange Commission. Information

contained on our website is not incorporated by reference into this report and you should not consider information contained on our website

as part of this report.

Our

business activities and the value of our securities are subject to significant hazards and risks, including those described below. If

any of such events should occur, our business, financial condition, liquidity and/or results of operations could be materially harmed,

and holders and purchasers of our securities could lose part or all of their investments.

Company

and Organization Risks

We

have experienced recurring operating losses and may not attain profitability; attainment of profitability will require successful drilling

and development operations to support substantial increases in production and revenues.

We

have incurred losses from operations in each year since 2011 and, at December 31, 2024, had an accumulated deficit of $85,215,109. While

we have implemented cost control initiatives that have brought down our overhead in recent years and distributions of our share of profits

from Hupecol Meta have improved overall profitability, our ability to attain profitability is substantially dependent upon our other

oil and gas assets. In order to increase production and revenues, we will need to successfully drill new wells on our existing acreage

at a pace, and with results, significantly greater than in recent years. If, for any reason, we are unable to substantially increase

our production and revenues and sustain or grow our profitability, while controlling drilling costs and overhead, we may never attain,

or sustain, profitability. Our ability to so increase production and revenues and attain profitability is subject to all of the other

risks of oil and gas operations as well as our ability to fund our share of drilling and development operations.

Our

ability to operate profitably and our financial condition are highly dependent on energy prices. A substantial or extended decline in

oil and natural gas prices may adversely affect our business, financial condition or results of operations and our ability to meet our

capital expenditure obligations and financial commitments.

The

price we receive for our oil and natural gas production heavily influences our revenue, profitability, access to capital and future rate

of growth. Oil and natural gas are commodities and, therefore, their prices are subject to wide fluctuations in response to relatively

minor changes in supply and demand. Historically, the markets for oil and natural gas have been volatile. These markets will likely continue

to be volatile in the future. The prices we receive for our production depend on numerous factors beyond our control. These factors include,

but are not limited to, the following:

| |

● |

changes

in global supply and demand for oil and natural gas, including changes in demand resulting from general and specific economic conditions

relating to the business cycle and other factors (e.g., global health pandemics such as COVID-19); |

| |

|

|

| |

● |

the

actions of the Organization of Petroleum Exporting Countries, or OPEC; |

| |

|

|

| |

● |

the

price and quantity of imports of foreign oil and natural gas; |

| |

|

|

| |

● |

political

conditions, including embargoes, in or affecting other oil-producing activity; |

| |

|

|

| |

● |

the

level of global oil and natural gas exploration and production activity; |

| |

|

|

| |

● |

the

level of global oil and natural gas inventories; |

| |

|

|

| |

● |

weather

conditions; |

| |

|

|

| |

● |

technological

advances affecting energy consumption, including renewable energy initiatives that result in energy consumption transitioning away

from fossil fuels; and |

| |

|

|

| |

● |

the

price and availability of alternative fuels. |

Global

economic growth drives demand for energy from all sources, including fossil fuels. Should the U.S. and global economies experience weakness,

demand for energy may decline. Similarly, should growth in global energy production outstrip demand, excess supplies may arise. Declines

in demand and excess supplies may result in accompanying declines in commodity prices and deterioration of our financial position along

with our ability to operate profitably and our ability to obtain financing to support operations.

With

respect to our business, we have experienced periodic declines in demand thought to be associated with slowing economic growth in certain

markets, including the effects of the COVID-19 pandemic, coupled with new oil and gas supplies coming on line and other circumstances

beyond our control that resulted in oil and gas supply exceeding global demand which, in turn, resulted in steep declines in prices of

oil and natural gas.

Past

declines in prices reduced, and any declines that may occur in the future can be expected to reduce, our revenues and profitability as

well as the value of our reserves. Such declines adversely affect well and reserve economics and may reduce the amount of oil and natural

gas that we can produce economically, resulting in deferral or cancellation of planned drilling and related activities until such time,

if ever, as economic conditions improve sufficiently to support such operations. Any extended decline in oil or natural gas prices may

materially and adversely affect our future business, financial condition, results of operations, liquidity or ability to finance planned

capital expenditures.

Supply

chain challenges, such as those arising in the wake of the COVID-19 pandemic, may adversely affect our operations.

