false

N-2

0001523289

0001523289

2023-04-01

2024-03-31

0001523289

dma:MarketDevelopmentsRiskMember

2023-04-01

2024-03-31

0001523289

dma:BDCRiskMember

2023-04-01

2024-03-31

0001523289

dma:InvestmentAndMarketRiskMember

2023-04-01

2024-03-31

0001523289

us-gaap:CreditRiskMember

2023-04-01

2024-03-31

0001523289

us-gaap:InterestRateRiskMember

2023-04-01

2024-03-31

0001523289

dma:BelowInvestmentGradeRatingRiskMember

2023-04-01

2024-03-31

0001523289

dma:DistributionPolicyRiskMember

2023-04-01

2024-03-31

0001523289

dma:InflationDeflationRiskMember

2023-04-01

2024-03-31

0001523289

dma:StructuredProductsRiskMember

2023-04-01

2024-03-31

0001523289

dma:StructuredNotesRiskMember

2023-04-01

2024-03-31

0001523289

dma:NonUSSecuritiesRiskMember

2023-04-01

2024-03-31

0001523289

dma:ForeignCurrencyRiskMember

2023-04-01

2024-03-31

0001523289

dma:LiquidityRiskMember

2023-04-01

2024-03-31

0001523289

dma:EquityRiskMember

2023-04-01

2024-03-31

0001523289

dma:ManagementRiskMember

2023-04-01

2024-03-31

0001523289

dma:MLPRiskMember

2023-04-01

2024-03-31

0001523289

dma:RealEstateIndustryConcentrationRiskMember

2023-04-01

2024-03-31

0001523289

dma:REITTaxRisksMember

2023-04-01

2024-03-31

0001523289

dma:UnderlyingFundsAIFsRiskMember

2023-04-01

2024-03-31

0001523289

dma:StockholderActivismMember

2023-04-01

2024-03-31

0001523289

dma:AntiTakeoverProvisionsMember

2023-04-01

2024-03-31

0001523289

dma:RisksAssociatedWithAdditionalOfferingsMember

2023-04-01

2024-03-31

0001523289

dma:SecondaryMarketForTheCommonSharesMember

2023-04-01

2024-03-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number 811-22572

Destra Multi-Alternative Fund

(Exact name of registrant as specified in charter)

443 N Willson Avenue

Bozeman, MT 59715

(Address of principal executive offices) (Zip code)

Robert A. Watson

C/O Destra Capital Advisors LLC

443 N Willson Avenue

Bozeman, MT 59715

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 843-6161

Date of fiscal year end: March 31

Date of reporting period: March 31, 2024

Item 1. Reports to Stockholders.

(a)

Destra Multi-Alternative Fund

Annual Report

March 31, 2024

Table of Contents

Dear Shareholders,

We are pleased to present you with your 2024 Annual Report (the “Report”) for the Destra Multi-Alternative Fund (the “Fund”) (NYSE: DMA). This Report covers the period between April 1, 2023, and March 31, 2024 (the “Fiscal Year”).

During the Fiscal Year, the Fund’s performance was up 7.29% on a net asset value basis (“NAV”). Alternatives (US Fund Multistrategy Morningstar Category) were up 10.45%, stocks (S&P 500 Index) were up 29.88% and bonds (Bloomberg U.S. Aggregate Bond Index) were up 1.70%. The common shares of the Fund, as measured by the market price, experienced a dramatic rebound, up 33.61%.

Despite the rebound in market price, as of the date of this Report, there remains a meaningful disconnect between the Fund’s NAV and its market price. This disconnect has led to a large discount between the market price of DMA and its NAV. As a reminder to shareholders, listed closed-end funds like DMA have two prices: 1) the NAV of the portfolio on a per share basis, and 2) the quoted market price at which the common shares of the Fund are traded in the secondary market on the NYSE. The value of these two “prices” frequently diverges, and sometimes meaningfully so, as is the case with DMA currently. Closed-end funds frequently trade at discounts to their NAVs, though some have occasionally traded at premiums to their NAVs.

During the Fiscal Year, the Fund’s Board of Trustees approved the implementation of a term for the Fund that provides that the Fund will dissolve at the close of business on March 31, 2027 (concurrent with the end of its 2026-27 fiscal year), unless certain targets are met. For more details on the parameters of the term and the new structure described above, including a description of the conditions under which the term may be extended, please see the Declaration of Trust filed with the Securities and Exchange Commission on October 6, 2023.

Destra Capital Advisors LLC (“Destra”), the Fund’s adviser, engages frequently with the closed-end fund institutional community, the broad marketplace, and with investors who might be interested in utilizing a multi-alternative strategy with access to unique, non-correlated investments through a listed closed-end fund with intra-day liquidity. In the last year, we have been heartened by the overall acceptance the marketplace has shown to the Fund, which we believe can bring some of the most compelling aspects of alternative investing to the broad marketplace in a liquid format as a listed closed-end fund.

We believe that the Fund may present a particularly attractive opportunity in today’s volatile economic and geopolitical market environments. The Fund is a core alternative solution that seeks returns from capital appreciation and income with an emphasis on income generation. The Fund’s sub-adviser, Validus Growth Investors, LLC (“Validus”), invests in companies and investment opportunities experiencing important points of growth inflection, in their view. As a growth equity manager focused on delivering total returns, Validus has created a proprietary security research and selection process that it uses to select both public and private alternative investments for the portfolio. As recent years have shown, there might be time periods in which traditional stocks and bonds struggle simultaneously. Because of this, many investors have looked to alternatives over the last several years to help provide diversification and seek low or no correlation to their more traditional investment positions. As the broader market comes to better understand Validus’ investment process and the role that an investment in the Fund might play in a diversified portfolio, we believe there is an opportunity for increased investor interest and demand in the Fund.

On the subsequent pages, you will find commentary from Validus discussing the factors that most affected the Fund’s performance during the Fiscal Year, as well as specific details regarding investment results and portfolio holdings. We encourage you to read this Report to learn more about how the Fund performed during the Fiscal Year.

We appreciate the continued confidence you have placed in Destra and our investment partners. Please read this Report carefully and be sure to contact your Financial Advisor or Destra if you have any additional questions.

Sincerely,

Robert A. Watson, CFP®

President

Jake Schultz, CFA®

Secretary

Destra Multi-Alternative Fund

Destra Capital Advisors LLC

| Destra Multi-Alternative Fund |

| Risk Disclosure |

| As of March 31, 2024 (unaudited) |

This document may contain forward-looking statements representing Destra Capital Advisors LLC’s (“Destra”), the portfolio managers’ or sub-adviser’s beliefs concerning future operations, strategies, financial results or other developments. Investors are cautioned that such forward-looking statements involve risks and uncertainties. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond Destra’s, the portfolio managers’ or sub-adviser’s control or are subject to change, actual results could be materially different. There is no guarantee that such forward-looking statements will come to pass.

Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in the Fund. Please read the prospectus carefully before investing. You may obtain a prospectus through the broker dealer, where you hold your shares or by visiting the Fund’s webpage at www.destracapital.com/DMA or by calling Destra at 877-855-3434 or the Fund’s Transfer Agent, Equiniti Trust Company, LLC at 800-591-8238.

| Destra Multi-Alternative Fund |

| Manager’s Commentary (unaudited) |

Manager Discussion & Analysis

Investment Environment

Over the last fiscal year ended March 31, 2024 (the “Fiscal Year”), most asset classes showed impressive strength in the face of an uncertain outlook. Surprising many, traditional equities led the charge shaking off concerns about stubborn inflation and the deferral of Federal Reserve (“Fed”) rate cuts. Investors transitioned to a “higher for longer” narrative with barely a hiccup and without any major dislocations – the US economy proved more resilient than most economists could have imagined with no recession materializing (or even on the current horizon). In part, it seems that last year’s brief challenge to the financial system that started with Silicon Valley Bank and led to a dramatic and forceful response by the Fed was a blessing in disguise, flooding the financial markets with liquidity, and thereby creating “looser” conditions, which overwhelmed the traditional monetary policies of rapidly rising rates and quantitative tightening.

Until recently (into the second quarter of 2024), volatility remained muted and manageable. This despite heightened tensions, geopolitical concerns, deglobalization and a host of other worries. It is notable that for significant portions of the Fiscal Year, traditional fixed income markets were as volatile as equity markets. This proved challenging for traditional asset allocation. Lured by higher short-term rates, many investors simply sat on the sidelines in low-risk cash equivalents, reasoning that 4-5% returns were sufficient in an uncertain world. Others sought refuge in the world of private credit, which provides debt to corporate borrowers outside of the traditional banking system. Private credit exploded in popularity – according to the International Monetary Fund, private credit totaled $2.1 trillion globally at the end of 2023 – by promising higher returns and lower volatility, and so far, it has delivered on both. However, some cautioned about infrequent valuations and techniques such as loan reworks or covenant-light structures that potentially misrepresent underlying distress relative to traditional lender portfolios. With the Fed on hold since the summer of 2023, we found ourselves carefully watching economic data in real time to intuit next moves and possible outcomes. And as the data has unfolded, it has revealed a story that is contradictory, essentially fueling both the bull and bear narratives at the same time.

|

● |

Inflation. The last mile has definitely been a rougher road than the first seven. For three consecutive months (January, February, and March 2024), inflation has headed in the wrong direction, whether it is the Consumer Price Index (“CPI”) (up 3.1%, 3.2% and 3.5%) or the Fed’s preferred measure, Personal Consumption Expenditures(ex food and energy) (up 2.5%, 2.5% and 2.7%). Some items seemingly continue to defy logic – the shelter component, for instance, which makes up 30% of the CPI calculation. Even though other, more reliable data points have indicated rents have peaked and are declining across most markets, “shelter” has remained resilient and stubbornly immovable. Maybe it’s not that surprising given that this is mostly a made-up number based upon surveys of homeowners asked to provide the current market rate for renting their home (that they are not renting). There have been similar curiosities in used car prices, insurance rates, and transportation services. |

|

● |

Employment. For most economists, against the backdrop of tighter monetary policy, slowing inflation without a commensurate decline in employment would have seemed too good to be true. Yet, that’s exactly what has happened. US unemployment has remained at very low levels and increased very slowly – from 3.8% as of the date of this report vs. 3.5% a year ago. However, as the Fiscal Year progressed and as companies, especially in the technology sector, began to focus on operating efficiencies after digesting the excesses of a post-COVID frenzy, staff reductions and layoffs became more common. Where has all the job growth come from? Turns out, mostly from the public sector – three cheers for bigger government! Like many other statistics, we think some of the supposed strength is misleading. |

|

● |

GDP Growth. US gross domestic product (“GDP”) growth came in at 1.6% for Q1 2024, a step-down from the GDP growth of 4.9% in Q3 2023 and 3.4% in Q4 2023. Despite the deceleration, we believe that this is still encouraging, pointing to a resilient economy that has not been torpedoed by Fed actions to date. Although recently, consumer spending, an important driver of economic activity seems to be moderating (at a minimum) with more data points and company-specific commentary suggesting that sustained higher inflation levels are beginning to impinge on consumer activity and sentiment at all income levels. |

Given all that we have discussed, we would be remiss in not addressing the Fed more specifically. The Fed paused rate increases after its 50 basis point hike in July 2023 and has held the Fed Funds Rate steady at 5.25%-5.50% ever since. However, at the same time, the Fed has been engaged in quantitative tightening – allowing $60 billion in US treasuries and $35 billion of agency mortgage-backed securities per month to mature, reducing the Fed’s balance

| Destra Multi-Alternative Fund |

| Manager’s Commentary (unaudited) (continued) |

sheet from $8.7 trillion a year ago to $7.4 trillion today. So far, it appears that the Fed has navigated a very difficult set of challenges – some of which it created itself – in a laudable manner, essentially “sticking the landing” at a very high degree of difficulty. Yet, the debate continues to rage as to whether the Fed should cut rates, stay the course at current levels, or even raise rates from here (a viewpoint which has seemingly picked up steam with the last few months’ inflation data). With the real 10-year interest rate – the nominal 10-year rate minus the inflation rate – significantly positive at roughly 2% (according to the St. Louis Fed) and holding steady over the Fiscal Year even in the face of disinflation, it seems that capital represents a real cost to borrowers and a meaningful return for savers. Maybe monetary policy is “just right” for now.

Is it time to ditch the inverted yield curve as the harbinger of recession? Perhaps. According to a March 21, 2024 Reuter’s article, the current 2-10 year yield curve inversion is now the longest on record. Even still, while the economy is showing signs of stress in certain areas, it appears far from breaching the event horizon that would put us on the path to unavoidable recession. Possible explanations for avoiding the unpleasant outcomes of such a seemingly negative signal lie in the large savings buffer that consumers enjoyed as they exited a COVID world and the increased liquidity delivered by the Fed in other forms to stave off a banking crisis early in 2023.

Market Performance

Traditional Asset Classes. As we shared above, equities performed extremely well over the Fiscal Year, with the S&P 500 Index up 29.9%. Many were offsides all year hiding in cash and waiting for the sustainable downturn that never came. On the other hand, fixed income lagged significantly with the Bloomberg US Aggregate Index up a paltry 1.7% for the Fiscal Year. With yields rising and the Fed’s window for cuts getting pushed further into the future, this “safer” asset class proved a disappointing diversifier.

For equities specifically, diversification also proved unrewarding. Larger cap tech stocks (as represented by the Magnificent Seven – Apple Inc. TKR: AAPL; Alphabet Inc. TKR: GOOG; Amazon.com Inc. TKR: AMZN; Meta Platforms Inc. TKR: META; Microsoft Corp. TKR: MSFT; Nvidia Corp. TKR: NVDA; Tesla Inc. TKR: TSLA) fueled by the boon of artificial intelligence provided the lion’s share of fundamental and stock performance, accounting for 18.7% of the return of S&P500 TR Index during the Fiscal Year. The other 493 constituents mustered only 11.2% of the return and barely grew their revenue and earnings during the Fiscal Year. Yet, many touted the eventual emergence of small cap equities as the Fed headed toward rate cuts, only to have their hopes dashed by “higher for longer” and the challenges this presented for less well-capitalized entities.

On the fixed income side, short duration outperformed during the Fiscal Year with higher investor demand for hiding out at the short end of the curve. Convertible bonds (iShares Convertible Bond ETF – TKR: ICTV), floating rate credit (VanEck Floating Rate ETF – TKR: FLTR), and US high yield (US Corporate High Yield index – TKR: LF98TRUU) outperformed, returning 12.1%, 11.2%, and 8.7%, respectively, for the Fiscal Year. Despite the challenges that high rates present, there has been surprisingly little credit distress so far, which has encouraged investors to reach for yield, seemingly without consequences.

Alternative Asset Classes. Alternative asset classes were largely positive during the Fiscal Year with two exceptions: commodities, as measured by the Bloomberg Commodity Index, and volatility, as represented by the CBOE Volatility Index (“VIX”), which were down -0.6% and -30.4%, respectively. Master limited partnerships, as represented by the Alerian MLP ETF, were the highest performing alternative at 38.2% for the Fiscal Year despite widespread uncertainty regarding global growth, most notably China’s stalled economic activity. However, for oil itself, supply side dynamics proved the greater influence as new geopolitical challenges in the Middle East conspired with peaking Organization of the Petroleum Exporting Countries production to sustain crude oil prices at higher levels for most of the Fiscal Year.

Other yielding alternative asset classes such as real estate investment trusts (“REITs”), business development companies, and closed-end funds posted high single-digit to double-digit returns for the Fiscal Year. Most rose into the end of 2023 as it became clear that the Fed was done raising rates and possibly would begin cutting soon. Many lower quality and potentially troubled investments, having weathered the storm of higher rates through incremental adjustments (such as deferring maintenance and improvements at property level) breathed a sigh of relief as better days (lower rates) appeared on the horizon. As 2024 unfolded, many of these same investments pulled back substantially as the Fed remained resolute in holding rates at higher levels indefinitely. We believe that it is likely that a meaningful, but orderly reckoning awaits many of these distressed situations over the next 12-18 months.