Supply

and demand imbalances, such as those arising from the COVID-19 pandemic, have resulted, and may result, in shortages, backlogs and delayed

deliveries of a wide array of products and services, including products and services critical to oil and gas operations. Any future outbreaks

of infectious disease, or other development, may result in supply chain challenges, in which case we may experience unavailability, or

delay in delivery, of products and services that are critical to our well operations. Any such delays may result in deferral or reduction

of revenues and increased costs, any of which could materially adversely affect our profitability.

Competition

in the oil and natural gas industry is intense, which may adversely affect our ability to compete.

We

operate in a highly competitive environment for acquiring properties, marketing oil and natural gas and securing trained personnel. Many

of our competitors possess and employ financial, technical and personnel resources substantially greater than ours, which can be particularly

important in the areas in which we operate. Those companies may be able to pay more for productive oil and natural gas properties and

exploratory prospects and to evaluate, bid for and purchase a greater number of properties and prospects than our financial or personnel

resources permit. Our ability to acquire additional prospects and to find and develop reserves in the future will depend on our ability

to evaluate and select suitable properties and to consummate transactions in a highly competitive environment. Also, there is substantial

competition for capital available for investment in the oil and natural gas industry. We may not be able to compete successfully in the

future in acquiring prospective reserves, developing reserves, marketing hydrocarbons, attracting and retaining quality personnel and

raising additional capital.

Our

ability to acquire additional mineral acreage and to drill and develop our existing acreage as well as other acreage that may be acquired

is subject to availability of financing on satisfactory terms.

Our

financial resources are limited and may not be adequate to fully drill and develop our acreage or to consummate any meaningful

acquisition. Our available funds as of February 2025 are expected to be adequate to fund our share of current existing well

expenses. However, our funds on hand are not expected to be adequate to support a long-term drilling and development plan with

respect to our existing acreage holdings, should such a plan be implemented.

We

may continue to seek to access the capital markets to support planned drilling operations or acquisitions through sales of equity securities

or may seek debt financing to support such capital requirements. We do not presently have any commitments to provide equity or debt financing

to support any future drilling operations or acquisitions and there can be no assurance that such financing will be available if and

when needed on acceptable terms or at all. If we are unable to fund our share of drilling and completion costs of future wells, we may

experience flat and declining production and revenues and decreased profitability and may be subject to penalties with respect to our

interest in acreage.

Our

ability to utilize our common stock to finance future capital needs, or for other purposes, is limited by our authorized shares available

for issuance.

As

of February 2025, we had authority to issue a total of 20 million shares of common stock, of which approximately 16 million shares had

been issued and 1 million shares were reserved for issuance pursuant to outstanding stock options and warrants.

We

have historically utilized “at-the-market” sales of our common stock to provide financing to support growth and operations.

With the limited shares of common stock presently available for issuance, our ability to secure additional funding through the sale of

common stock is limited. Absent an increase in the shares of common stock authorized to be issued, we will be limited to other financing

structures in the event additional financing is required. Such alternative structures may be less favorable or unavailable in which case

we may be forced to forego opportunities or required to downsize operations due to lack of funding.

We

may be unable to make attractive acquisitions and any acquisitions may be subject to substantial risks that could adversely affects our

business.

Acquisitions

of additional mineral acreage at favorable prices is part of our strategy to increase and diversify our holdings and grow our production

and revenues. We expect to focus our acquisition efforts in the Permian Basin with an emphasis on partnering with proven

operators in the area to acquire positions at favorable prices. Competition for mineral acreage in the Permian Basin is intense. Other

operators, particularly large operators, have historically paid substantially higher prices for Permian Basin acreage than we have paid.

There can be no assurance that we will be able to successfully acquire additional acreage in the Permian Basin, or elsewhere

at favorable prices or at all. Even if we are successful in acquiring additional acreage on favorable terms, it is possible that such

acreage (i) will be more speculative than higher priced acreage, (ii) may face challenges or limitations in drilling and operations such

as lack of, or limited access to, critical infrastructure, or (iii) may prove uneconomical.

Our

success depends on our staff, which is small in size and limited in technical capabilities, and third party consultants, the loss of

any of whom could disrupt our business operations.

Our

success will depend on our ability to attract and retain key staff members. Our staff is extremely small in size and possesses limited

technical capabilities. We do not presently maintain any significant internal technical capabilities but rely on the engineering, geological

and other technical skills of our board and third party consultants. If members of our staff should resign or we

are unable to attract the necessary personnel, our business operations could be adversely affected.

Our

charter and bylaws, as well as provisions of Delaware law, could make it difficult for a third party to acquire our company and also

could limit the price that investors are willing to pay in the future for shares of our common stock.

Delaware

corporate law and our charter and bylaws contain provisions that could delay, deter or prevent a change in control of our Company or

our management. These provisions could also discourage proxy contests and make it more difficult for our stockholders to elect directors

and take other corporate actions without the concurrence of our management or board of directors. These provisions:

| |

● |

authorize

our board of directors to issue “blank check” preferred stock, which is preferred stock that can be created and issued

by our board of directors, without stockholder approval, with rights senior to those of our common stock; |

| |

|

|

| |

● |

provide

for a staggered board of directors and three-year terms for directors, so that no more than one-third of our directors could be replaced

at any annual meeting; |

| |

|

|

| |

● |

provide

that directors may be removed only for cause; and |

| |

|

|

| |

● |

establish

advance notice requirements for submitting nominations for election to the board of directors and for proposing matters that can

be acted upon by stockholders at a meeting. |

We

are also subject to anti-takeover provisions under Delaware law, which could also delay or prevent a change of control. Taken together,

these provisions of our charter, bylaws, and Delaware law may discourage transactions that otherwise could provide for the payment of

a premium over prevailing market prices of our common stock and also could limit the price that investors are willing to pay in the future

for shares of our common stock.

Oil

and Gas Operating Risks

Drilling

for and producing oil and natural gas are high risk activities with many uncertainties that could adversely affect our business, financial

condition or results of operations.

Our

future success will depend on the success of our exploitation, exploration, development and production activities. Our oil and natural

gas exploration and production activities are subject to numerous risks beyond our control, including the risk that drilling will not

result in commercially viable oil or natural gas production. Our decisions to purchase, explore, develop or otherwise exploit prospects

or properties will depend in part on the evaluation of data obtained through geophysical and geological analyses, production data and

engineering studies, the results of which are often inconclusive or subject to varying interpretations. Please read “Reserve estimates

depend on many assumptions that may turn out to be inaccurate” (below) for a discussion of the uncertainty involved in these processes.

Our cost of drilling, completing and operating wells is often uncertain before drilling commences. Overruns in budgeted expenditures

are common risks that can make a particular project uneconomical. Further, many factors may curtail, delay or cancel drilling, including

the following:

| |

● |

delays

imposed by or resulting from compliance with regulatory requirements; |

| |

|

|

| |

● |

pressure

or irregularities in geological formations; |

| |

|

|

| |

● |

shortages

of or delays in obtaining equipment and qualified personnel; |

| |

|

|

| |

● |

equipment

failures or accidents; |

| |

|

|

| |

● |

adverse

weather conditions; |

| |

|

|

| |

● |

reductions

in oil and natural gas prices; |

| |

|

|

| |

● |

title

problems; and |

| |

|

|

| |

● |

limitations

in the market for oil and natural gas. |

Cost

overruns, curtailments, delays and cancellations of operations as a result of the above factors and other factors common in our industry

may materially adversely affect our operating results and financial position and our ability to maintain our interests in prospects.

We

are dependent upon third party operators of our oil and gas properties.

Under

the terms of the operating agreements related to our oil and gas properties, third parties act as the operator of each of our oil and

gas wells and control the drilling and operating activities to be conducted on our properties. Therefore, we have limited control over

certain decisions related to activities on our properties, which could affect our results of operations. Decisions over which we have

limited control include:

| |

● |

the

timing and amount of capital expenditures; |

| |

|

|

| |

● |

the

timing of initiating the drilling and recompleting of wells; |

| |

|

|

| |

● |

the

extent of operating costs; and |

| |

|

|

| |

● |

the

level of ongoing production. |

Decisions

made by our operators may be different than those we would make reflecting priorities different than our priorities and may materially

adversely affect our operating results and financial position, including potential declines in production and revenues from properties,

declines in value of properties and lease expirations, among other potential consequences.

Prospects