With warnings of the increasing cost of financing, rising government deficits at higher rates and the pullback by certain strategic buyers of US government debt beginning to appear more realistic, alternative “currencies” like gold and Bitcoin flourished – up 12.1% and 148.9% during the Fiscal Year, respectively. Some argue more of a reversion to the

| Destra Multi-Alternative Fund |

| Manager’s Commentary (unaudited) (continued) |

mean as an explanation as Bitcoin was down -37.6% in the year earlier. Yet, good news specific to crypto regulation also helped, including the approval of multiple bitcoin exchange-traded funds by the US Securities & Exchange Commission in early 2024. For our part, we remain skeptical that this “asset class” deserves a place in a portfolio other than for pure speculation.

Fund Portfolio Performance

With respect to the underlying investment portfolio of the Destra Multi-Alternative Fund (the “Fund”), the one-year performance through the Fiscal Year end, was 7.3% on a net asset value (“NAV”) basis. While the NAV underperformed some alternative asset classes, it outperformed bonds as measured by the Bloomberg US Aggregate Bond TR USD Index, the US Dollar, commodities, and volatility, as shown in the chart below. This reflects both the investment objective of the Fund and the composition of the portfolio during the Fiscal Year, which has been designed to seek returns from capital appreciation and income through lower correlations to traditional markets, generating alternative income and providing upside exposure through a combination of public and private securities implemented with an eye towards limiting downside exposure. The results of the Fiscal Year masks some of the exciting performance delivered by liquid strategies, an overall approach that we call “Dynamic Alpha”, that leverages proprietary inflection research from Validus Growth Investors, LLC (the “Sub-Adviser”) in risk managed “wrappers.” The relatively small allocation to liquid strategies punched above its weight during the Fiscal Year to such an extent that we currently intend to continue to reposition illiquid assets into these categories, although past performance is no indication of how such asset classes will perform in the future.

| Index |

|

1-Year |

|

|

3-Year |

|

|

5-Year |

|

|

Inception |

|

| Destra Multi-Alternative Fund – NAV |

|

|

7.3 |

% |

|

|

2.2 |

% |

|

|

0.77 |

% |

|

|

1.23 |

% |

| Destra Multi-Alternative Fund – Mkt. |

|

|

33.6 |

% |

|

|

n/a |

|

|

|

n/a |

|

|

|

n/a |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| US Fund Multistrategy |

|

|

10.5 |

% |

|

|

4.0 |

% |

|

|

3.9 |

% |

|

|

3.0 |

% |

| FTSE NAREIT All Equity REITs |

|

|

8.0 |

% |

|

|

9.6 |

% |

|

|

6.54 |

% |

|

|

7.56 |

% |

| FTSE NAREIT Mortgage REITs |

|

|

17.9 |

% |

|

|

15.9 |

% |

|

|

-0.44 |

% |

|

|

3.95 |

% |

| S-Network Composite Closed-End Fund Index |

|

|

14.8 |

% |

|

|

11.0 |

% |

|

|

5.25 |

% |

|

|

6.36 |

% |

| VanEck BDC Income ETF |

|

|

27.7 |

% |

|

|

12.2 |

% |

|

|

11.74 |

% |

|

|

7.79 |

% |

| Alerian MLP |

|

|

38.2 |

% |

|

|

29.2 |

% |

|

|

11.23 |

% |

|

|

4.81 |

% |

| Bloomberg Equity Long/Short HF Index |

|

|

11.7 |

% |

|

|

2.3 |

% |

|

|

5.88 |

% |

|

|

4.40 |

% |

| Bloomberg Commodity Index |

|

|

-0.6 |

% |

|

|

9.1 |

% |

|

|

6.38 |

% |

|

|

-1.97 |

% |

| Bloomberg US Dollar Spot Index |

|

|

1.2 |

% |

|

|

2.6 |

% |

|

|

0.77 |

% |

|

|

1.98 |

% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Barclays US Aggregate Bond |

|

|

1.7 |

% |

|

|

-2.5 |

% |

|

|

0.36 |

% |

|

|

1.61 |

% |

| S&P 500 Index |

|

|

29.9 |

% |

|

|

11.5 |

% |

|

|

15.04 |

% |

|

|

13.74 |

% |

| Chicago Board Options Exchange SPX Volatility Index |

|

|

-30.4 |

% |

|

|

-12.5 |

% |

|

|

-1.04 |

% |

|

|

-0.88 |

% |

Allocations to idiosyncratic cannabis real estate, equity collateralized loan obligations (“CLOs”), direct private equity, and proprietary liquid strategies were positive contributors to the ‘Fund’s portfolio during the Fiscal Year. We certainly were early in investing in real estate specifically purposed for cannabis operators and, in retrospect, the above-market yields received from asset-backed property investments did not compensate for the ultimate challenges faced by the industry. Like many, we endured some pain as the industry underwent a shake-out of operators related to incoherent regulatory regimes that have scared off capital providers at every level of the capital stack and hampered managing these businesses in the normal course. Managing through this difficult environment has strengthened the focus and efficiency of portfolio real estate investment trusts (“REITs”), such as NewLake and Aventine, which we believe are well-positioned to flourish as the pall is lifted and a more rational environment unfolds. We began to see some of the positive impacts of this changing landscape during the Fiscal Year.

In contrast, the decision to favor CLOs for a significant portion of our alternative income allocation paid off in spades during the Fiscal Year, earning-high-teen double-digit internal rates of return since inception. Additionally, positions taken in early-stage direct private equity opportunities contributed positively to performance during the Fiscal Year by relying on fundamentals rather than multiple inflation and reducing the need for an open initial public offering (“IPO”) window that later stage capital providers depend on for exits. Lastly, liquid strategies that provide hedged exposure to public markets also delivered meaningfully during the Fiscal Year. We believe that the fundamental underpinnings of this approach may continue to add value in a more meaningful way as we increase allocations into the future.

| Destra Multi-Alternative Fund |

| Manager’s Commentary (unaudited) (continued) |

Despite the challenges in the private equity world, originally brought on by the Silicon Valley Bank debacle in February 2023, we saw several of the Fund’s early-stage direct private equity investments mark up to higher valuations during the Fiscal Year through successful capital raises of equity or convertible debt. However, similar to what we have seen industry-wide, certain positions were forced to re-evaluate their business models, create greater efficiencies and even restructure in order to maximize their opportunity and minimize their cash burn. Overall, we believe our direct equity exposure is well-positioned and well-capitalized for future growth.

Not every real estate investment performed well during the Fiscal Year. Industrial real estate as implemented through Clarion Lion Industrial Trust hit a soft patch after years of consistent 15-20% total annual returns. Fundamentally, supply has finally caught up to demand after years of development fueled originally by the COVID crisis. Rents, while still growing, have slowed their advance. This oversupplied condition will take some time to normalize, creating a ceiling for cap rates. At the same time, the new normal for rates has meant that operating cash flows are valued using higher discount rates for appraisal purposes, impacting NAV performance. Coincidentally, as part of prudent portfolio management, we have been right sizing the position over the past 12 months after a great run. Higher rates have also impacted the appraisals for the Fund’s low-income multi-family position and the timing of property-specific value realizations. However, this asset class has proven very resilient, especially during recessionary periods, and remains a sought-after asset class due to its favorable tax characteristics. Lastly, given the challenges faced by cannabis operators and the hyper-competitive environment described above, one of the Fund’s private REIT positions has not been able to diversify quickly enough away from its single-tenant concentration risk and is in the process of repositioning portions of its portfolio, which has negatively impacted its carrying value.

The Fund’s publicly traded market price was up 33.6% over the Fiscal Year, outperforming the S&P 500 Index by +3.7%. During this period, the Fund had the 4th highest total market return out of 49 closed end funds defined in the special equity peer group by Citadel Securities and the 2nd highest market return of the DMA Exchange Listed Trading Group Trading activity improved during the Fiscal Year as well with volume improving from roughly 350,000 shares per month for the 12 months ended March 31, 2023 to roughly 950,000 per month for the Fiscal Year. As a result, the NAV discount narrowed meaningfully over the last year, from –44% in March 2023 to –29.4% in March 2024.

Portfolio Positioning

The Fund implements a multi-strategy approach to alternative investing, utilizing public and private investments to deliver non-correlated income and asymmetric growth opportunities. We believe the Fund’s unique combination of strategies represents the first of its kind in the closed-end fund world – a listed public/private “crossover” strategy with what we believe has significant yield potential.

Evaluating new illiquid, multi-year alternative investment opportunities in a changing and dynamic fiscal and monetary environment remains challenging. As we noted last year, for some time we have been skeptical that most illiquid alternatives offered illiquidity premiums that were attractive enough to adequately reward investors for the risk of locking up capital for long periods. Consistent with that, the last commitment made to such an illiquid investment was Canyon CLO Fund III. As of March 31, 2024, remaining capital commitments to fund-type architectures represented just 1.6% of the Fund, down from 8.1% as of March 31, 2023. Given the current term structure of the Fund, it is unlikely that another such structure will be implemented to access these illiquid alternatives.

Instead, we are focused on re-distributing capital to risk-reward opportunities where we can customize the time horizon and terms more directly to meet the Fund’s objectives in three main areas: proprietary liquid strategies, market-linked notes and direct private equity. In addition, largely for purposes of generating non-correlated income, the Fund will continue to maintain a healthy allocation to real estate and CLOs, consistent with its investment mandate. With respect to real estate specifically, we expect the focus to be on specialty asset classes with unique characteristics, like low-income housing, industrial/warehouse and cannabis. Overall, this asset-class specific approach has been rewarding in the past for the Fund despite some challenges with individual investments.

Perspective & Outlook

Importantly for financial markets, investors are balanced on a razor’s edge awaiting the next data point about the economic growth, inflation, jobs, and treasury auctions. In short, a data dependent world is a more volatile world. And even if one could predict certain economic statistics – and we think we have proven that no one really can – one would also have to predict how the market will react to that new information on any given trading day. The derivative nature of this equation has the potential for much wider outcomes. Since the end of Q1’24, we have seen volatility in traditional asset classes pick up substantially with the VIX and the ICE BofA MOVE Index (“MOVE”) up 20.3% and 24.4%, respectively through April 30, 2024.

| Destra Multi-Alternative Fund |

| Manager’s Commentary (unaudited) (continued) |

With monetary policy continuing to be a headwind, capital has a meaningful cost. We believe marginal investments and strategies in certain asset classes based, in part, upon favorable monetary tailwinds will be susceptible to draw downs or underperformance. So far, investors in these asset classes have managed to tread water by deferring. Most importantly, the longer that the Fed stays “higher” with rates, the more likely the reckoning for certain sectors of real estate – including lower quality office, retail and hospitality properties – in magnitudes that may test the strength of the banking system. As we noted, the long-term nature of most leases, low borrowing costs, and the lagging nature of appraisals have continued to allow the sense of health and stability to persist. Without a single catalyst pushing closure, we expect the headwind to be a drawn out, low-intensity burn.

With traditional markets expected to be volatile as monetary, economic, and geopolitical issues play out, we believe alternative asset classes continue to represent opportunity, but only in the highest quality strategies implemented by experienced teams that have navigated multiple cycles and are confident enough to pivot quickly amid dynamic market conditions or direct access to opportunities.

Similar to last year, direct private equity opportunities continue to be attractive while traditional funding sources continue to show restraint due to: (1) the need to be seen as rational and prudent allocators of capital; (2) the prioritization of rationalizing portfolios and extending runways for existing investments, and (3) the belief that founders have yet to adapt their expectations on pricing and terms to new realities. Further, the effect of continuation funds has served to preserve the status quo and postpone a major market realignment, which eventually may be essential for reopening the IPO window.

We maintain that prioritizing liquidity and identifying quality assets and strategies that can perform across a range of volatility regimes will be critical to investors navigating uncomfortable levels of uncertainty. It is our belief that active management can add value by implementing time-tested processes, leveraging value-added relationships to boost investment-specific performance, enhancing fundamental research with augmented diligence, and most importantly, understanding and positioning the portfolio to maximize shareholder return regardless of environment.

| Destra Multi-Alternative Fund |

| Performance and Graphical Illustration |

| March 31, 2024 (unaudited) |

| |

|

|

|

|

|

|

|

|

|

|

Inception Date:

July 2, 2014 |

|

| Fund / Indexes |

|

1 Year |

|

|

3 year

Average Annual |

|

|

5 year

Average Annual |

|

|

Since Inception

Average Annual |

|

| Destra Multi-Alternative Fund* |

|

|

7.29 |

% |

|

|

2.24 |

% |

|

|

0.77 |

% |

|

|

1.23 |

% |

| Bloomberg U.S. Aggregate Bond Index |

|

|

1.70 |

% |

|

|

-2.46 |

% |

|

|

0.36 |

% |

|

|

1.43 |

% |

| S&P 500 Total Return Index |

|

|

29.88 |

% |

|

|

11.49 |

% |

|

|

15.05 |

% |

|

|

12.64 |

% |

The performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. For performance information current to the most recent month-end, please call Destra Capital at 877-855-3434.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed-rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark.

The S&P 500 Total Return Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

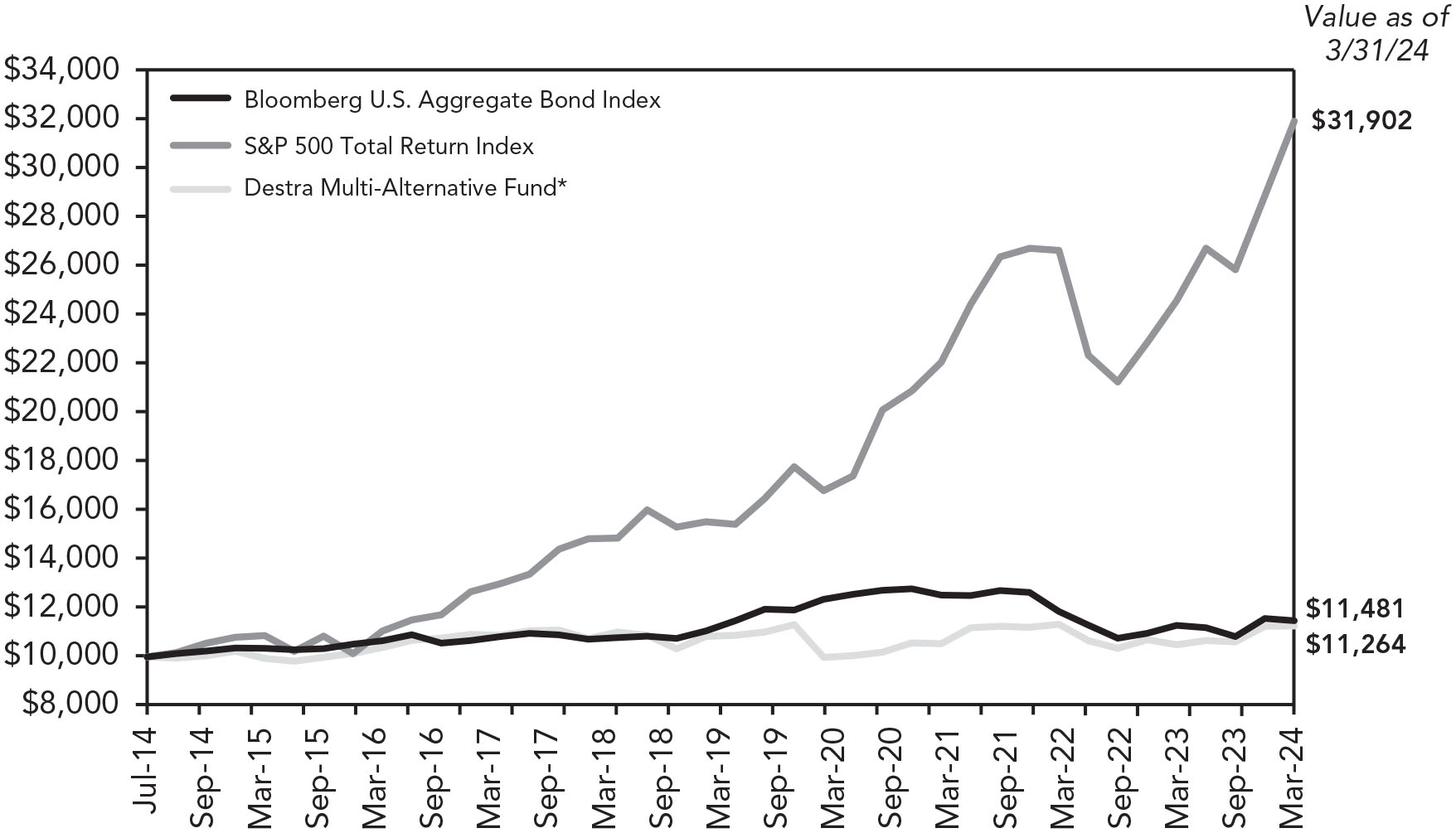

Growth of an Assumed $10,000 Investment

This graph illustrates the hypothetical investment of $10,000 in the Fund*, Common shares, from July 2, 2014 to March 31, 2024. The Average Annual and Cumulative Total Return table and Growth of Assumed $10,000 Investment graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

|

* |

The Fund’s shares began trading on the New York Stock Exchange (“NYSE”) on January 13, 2022 under NYSE ticker symbol “DMA.” To facilitate the listing of the Fund’s shares on the NYSE, the Fund redesignated its Class A, Class C and Class T shares as Class I shares and eliminated all share class designations. Consequently, the Fund’s shares are now referred to as shares of beneficial interest or common shares. Performance represents Class I from July 2, 2014 through January 12, 2022 and Common share performance thereafter. |

| Destra Multi-Alternative Fund |

| Schedule of Investments |

| As of March 31, 2024 |

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

COMMON STOCKS – 14.7% |

|

|

|

|

| |

|

|

|

AEROSPACE/DEFENSE – 0.1% |

|

|

|

|

| |

613 |

|

|

Moog, Inc., Class A |

|

$ |

97,865 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

AGRICULTURE – 0.5% |

|

|

|

|

| |

7,774 |

|

|

Archer-Daniels-Midland Co. |

|

|

488,285 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

AUTO MANUFACTURERS – 0.3% |

|

|

|

|

| |

1,152 |

|

|

Cummins, Inc. |

|

|

339,437 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

BANKS – 0.6% |

|

|

|

|

| |

5,115 |

|

|

Morgan Stanley |

|

|

481,628 |

|

| |

1,000 |

|

|

PNC Financial Services Group, Inc. |

|

|

161,600 |

|

| |

|

|

|

|

|

|

643,228 |

|

| |

|

|

|

BIOTECHNOLOGY – 0.1% |

|

|

|

|

| |

2,321 |

|

|

Corteva, Inc. |

|

|

133,852 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

CHEMICALS – 0.1% |

|

|

|

|

| |

1,454 |

|

|

International Flavors & Fragrances, Inc. |

|

|

125,029 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

COMPUTERS – 0.3% |

|

|

|

|

| |

3,764 |

|

|

Cognizant Technology Solutions Corp., Class A |

|

|

275,864 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

DIVERSIFIED FINANCIAL SERVICES – 0.3% |

|

|

|

|

| |

1,445 |

|

|

American Express Co. |

|

|

329,012 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

ELECTRIC – 0.5% |

|

|

|

|

| |

7,227 |

|

|

NextEra Energy, Inc. |

|

|

461,878 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

ENTERTAINMENT – 0.1% |

|

|

|

|

| |

2,570 |

|

|

Cedar Fair LP |

|

|

107,683 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

FINANCIAL SERVICES – 0.2% |

|

|

|

|

| |

1,530 |

|

|

Blackstone Group, Inc. |

|

|

200,996 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

FOOD SERVICE – 0.2% |

|

|

|

|

| |

731 |

|

|

McDonald’s Corp. |

|

|

206,105 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

HEALTHCARE-SERVICES – 0.5% |

|

|

|

|

| |

600 |

|

|

Elevance Health, Inc. |

|

|

311,124 |

|

| |

420 |

|

|

UnitedHealth Group, Inc. |

|

|

207,774 |

|

| |

|

|

|

|

|

|

518,898 |

|

| |

|

|

|

INSURANCE – 0.3% |

|

|

|

|

| |

3,327 |

|

|

Principal Financial Group, Inc. |

|

|

287,153 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

INTERNET – 2.0% |

|

|

|

|

| |

4,100 |

|

|

Meta Platforms, Inc. - Class A(1)* |

|

|

1,990,878 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

INVESTMENT COMPANIES – 2.5% |

|

|

|

|

| |

160,645 |

|

|

Blue Owl Capital Corp.(1)* |

|

|

2,470,720 |

|

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

COMMON STOCKS (continued) |

|

|

|

|

| |

|

|

|

MACHINERY-DIVERSIFIED – 0.3% |

|

|

|

|

| |

628 |

|

|

Deere & Co. |

|

$ |

257,945 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

MEDIA – 0.5% |

|

|

|

|

| |

12,254 |

|

|

Comcast Corp., Class A |

|

|

531,211 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

MINING – 0.4% |

|

|

|

|

| |

12,163 |

|

|

Newmont Mining Corp. |

|

|

435,922 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

MISCELLANEOUS MANUFACTURING – 0.4% |

|

|

|

|

| |

687 |

|

|

Parker-Hannifin Corp. |

|

|

381,828 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

OIL & GAS – 1.2% |

|

|

|

|

| |

2,784 |

|

|

EOG Resources, Inc. |

|

|

355,907 |

|

| |

3,943 |

|

|

Marathon Petroleum Corp. |

|

|

794,513 |

|

| |

|

|

|

|

|

|

1,150,420 |

|

| |

|

|

|

PHARMACEUTICALS – 0.2% |

|

|

|

|

| |

917 |

|

|

AbbVie, Inc. |

|

|

166,986 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

RETAIL – 0.5% |

|

|

|

|

| |

1,464 |

|

|

Genuine Parts Co. |

|

|

226,818 |

|

| |

2,832 |

|

|

The TJX Cos., Inc. |

|

|

287,221 |

|

| |

|

|

|

|

|

|

514,039 |

|

| |

|

|

|

SEMICONDUCTORS – 0.7% |

|

|

|

|

| |

1,749 |

|

|

Analog Devices, Inc. |

|

|

345,935 |

|

| |

268 |

|

|

Broadcom Ltd. |

|

|

355,210 |

|

| |

|

|

|

|

|

|

701,145 |

|

| |

|

|

|

SOFTWARE – 0.2% |

|

|

|

|

| |

584 |

|

|

Microsoft Corp. |

|

|

245,700 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

TELECOMMUNICATIONS – 0.7% |

|

|

|

|

| |

20,034 |

|

|

Corning, Inc. |

|

|

660,321 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

TRANSPORTATION – 1.0% |

|

|

|

|

| |

2,193 |

|

|

Union Pacific Corp. |

|

|

539,325 |

|

| |

3,067 |

|

|

United Parcel Service, Inc., Class B |

|

|

455,848 |

|

| |

|

|

|

|

|

|

995,173 |

|

| |

|

|

|

TOTAL COMMON STOCKS

(Cost $14,613,446) |

|

|

14,717,573 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

MEDIUM TERM NOTES – 1.5% |

|

|

|

|

| |

|

|

|

BANKS – 1.5% |

|

|

|

|

| |

1,500,000 |

|

|

Credit Suisse AG London, 0.0%, 09/18/25(2)(3)(4) |

|

|

1,500,000 |

|

| |

|

|

|

TOTAL MEDIUM TERM NOTES

(Cost $1,500,000) |

|

|

1,500,000 |

|

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Schedule of Investments (continued) |

| As of March 31, 2024 |

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

PRIVATE COMPANIES – 16.6% |

|

|

|

|

| |

2,000,000 |

|

|

Always AI, Inc., Convertible Debt, 8.0%, 09/29/25(2)(3)(4) |

|

$ |

2,000,000 |

|

| |

744,880 |

|

|

Always AI, Inc. (254,113 Series A-1, 490,767 Series B) Preferred Stock(2)(3)(4) |

|

|

3,885,088 |

|

| |

179,641 |

|

|

Clear Street Group, Inc., Series B-1 Preferred Stock(2)(3)(4) |

|

|

1,500,002 |

|

| |

23,723 |

|

|

Eat Just, Inc., Series F Common Stock(2)(3)(4) |

|

|

472,660 |

|

| |

56,331 |

|

|

GOSITE, Inc., Convertible Debt, 10.0%, 04/19/25(2)(4) |

|

|

56,331 |

|

| |

542,467 |

|

|

GOSITE, Inc., Series A-1 Preferred Stock(2)(3)(4) |

|

|

2,738,144 |

|

| |

750,000 |

|

|

Iridia, Inc., Convertible Debt, 8.0%, 06/20/25(2)(4) |

|

|

750,000 |

|

| |

497,216 |

|

|

Iridia, Inc., Series A-3 Preferred Stock(2)(3)(4) |

|

|

1,249,538 |

|

| |

2,387,937 |

|

|

Nurture Life, Inc., Series B Preferred Stock(2)(3)(4) |

|

|

3,946,543 |

|

| |

|

|

|

TOTAL PRIVATE COMPANIES

(Cost $12,918,545) |

|

|

16,598,306 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

PURCHASED OPTIONS CONTRACTS* – 0.4% |

|

|

|

|

| |

|

|

|

CALL OPTIONS – 0.4% |

|

|

|

|

| |

5 |

|

|

Adobe, Inc.

Exercise Price: $670,

Notional Amount: $335,000,

Expiration Date: 06/21/2024(3) |

|

|

820 |

|

| |

7 |

|

|

Adobe, Inc.

Exercise Price: $630,

Notional Amount: $441,000,

Expiration Date: 09/20/2024(3) |

|

|

8,505 |

|

| |

20 |

|

|

Airbnb, Inc.

Exercise Price: $175,

Notional Amount: $350,000,

Expiration Date: 06/21/2024(3) |

|

|

16,800 |

|

| |

20 |

|

|

Airbnb, Inc.

Exercise Price: $180,

Notional Amount: $360,000,

Expiration Date: 06/21/2024(3) |

|

|

13,200 |

|

| |

15 |

|

|

Deere & Company

Exercise Price: $500,

Notional Amount: $750,000,

Expiration Date: 06/21/2024(3) |

|

|

1,500 |

|

| |

75 |

|

|

DraftKings, Inc.

Exercise Price: $60,

Notional Amount: $450,000,

Expiration Date: 01/17/2025(3) |

|

|

30,750 |

|

| |

4 |

|

|

Eli Lilly And Co.

Exercise Price: $820,

Notional Amount: $328,000,

Expiration Date: 01/17/2025(3) |

|

|

36,000 |

|

| |

25 |

|

|

Enphase Energy, Inc.

Exercise Price: $280,

Notional Amount: $700,000,

Expiration Date: 06/21/2024(3) |

|

|

413 |

|

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

PURCHASED OPTIONS CONTRACTS (continued) |

|

|

|

|

| |

|

|

|

CALL OPTIONS (continued) |

|

|

|

|

| |

20 |

|

|

Marvell Technology, Inc.

Exercise Price: $85,

Notional Amount: $170,000,

Expiration Date: 06/21/2024(3) |

|

$ |

5,100 |

|

| |

10 |

|

|

Mp Materials Corp.

Exercise Price: $45,

Notional Amount: $45,000,

Expiration Date: 01/17/2025(3) |

|

|

225 |

|

| |

30 |

|

|

Mp Materials Corp.

Exercise Price: $50,

Notional Amount: $150,000,

Expiration Date: 01/17/2025(3) |

|

|

600 |

|

| |

10 |

|

|

Netflix, Inc.

Exercise Price: $620,

Notional Amount: $620,000,

Expiration Date: 06/21/2024(3) |

|

|

38,800 |

|

| |

130 |

|

|

Palantir Technologies, Inc.

Exercise Price: $27,

Notional Amount: $351,000,

Expiration Date: 06/21/2024(3) |

|

|

18,590 |

|

| |

150 |

|

|

Palantir Technologies, Inc.

Exercise Price: $30,

Notional Amount: $450,000,

Expiration Date: 10/18/2024(3) |

|

|

31,800 |

|

| |

12 |

|

|

Palo Alto Networks, Inc.

Exercise Price: $330,

Notional Amount: $396,000,

Expiration Date: 09/20/2024(3) |

|

|

20,856 |

|

| |

40 |

|

|

Pinterest, Inc.

Exercise Price: $40,

Notional Amount: $160,000,

Expiration Date: 06/21/2024(3) |

|

|

4,720 |

|

| |

95 |

|

|

Pinterest, Inc.

Exercise Price: $45,

Notional Amount: $427,500,

Expiration Date: 10/18/2024(3) |

|

|

14,440 |

|

| |

50 |

|

|

Roblox Corp.

Exercise Price: $65,

Notional Amount: $325,000,

Expiration Date: 06/21/2024(3) |

|

|

700 |

|

| |

18 |

|

|

Shopify, Inc.

Exercise Price: $75,

Notional Amount: $135,000,

Expiration Date: 06/21/2024(3) |

|

|

16,272 |

|

| |

15 |

|

|

Snowflake, Inc.

Exercise Price: $260,

Notional Amount: $390,000,

Expiration Date: 06/21/2024(3) |

|

|

1,125 |

|

| |

20 |

|

|

Snowflake, Inc.

Exercise Price: $240,

Notional Amount: $480,000,

Expiration Date: 06/21/2024(3) |

|

|

2,720 |

|

| |

10 |

|

|

Snowflake, Inc.

Exercise Price: $230,

Notional Amount: $230,000,

Expiration Date: 01/17/2025(3) |

|

|

10,100 |

|

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Schedule of Investments (continued) |

| As of March 31, 2024 |

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

PURCHASED OPTIONS CONTRACTS (continued) |

|

|

|

|

| |

|

|

|

CALL OPTIONS (continued) |

|

|

|

|

| |

8 |

|

|

Tesla, Inc.

Exercise Price: $350,

Notional Amount: $280,000,

Expiration Date: 09/20/2024(3) |

|

$ |

1,112 |

|

| |

18 |

|

|

Tesla, Inc.

Exercise Price: $450,

Notional Amount: $810,000,

Expiration Date: 09/20/2024(3) |

|

|

1,116 |

|

| |

11 |

|

|

Tesla, Inc.

Exercise Price: $260,

Notional Amount: $286,000,

Expiration Date: 01/17/2025(3) |

|

|

12,320 |

|

| |

35 |

|

|

Trade Desk, Inc.

Exercise Price: $110,

Notional Amount: $385,000,

Expiration Date: 06/21/2024(3) |

|

|

6,440 |

|

| |

16 |

|

|

Trade Desk, Inc.

Exercise Price: $100,

Notional Amount: $160,000,

Expiration Date: 09/20/2024(3) |

|

|

12,640 |

|

| |

16 |

|

|

Trade Desk, Inc.

Exercise Price: $105,

Notional Amount: $168,000,

Expiration Date: 10/18/2024(3) |

|

|

11,000 |

|

| |

60 |

|

|

UiPath, Inc.

Exercise Price: $30,

Notional Amount: $180,000,

Expiration Date: 06/21/2024(3) |

|

|

2,640 |

|

| |

8 |

|

|

Vertex

Pharmaceuticals Incorporated

Exercise Price: $400,

Notional Amount: $320,000,

Expiration Date:

06/21/2024(3) |

|

|

28,160 |

|

| |

18 |

|

|

Zscaler, Inc.

Exercise Price: $290,

Notional Amount: $522,000,

Expiration Date: 09/20/2024(3) |

|

|

6,300 |

|

| |

|

|

|

TOTAL CALL OPTIONS |

|

|

355,764 |

|

| |

|

|

|

TOTAL PURCHASED OPTIONS CONTRACTS

(Cost $546,594) |

|

|

355,764 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

CONTINGENT VALUE RIGHTS – 0.2% |

|

|

|

|

| |

|

|

|

PHARMACEUTICALS – 0.0% |

|

|

|

|

| |

142,000 |

|

|

Bristol-Myers Squibb Co.(2)(3) |

|

|

— |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

REAL ESTATE – 0.2% |

|

|

|

|

| |

456,540 |

|

|

Hospitality Investors Trust, Inc.(2)(3)(4)* |

|

|

241,226 |

|

| |

579,536 |

|

|

Ready Capital Corp.(2)(3)(4) |

|

|

— |

|

| |

|

|

|

|

|

|

241,226 |

|

| |

|

|

|

TOTAL CONTINGENT VALUE RIGHTS

(Cost $9,395,584) |

|

|

241,226 |

|

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

WARRANTS – 1.0% |

|

|

|

|

| |

|

|

|

FOOD – 1.0% |

|

|

|

|

| |

878,570 |

|

|

Nurture Life, Inc.(2)(3)(4) |

|

$ |

991,088 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

SOFTWARE – 0.0% |

|

|

|

|

| |

1 |

|

|

Always AI, Inc.(2)(3)(4) |

|

|

— |

|

| |

|

|

|

TOTAL WARRANTS

(Cost $—) |

|

|

991,088 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

REAL ESTATE INVESTMENT TRUSTS – 28.7% |

|

|

|

|

| |

|

|

|

LISTED REAL ESTATE INVESTMENT TRUSTS – 8.9% |

|

|

|

|

| |

275,000 |

|

|

Newlake Capital Partners, Inc. |

|

|

5,238,750 |

|

| |

4,175 |

|

|

Prologis, Inc. |

|

|

543,669 |

|

| |

345,947 |

|

|

Ready Capital Corp. |

|

|

3,158,496 |

|

| |

|

|

|

TOTAL LISTED REAL ESTATE INVESTMENT TRUSTS |

|

|

8,940,915 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

NON-LISTED REAL ESTATE INVESTMENT TRUSTS – 7.3% |

|

|

|

|

| |

344,812 |

|

|

Healthcare Trust, Inc., Common Stock(2)(4)* |

|

|

4,448,161 |

|

| |

1,061,081 |

|

|

NorthStar Healthcare Income, Inc., Common Stock(2)(3)(4)* |

|

|

2,818,031 |

|

| |

|

|

|

TOTAL NON-LISTED REAL ESTATE INVESTMENT TRUSTS |

|

|

7,266,192 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

PRIVATE REAL ESTATE INVESTMENT TRUSTS – 12.5% |

|

|

|

|

| |

715,000 |

|

|

Aventine Property Group, Inc., Common Stock(2)(4) |

|

|

7,030,098 |

|

| |

715,000 |

|

|

Treehouse Real Estate Investment Trust, Inc., Common Stock(2)(4) |

|

|

5,525,693 |

|

| |

|

|

|

TOTAL PRIVATE REAL ESTATE INVESTMENT TRUSTS |

|

|

12,555,791 |

|

| |

|

|

|

TOTAL REAL ESTATE INVESTMENT TRUSTS

(Cost $37,296,145) |

|

|

28,762,898 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

ALTERNATIVE INVESTMENT FUNDS – 45.9% |

|

|

|

|

| |

250 |

|

|

Arboretum Core Asset Fund LP(4)(5) |

|

|

2,401,478 |

|

| |

— |

|

|

Canyon CLO Fund II LP(3)(4)(5)(6) |

|

|

8,799,067 |

|

| |

— |

|

|

Canyon CLO Fund III (Cayman) Ltd.(3)(4)(5)(6) |

|

|

14,678,640 |

|

| |

3,483 |

|

|

Clarion Lion Industrial Trust(4)(5) |

|

|

13,248,190 |

|

| |

— |

|

|

Ovation Alternative Income Fund(4)(5)(6) |

|

|

476,153 |

|

| |

159 |

|

|

Preservation REIT 1, Inc.(4)(5) |

|

|

6,382,201 |

|

| |

|

|

|

TOTAL ALTERNATIVE INVESTMENT FUNDS

(Cost $29,784,591) |

|

|

45,985,729 |

|

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Schedule of Investments (continued) |

| As of March 31, 2024 |

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

SHORT-TERM INVESTMENTS – 8.5% |

|

|

|

|

| |

|

|

|

MONEY MARKET FUND – 8.5% |

|

|

|

|

| |

8,472,015 |

|

|

Fidelity Investments Money Market Funds - Government Portfolio, Class I, 5.21%(1)(7) |

|

$ |

8,472,015 |

|

| |

|

|

|

TOTAL SHORT-TERM INVESTMENTS

(Cost $8,472,015) |

|

|

8,472,015 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

TOTAL INVESTMENTS – 117.5%

(Cost $114,526,920) |

|

|

117,624,599 |

|

| |

|

|

|

Liabilities in Excess of Other Assets – (17.5)% |

|

|

(17,557,308 |

) |

| |

|

|

|

TOTAL NET ASSETS – 100.0% |

|

$ |

100,067,291 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

WRITTEN OPTIONS CONTRACTS* – (0.2)% |

|

|

|

|

| |

|

|

|

CALL OPTIONS – (0.2)% |

|

|

|

|

| |

(7 |

) |

|

American Express Company

Exercise Price: $220,

Notional Amount: $(154,000),

Expiration Date: 06/21/2024 |

|

|

(11,165 |

) |

| |

(17 |

) |

|

Analog Devices, Inc.

Exercise Price: $210,

Notional Amount: $(357,000),

Expiration Date: 06/21/2024 |

|

|

(9,350 |

) |

| |

(77 |

) |

|

Archer-Daniels-Midland Co.

Exercise Price: $63,

Notional Amount: $(481,250),

Expiration Date: 06/21/2024 |

|

|

(25,872 |

) |

| |

(15 |

) |

|

Blackstone, Inc.

Exercise Price: $135,

Notional Amount: $(202,500),

Expiration Date: 06/21/2024 |

|

|

(9,300 |

) |

| |

(2 |

) |

|

Broadcom, Inc.

Exercise Price: $1,400,

Notional Amount: $(280,000),

Expiration Date: 06/21/2024 |

|

|

(13,200 |

) |

| |

(37 |

) |

|

Cognizant Technology Solutions Corp.

Exercise Price: $83,

Notional Amount: $(305,250),

Expiration Date: 06/21/2024 |

|

|

(1,572 |

) |

| |

(100 |

) |

|

Corning, Inc.

Exercise Price: $33,

Notional Amount: $(330,000),

Expiration Date: 06/21/2024 |

|

|

(13,700 |

) |

| |

(6 |

) |

|

Deere & Co.

Exercise Price: $400,

Notional Amount: $(240,000),

Expiration Date: 06/21/2024 |

|

|

(16,728 |

) |

| |

(6 |

) |

|

Elevance Health, Inc.

Exercise Price: $520,

Notional Amount: $(312,000),

Expiration Date: 06/21/2024 |

|

|

(13,080 |

) |

| |

(12 |

) |

|

EOG Resources, Inc.

Exercise Price: $120,

Notional Amount: $(144,000),

Expiration Date: 06/21/2024 |

|

|

(12,480 |

) |

Shares/

Contracts/

Principal |

|

|

Security |

|

Value |

|

| |

|

|

|

WRITTEN OPTIONS CONTRACTS (continued) |

|

|

|

|

| |

|

|

|

CALL OPTIONS (continued) |

|

|

|

|

| |

(39 |

) |

|

Marathon Petroleum Corp.

Exercise Price: $210,

Notional Amount: $(819,000),

Expiration Date: 07/19/2024 |

|

$ |

(37,440 |

) |

| |

(120 |

) |

|

Newmont Corporation

Exercise Price: $38,

Notional Amount: $(450,000),

Expiration Date: 06/21/2024 |

|

|

(21,600 |

) |

| |

(72 |

) |

|

NextEra Energy, Inc.

Exercise Price: $65,

Notional Amount: $(468,000),

Expiration Date: 06/21/2024 |

|

|

(19,512 |

) |

| |

(41 |

) |

|

Prologis, Inc.

Exercise Price: $135,

Notional Amount: $(553,500),

Expiration Date: 08/16/2024 |

|

|

(24,600 |

) |

| |

(21 |

) |

|

Union Pacific Corp.

Exercise Price: $260,

Notional Amount: $(546,000),

Expiration Date: 06/21/2024 |

|

|

(8,820 |

) |

| |

(15 |

) |

|

United Parcel Service, Inc.

Exercise Price: $155,

Notional Amount: $(232,500),

Expiration Date: 06/21/2024 |

|

|

(6,450 |

) |

| |

|

|

|

TOTAL CALL OPTIONS |

|

|

(244,869 |

) |

| |

|

|

|

TOTAL WRITTEN OPTIONS CONTRACTS

(Proceeds $(191,135)) |

|

|

(244,869 |

) |

| |

|

|

|

|

|

|

|

|

| |

|

|

|

EXCHANGE-TRADED FUNDS SOLD SHORT* – (2.3)% |

|

|

|

|

| |

(9,900 |

) |

|

Direxion Daily S&P 500 Bull 3X |

|

|

(1,326,897 |

) |

| |

(5,160 |

) |

|

iShares Transportation Average ETF |

|

|

(363,264 |

) |

| |

(9,800 |

) |

|

ProShares UltraPro QQQ |

|

|

(603,288 |

) |

| |

|

|

|

TOTAL EXCHANGE-TRADED FUNDS SOLD SHORT

(Proceeds $(802,222)) |

|

|

(2,293,449 |

) |

| |

|

|

|

TOTAL SHORT SECURITIES

(Proceeds $(993,357)) |

|

$ |

(2,538,318 |

) |

|

* |

All securities are pledged as collateral except for securities indentified with a * superscript. |

|

(1) |

All or a portion of this security is segregated as collateral for securities sold short. |

|

(2) |

Fair valued using significant unobservable inputs (See Note 2). |

|

(3) |

Non-income producing security. |

|

(4) |

Restricted investment as to resale (See Note 2). |

|

(5) |

Investments in Alternative Investment Funds are valued using net asset value as a practical expedient. See Note 2 for respective investment strategies, unfunded commitments and redemptive restrictions. |

|

(6) |

Alternative investment fund does not issue shares. |

|

(7) |

The rate is the annualized seven-day yield as of March 31, 2024. |

ETF – Exchange-Traded Fund

LP – Limited Partnership

REIT – Real Estate Investment Trusts

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Schedule of Investments (continued) |

| As of March 31, 2024 |

| |

|

Percent of |

|

| |

|

Net Assets |

|

| Alternative Investment Funds |

|

|

45.9 |

% |

| Real Estate Investment Trusts |

|

|

|

|

| Private Real Estate Investment Trusts |

|

|

12.5 |

% |

| Listed Real Estate Investment Trusts |

|

|

8.9 |

% |

| Non-Listed Real Estate Investment Trusts |

|

|

7.3 |

% |

| Private Companies |

|

|

16.6 |

% |

| Common Stocks |

|

|

|

|

| Investment Companies |

|

|

2.5 |

% |

| Internet |

|

|

2.0 |

% |

| Oil & Gas |

|

|

1.2 |

% |

| Transportation |

|

|

1.0 |

% |

| Semiconductors |

|

|

0.7 |

% |

| Telecommunications |

|

|

0.7 |

% |

| Banks |

|

|

0.6 |

% |

| Media |

|

|

0.5 |

% |

| Healthcare-Services |

|

|

0.5 |

% |

| Electric |

|

|

0.5 |

% |

| Agriculture |

|

|

0.5 |

% |

| Retail |

|

|

0.5 |

% |

| Miscellaneous Manufacturing |

|

|

0.4 |

% |

| Mining |

|

|

0.4 |

% |

| Diversified Financial Services |

|

|

0.3 |

% |

| Auto Manufacturers |

|

|

0.3 |

% |

| Machinery-Diversified |

|

|

0.3 |

% |

| Computers |

|

|

0.3 |

% |

| Insurance |

|

|

0.3 |

% |

| Software |

|

|

0.2 |

% |

| Pharmaceuticals |

|

|

0.2 |

% |

| Financial Services |

|

|

0.2 |

% |

| Food Service |

|

|

0.2 |

% |

| Aerospace/Defense |

|

|

0.1 |

% |

| Chemicals |

|

|

0.1 |

% |

| Entertainment |

|

|

0.1 |

% |

| Biotechnology |

|

|

0.1 |

% |

| Contingent Value Rights |

|

|

|

|

| Real Estate |

|

|

0.2 |

% |

| Pharmaceuticals |

|

|

0.0 |

% |

| Purchased Options Contracts |

|

|

0.4 |

% |

| Warrants |

|

|

1.0 |

% |

| Medium Term Notes |

|

|

|

|

| Banks |

|

|

1.5 |

% |

| Short-Term Investments |

|

|

8.5 |

% |

| Liabilities in Excess of Other Assets |

|

|

(17.5 |

)% |

| Net Assets |

|

|

100.0 |

% |

| Written Options Contracts |

|

|

(0.2 |

)% |

| Exchange-Traded Funds Sold Short |

|

|

(2.3 |

)% |

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Statement of Assets and Liabilities |

| As of March 31, 2024 |

| Assets: |

|

|

|

| Investments, at value (cost $113,980,326) |

|

$ |

117,268,835 |

|

| Purchased options contracts, at value (cost $546,594) |

|

|

355,764 |

|

| Cash |

|

|

888 |

|

| Receivables: |

|

|

|

|

| Interest |

|

|

108,585 |

|

| Dividends |

|

|

466,570 |

|

| Investments sold |

|

|

1,544,121 |

|

| Prepaid expenses |

|

|

29,423 |

|

| Other assets |

|

|

628 |

|

| Total assets |

|

|

119,774,814 |

|

| |

|

|

|

|

| Liabilities: |

|

|

|

|

| Credit facility, net (see note 7) |

|

|

14,975,863 |

|

| Due to broker |

|

|

1,793,624 |

|

| Securities sold short, at value (proceeds $802,222) |

|

|

2,293,449 |

|

| Written options contracts, at value (premium received $191,135) |

|

|

244,869 |

|

| Payables: |

|

|

|

|

| Professional fees |

|

|

131,875 |

|

| Management fee (see note 3) |

|

|

93,609 |

|

| Income tax payable |

|

|

89,391 |

|

| Accounting and administrative fees |

|

|

33,319 |

|

| Investments purchased |

|

|

31,903 |

|

| Transfer agent fees and expenses |

|

|

6,711 |

|

| Custody fees |

|

|

4,846 |

|

| Accrued other expenses |

|

|

8,064 |

|

| Total liabilities |

|

|

19,707,523 |

|

| Commitments and contingencies (see note 2) |

|

|

|

|

| |

|

|

|

|

| Net assets |

|

$ |

100,067,291 |

|

| Net assets consist of: |

|

|

|

|

| Paid-in capital |

|

$ |

98,100,278 |

|

| Total distributable earnings |

|

|

1,967,013 |

|

| Net assets |

|

$ |

100,067,291 |

|

| |

|

|

|

|

| Common shares outstanding |

|

|

8,963,239 |

|

| |

|

|

|

|

| Net asset value per common share |

|

$ |

11.16 |

|

| |

|

|

|

|

| Market price per common share |

|

$ |

7.82 |

|

| |

|

|

|

|

| Market price (discount) to net asset value per common share |

|

|

(29.93 |

)% |

See accompanying Notes to Financial Statements.

| Destra Multi-Alternative Fund |

| Statement of Operations |

| For the year ended March 31, 2024 |

| Investment income: |

|

|

|

|

| Dividend income |

|

$ |

1,721,315 |

|

| Distributions from alternative investment funds |

|

|

1,341,369 |

|

| Interest income |

|

|

868,324 |

|

| Total investment income |

|

|

3,931,008 |

|

| |

|

|

|

|

| Expenses: |

|

|

|

|

| Interest expense |

|

|

2,408,963 |

|

| Management fee (see note 3) |

|

|

1,528,607 |

|

| Professional fees |

|

|

318,871 |

|

| Accounting and administrative fees |

|

|

201,065 |

|

| Service provider fees |

|

|

113,391 |

|

| Income tax expense |

|

|

89,391 |

|

| Chief financial officer fees (see note 10) |

|

|

46,743 |

|

| Trustee fees (see note 10) |

|

|

37,708 |

|

| Transfer agent fees and expenses |